Though China would have you believe

Their goals, they are set to achieve

Their banks are in trouble

From their housing bubble

So capital, now, they’ll receive

Meanwhile, with Ukraine there’s a deal

For mineral wealth that’s a steal

This will help the peace

If war there does cease

And so, it has broader appeal

But really, the thing to denote

Is everything is anecdote

The data don’t matter

Unless it can flatter

The narrative as it’s been wrote

Confusion continues to be the watchword in financial markets as it is very difficult to keep up with the constant changes in the narrative and announcements on any number of subjects. And traders are at a loss to make sense of the situation. This is evidenced by the breakdown in previously strong correlations between different markets and ostensibly critical data for those markets.

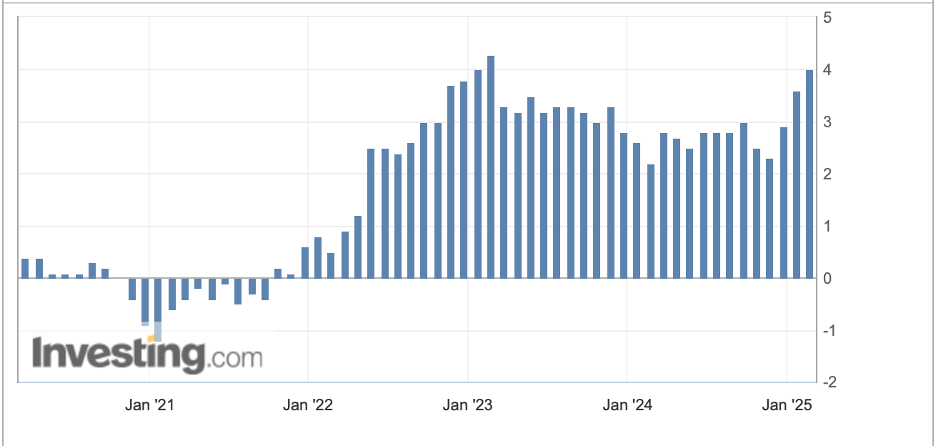

For example, inflation expectations continue to rise, at least as per the University of Michigan surveys, with last week’s result coming in at 4.3% for one year and 3.5% for 5 years. And yet, Treasury yields continue to fall in the back end of the curve, with 10-year Treasury yields lower by nearly 15bps since that report was released on Friday. So, which is it? Is the data a better reflection of things? Or is market pricing foretelling the future?

Source: tradingeconomics.com

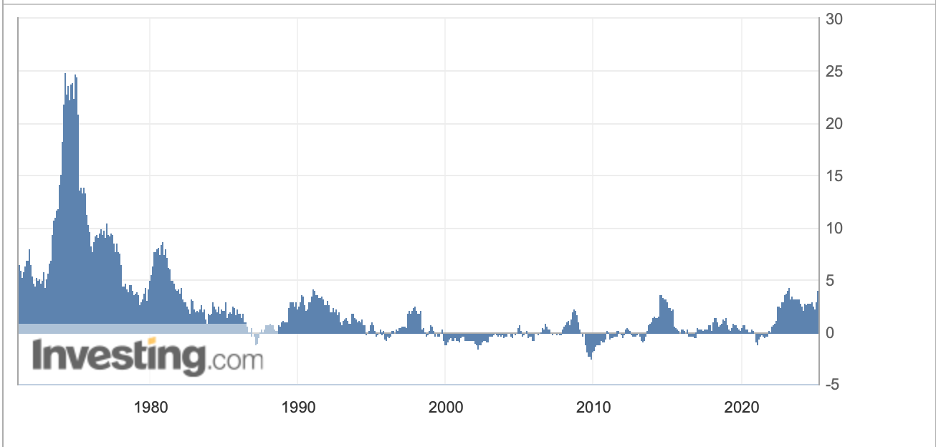

At the same time, the Fed funds futures market is now pricing in 55bps of cuts this year, up from just 29bps a few weeks ago. Is this reflective of concerns over economic growth? And how does this jibe with the rising inflation expectations?

Source: cmegroup.com

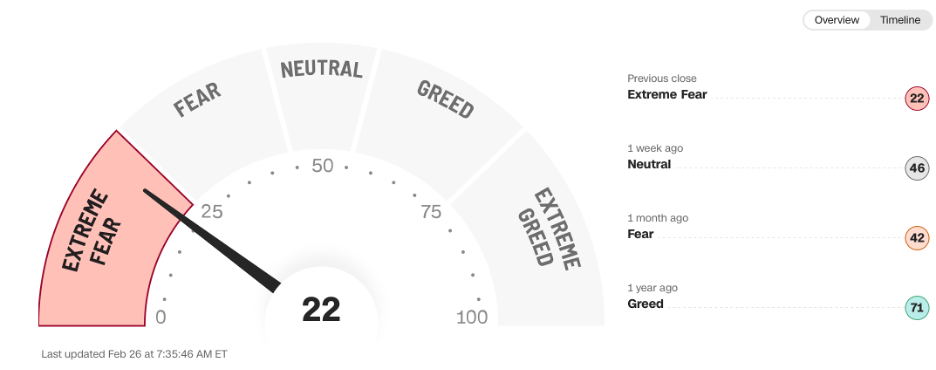

If risk is a concern, why is the price of gold declining?

Source: cnn.com

My point is right now, at least, many of the relationships that markets and investors have relied upon in the past seem to be broken. They could revert to form, or perhaps this is a new paradigm. In fact, that is the point, there is no clear pathway.

Sometimes a better way to view these things is to look at policy actions at the country level as they reflect a government’s major concerns. I couldn’t help but notice in Bloomberg this morning the story that the Chinese government is going to be injecting at least $55 billion of equity into their large banks. Now, government capital injections are hardly a sign of a strong industry, regardless of the spin. This highlights the fact that Chinese banks remain in difficult straits from the ongoing property market woes and so, are clearly not lending to industry in the manner that the government would like to see. I’m not sure how injecting capital into large banks that lend to SOE’s is helping the consumer in China, which allegedly has been one of their goals, but regardless, actions speak louder than words. Clearly the Chinese remain concerned over the health of their economy and are doing more things to support it. As it happens, this helped equity markets there last night with the Hang Seng (+3.3%) ripping higher with mainland shares (+0.9%) following along as well. Will it last? Great question.

Another interesting story that seems at odds with what the narrative, or at least quite a few headlines, proclaimed, is that the US and Ukraine have reached a deal for the US to have access to Ukrainian rare earth minerals once the fighting stops. The terms of this deal are unclear, but despite President Zelensky’s constant protests that he will not partake in peace talks, it appears that this is one of the steps necessary for the US to let him into the conversation. Now, is peace a benefit for the markets? Arguably, it is beneficial for lowering inflation as the one thing we know about war is it is inflationary. If peace is coming soon, how much will that help the Eurozone economy, which remains in the doldrums, and the euro? Will it lower energy prices as sanctions on Russian oil and gas disappear? Or will keeping the peace become a huge expense for Europe and not allow them to focus on their domestic issues?

Again, my point is that there are far more things happening that add little clarity to market narratives, and in some cases, result in price action that is not consistent with previous relationships. With this I return to my preaching that the only thing we can truly anticipate is increased volatility across markets.

With that in mind, let’s consider what happened overnight. First, US markets had another weak session, with the NASDAQ particularly under pressure. (I half expect the Fed to put forth an emergency rate cut to support the stock market.) As to Asian markets, that Chinese news was well received almost everywhere except Japan (Nikkei -0.25%) as most other markets gained on the idea that Chinese stimulus would help their economies. As such, we saw gains virtually across the board in Asia. Similarly, European bourses are all feeling terrific this morning with the UK (+0.6%) the laggard and virtually every continental exchange higher by more than 1%. Apparently, the Ukraine/US mineral rights deal has traders and investors bidding up shares for the peace dividend. Too, US futures are higher at this hour, about 0.5% or so across the board.

As to bond yields, after a sharp decline in Treasury yields over the past two sessions, this morning, the 10-year is higher by 1bp, consolidating that move. Meanwhile, European sovereign yields are all slipping between -2bps and -4bps as the peace dividend gets priced in there as well. While European governments may be miffed they have not been part of the peace talks, clearly investors are happy. Also, JGB yields, which didn’t move overnight, need to be noted as having fallen nearly 10bps in the past week as the narrative of ever tighter BOJ policy starts to slip a bit. While the yen has held its own, and USDJPY remains just below 150, it appears that for now, the market is taking a respite.

In the commodity markets, oil (-0.25% today, -2.0% yesterday) has convincingly broken below the $70/bbl level as this market clearly expects more Russian oil to freely be available. OPEC+ had discussed reducing their cuts in H2 this year, but if the price of oil continues to slide, I expect that will be changed as well. Certainly, declining oil prices will be a driver for lower inflation, arguably one of the reasons that Treasury yields are falling. So, some things still make some sense. As to the metals markets, gold (-0.2%) still has a hangover from yesterday’s sharp sell-off, although there have been myriad reasons put forth for that movement. Less global risk with Ukraine peace or falling inflation on the back of oil prices or suddenly less concern over the status of the gold in Ft Knox, pick your poison. Silver is little changed this morning but copper, which had been following gold closely, has jumped 2.7% this morning after President Trump turned his attention to the red metal for tariff treatment.

Finally, the dollar is firmer this morning, recouping most of yesterday’s losses. G10 currencies are lower by between -0.1% (GBP) and -0.5% (AUD) with the entire bloc under pressure. In the EMG space, only CLP (+0.45%) is managing any strength based on its tight correlation to the copper price. But otherwise, most of these currencies have slipped in the -0.1% to -0.3% range.

On the data front, New Home Sales (exp 680K) is the only hard data although we do see the EIA oil inventory numbers with a small build expected. Richmond Fed president Barkin speaks again, but as we have seen lately, the Fed’s comments have ceased to be market moving. President Trump’s policy announcements are clearly the primary market mover these days.

Quite frankly, it is very difficult to observe the ongoing situation and have a strong market view in either direction. There are too many variables or perhaps, as Donald Rumsfeld once explained, too many unknown unknowns. Who can say what Trump’s next target will be and how that will impact any particular market. In fact, this points back to my strong support for consistent hedging programs to help reduce volatility in one’s financial reporting.

Good luck

Adf