While yesterday’s moves were extreme

It seems like t’was all a bad dream

This morning there’s calm

And nary a qualm

Though things may not be what they seem

For now, oil’s price has retreated

And stocks, a round trip, have completed

As Trump has implied

Though not verified

Iran soon will have been defeated

One must be impressed with the price action yesterday, if nothing else. It is a very rare occasion when the price of anything in a public market behaves like we saw oil behave yesterday. From Friday’s closing price in the futures market of $90.71/bbl, we saw a $28.70 (31.6%) rally and a subsequent $34.35 (37.9%) decline in the first 24 hours of trading.

Source: tradingeconomics.com

With oil back to Friday morning’s, still elevated, prices, it’s almost as if nothing happened yesterday. The two stories that appear to have driven the remarkable reversal early Monday morning were first, the discussion about the G7 potentially coordinating a release of strategic reserves, with that meeting slated for this morning. The other catalyst apparently was a comment from President Trump that, having made significant progress on their objectives, the war could be over “very soon”. Obviously, that would be a great outcome for all involved, although it remains to be seen if that will be the case.

The upshot is that while oil saw the most dramatic price movement across markets, prices everywhere synchronized such that those that had declined (stocks, bonds and metals) rebounded, while the dollar, which rose, retreated. And that’s where we are this morning.

As I read across news sources, there remains no agreement on any aspect of the ongoing war with each side of the argument maintaining their views. There is a contingent that insists Iran is about to start a major retaliatory campaign that will devastate Israel and Gulf neighbors and a side that insists Iran’s military infrastructure has been so compromised they have nothing left but drones to fire. As I’m not on the ground (thankfully) nor in any situation room on any side, I am completely in the dark like essentially all of us. In fact, arguably, market price action is one of the best indicators we have, because institutions don’t invest on hope, but on the best information they have. This tells me that the worst-case scenario has been priced out for now, meaning a prolonged conflict, but frankly, neither I nor anyone else really knows.

So, let us embrace our ignorance on the issue and simply observe market behavior to see what we can glean. Starting with equity markets, the below chart shows the S&P 500 futures from Sunday night’s opening through this morning. While the opening is obvious on the left, the huge green bar on the right at 3:15pm is the other major feature.

Source: tradingeconomics.com

The interesting thing to me is that Trump’s comment about the war ending soon were not made until 5:45pm. This tells me that there was a major buy order that went through the market shortly before the close, a feature that we have seen more frequently of late. My point is there is still much more to the markets than just the Iran conflict. In fact, the cynical view is that the algorithms continue to control things completely and that there is a major effort to prevent a significant decline in equity markets overall, at least US equity markets. That’s a little conspiratorial, but one cannot ignore the evidence.

At any rate, after positive closes in the US yesterday on the order of +1.0%, we saw gains across the board in both Asia (Japan +2.9%, HK +2.2%, China +1.3%, Korea +5.4%, Taiwan +2.1%, India +0.8%, Australia +1.1%) as only New Zealand lagged, essentially unchanged on the day, amid concerns of rising inflation and a tighter RBNZ going forward. Europe, too, is enjoying the session with strong gains across the board reversing yesterday’s declines as Spain (+2.9%) leads the way, but there is strength everywhere (Germany +2.4%, France +1.9%, UK +1.6%). At this hour (7:10), US futures are also pointing higher, but just by 0.2% or so across the board.

Bonds also reversed yesterday, albeit not quite as dramatically. So, in a picture remarkably similar to both oil and stocks, the yield on the 10-year gapped higher Sunday night and fell sharply enough to close lower yesterday as per the below chart.

Source: tradingeconomics.com

Much of that retracement came after Europe closed, though, and so while this morning, 10-year Treasury yields have edged back up by 2bps, European sovereign yields are lower across the board with Italian BTPs (-6bps) leading the continent although UK Gilts (-7bps) have rallied further. Other nations have seen a mix between -4bps and -5bps although Germany (unchanged) seems to be suffering on a relative basis after its Trade Surplus grew to €21.2B on the back of a substantial decline in imports. Throughout all this, JGB yields (-1bp) have been the least impacted and show no signs of running away at this point despite much doomsaying for the nation.

Metals markets have reversed their decline from yesterday and are higher across the board (Au +0.9%, Ag +1.6%, Cu +1.0%, Pt +1.9%). This is all part of the same story with price action virtually identical, although again, not quite as dramatic, as that of oil.

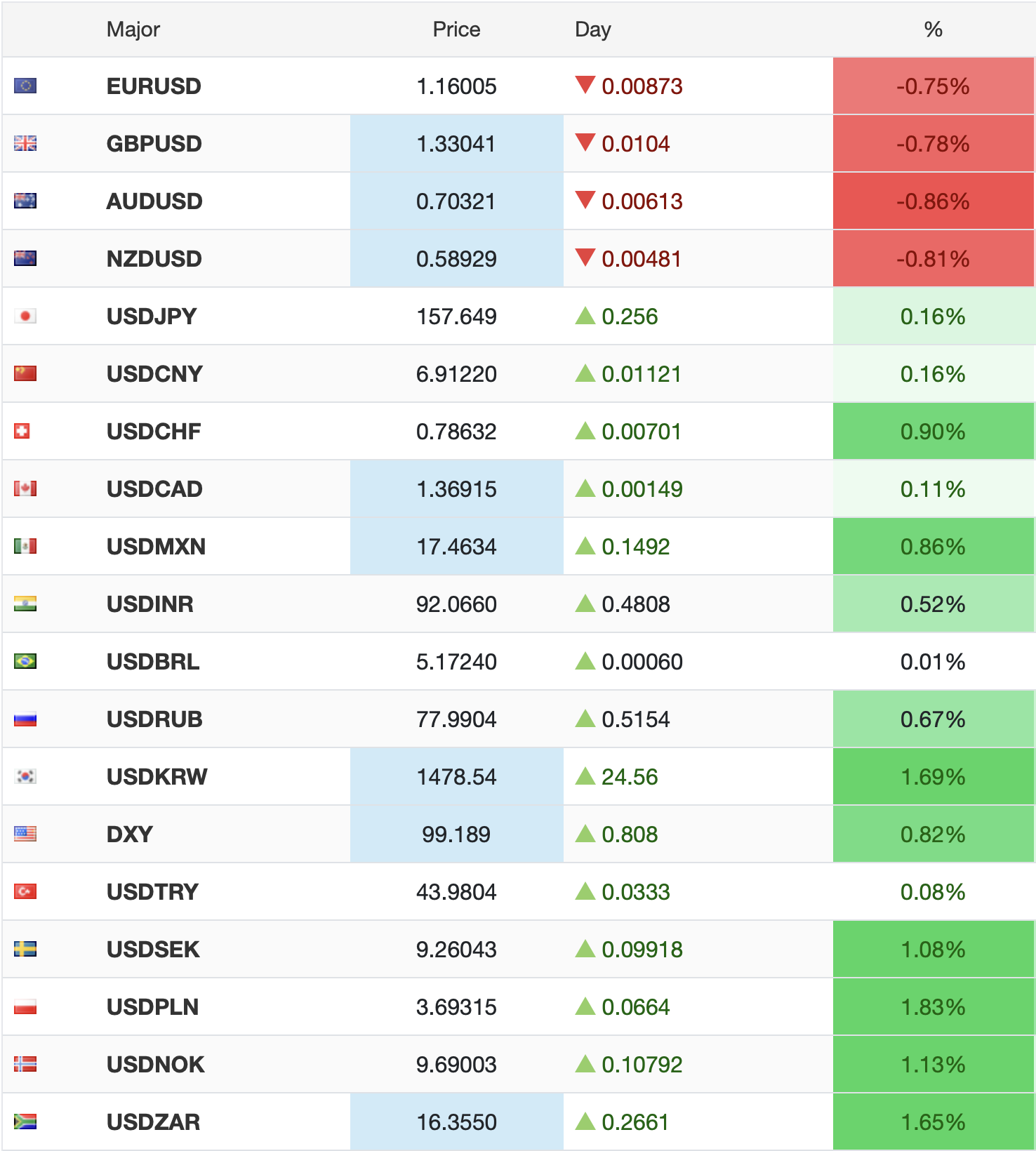

Finally, the dollar, which had significant support yesterday is giving back some of those gains as well. But let’s face it, if we take a look at the dollar over the past year vs. the euro, it has largely traded withing a 1.1500 / 1.1900 range and doesn’t appear to be making a break in either direction.

Source: tradingeconomics.com

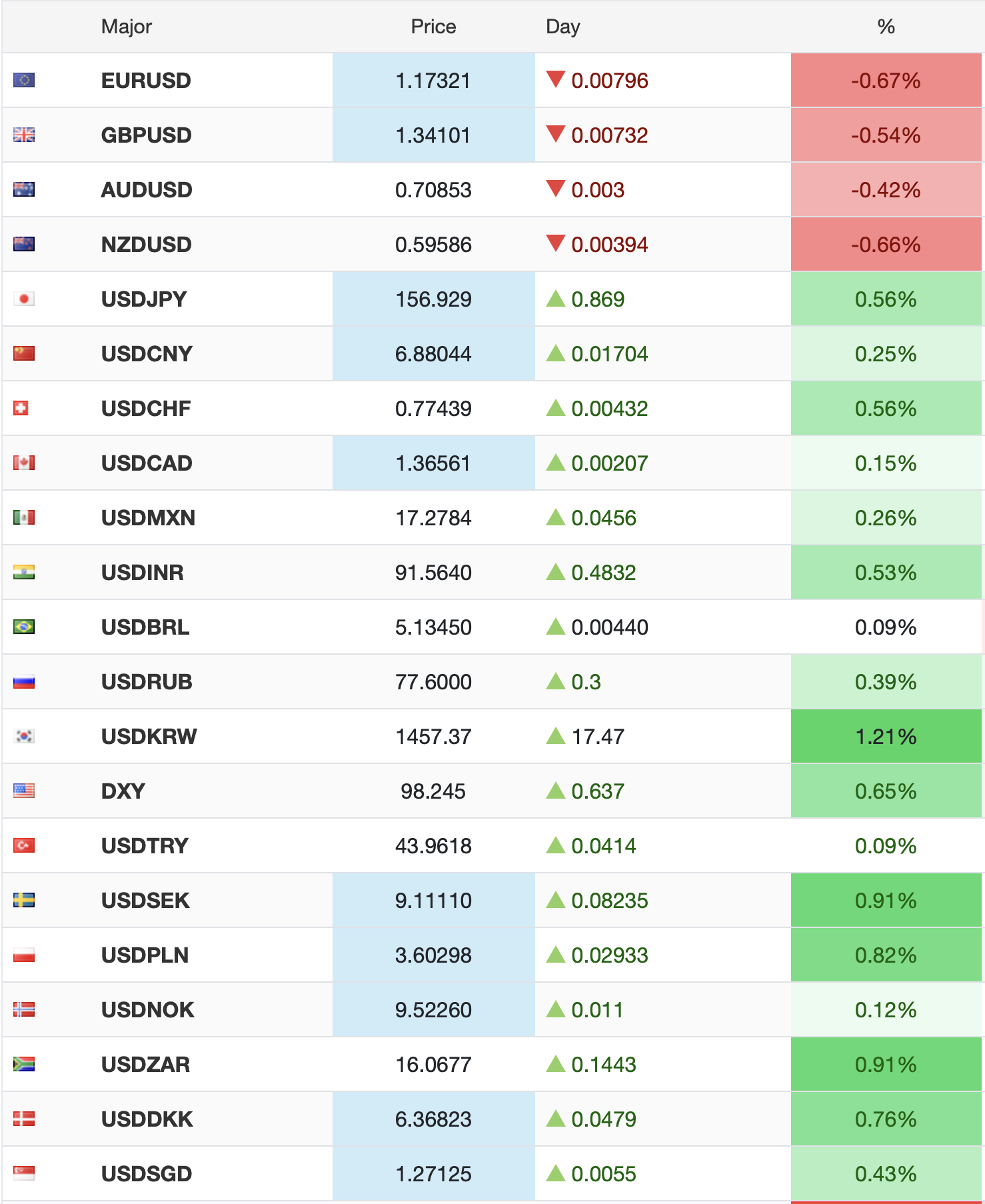

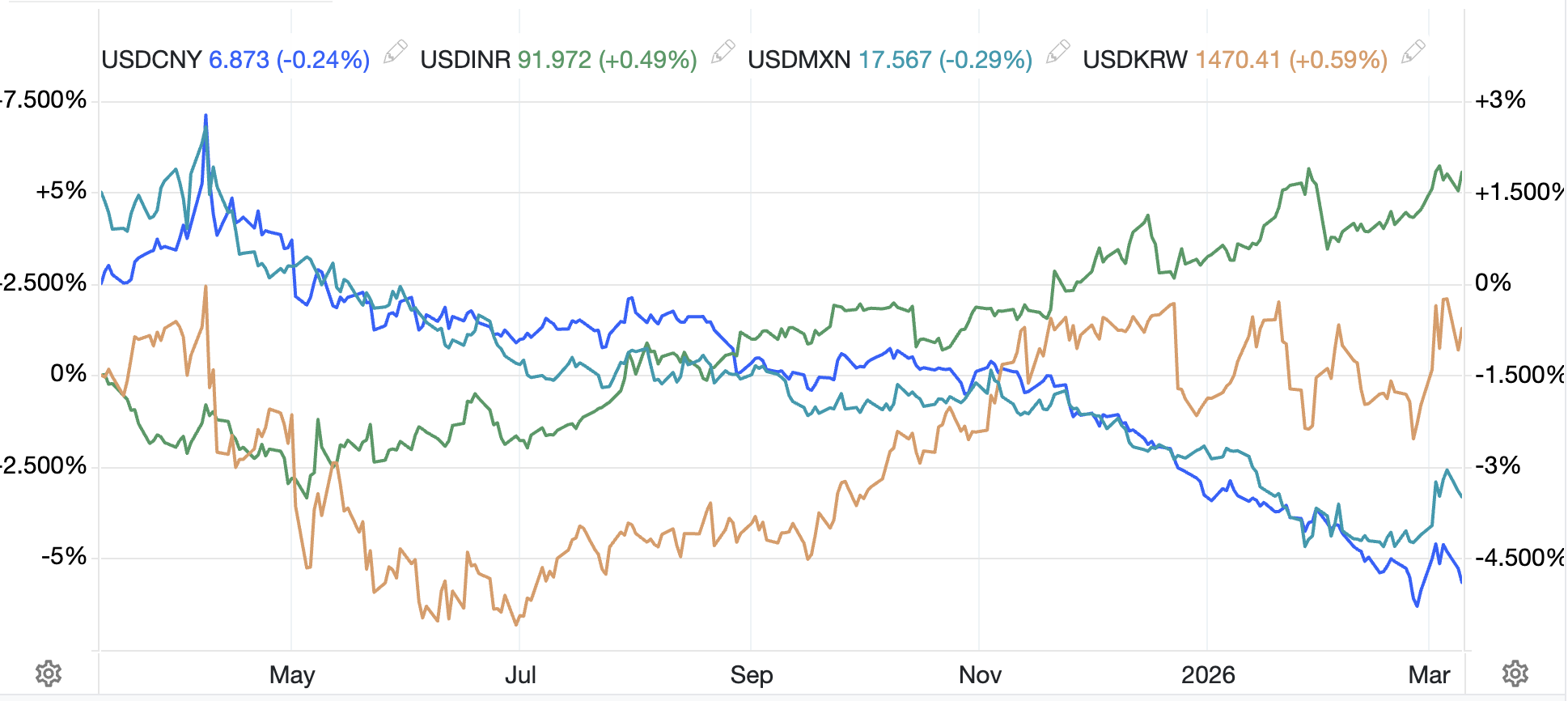

The very messy chart below shows four key EMG currencies to demonstrate that there is no trend there either. While CNY and MXN have both strengthened during the year, INR and KRW have both fallen. All I’m saying is that the idea that the dollar is either collapsing or exploding higher is simply not true. Different currencies have different drivers, and while sometimes there is a key dollar issue that impacts virtually everything, many times, you need to watch the currency in question.

Source: tradingeconomics.com

Turning to the data, this morning we just saw NFIB Business Optimism print a bit soft at 98.8, exp 99.7, and we are awaiting Existing Home Sales (exp 3.89M). Tomorrow’s CPI will garner more attention, I think. Too, the Fed is in their quiet period as they meet next Wednesday, so even though they have been drowned out by events lately, the FOMC meeting will still get a lot of attention.

But that is where we stand. As has been the case since President Trump’s election, White House bingo remains the biggest risk to markets since one never knows what may come out. The backdrop of the war continues to be front of mind for all market participants, so new stories will have market impacts. With that in mind, short term forecasts are even more of a waste of time than they usually are. The questions I am pondering are about the long-term implications when the military activity ends. Certainly, any result where Iran gives up its terrorist interests would not only be welcome on the global stage but would open the door for much more oil flow around the world and lower prices across the board. Of course, a more entrenched Iranian regime would likely see even stricter sanctions there with the need for other sources to help satisfy global demand. I guess we shall see.

Good luck

Adf