While news from Iran shows the war

Continues apace, like before

On Wall Street it seems

It’s over, with dreams

Of stock market rallies galore

Now, I realize stocks look ahead

And discount the future instead

But wars tend to last

They don’t end so fast

Beware in which markets you tread

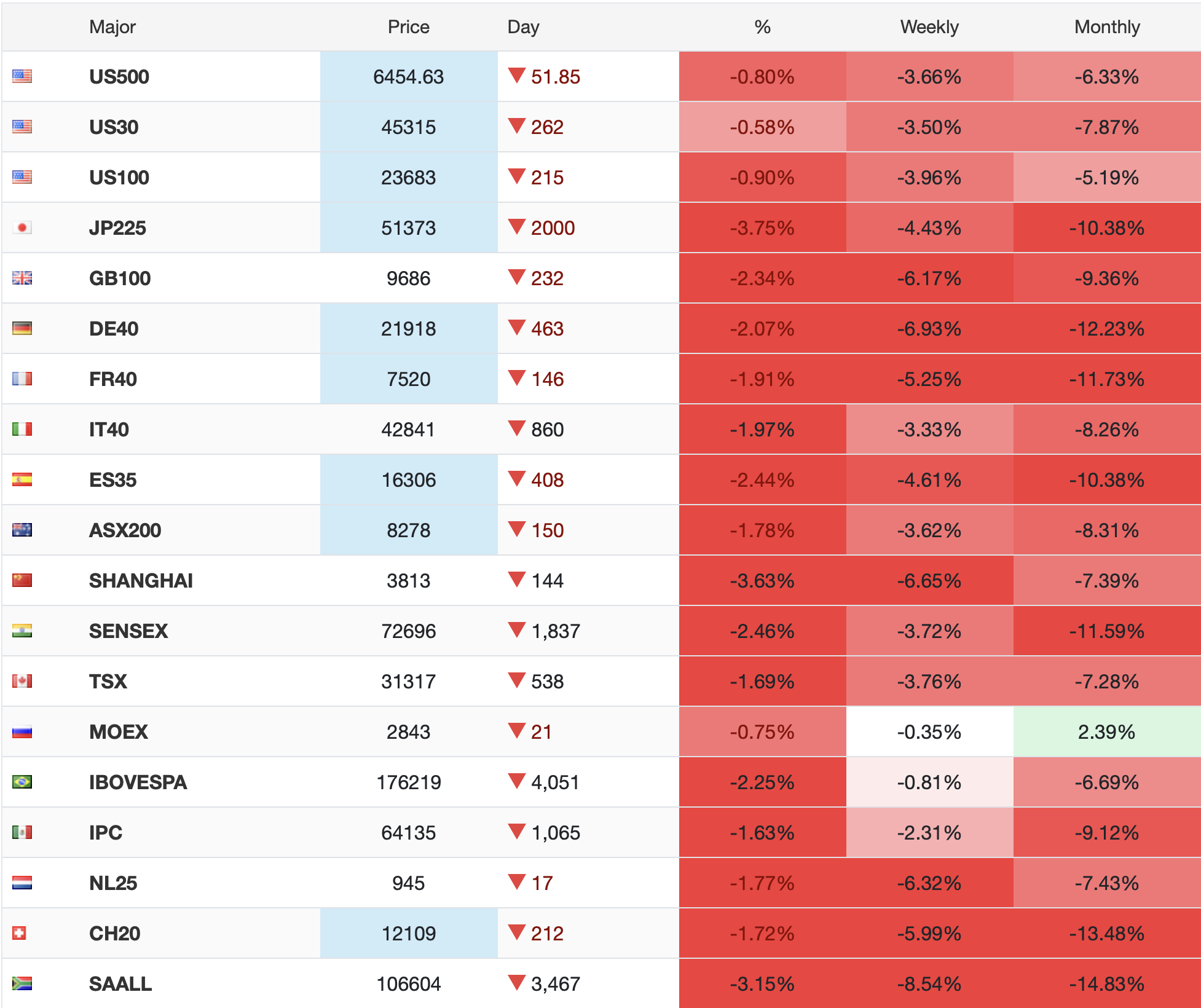

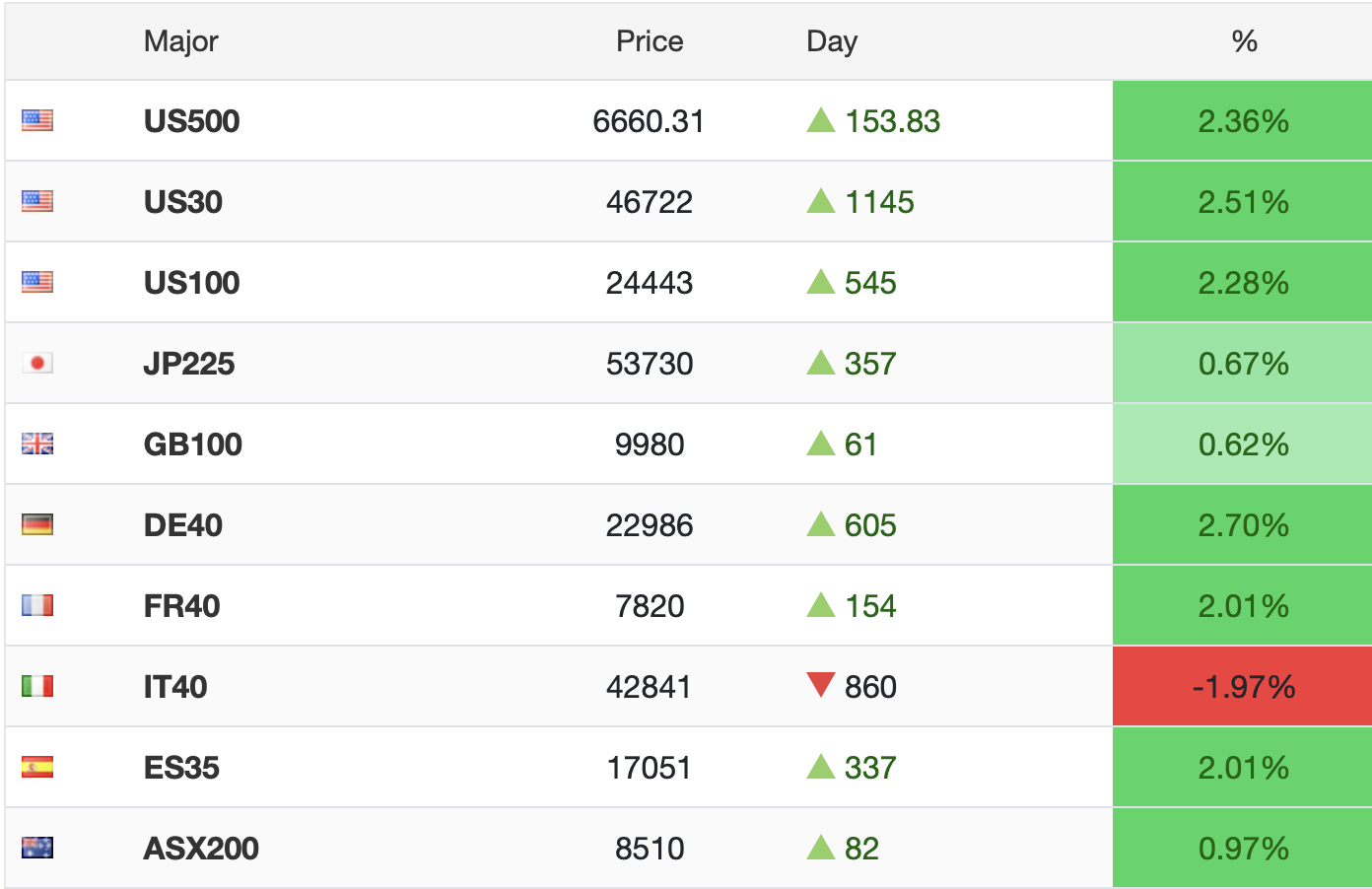

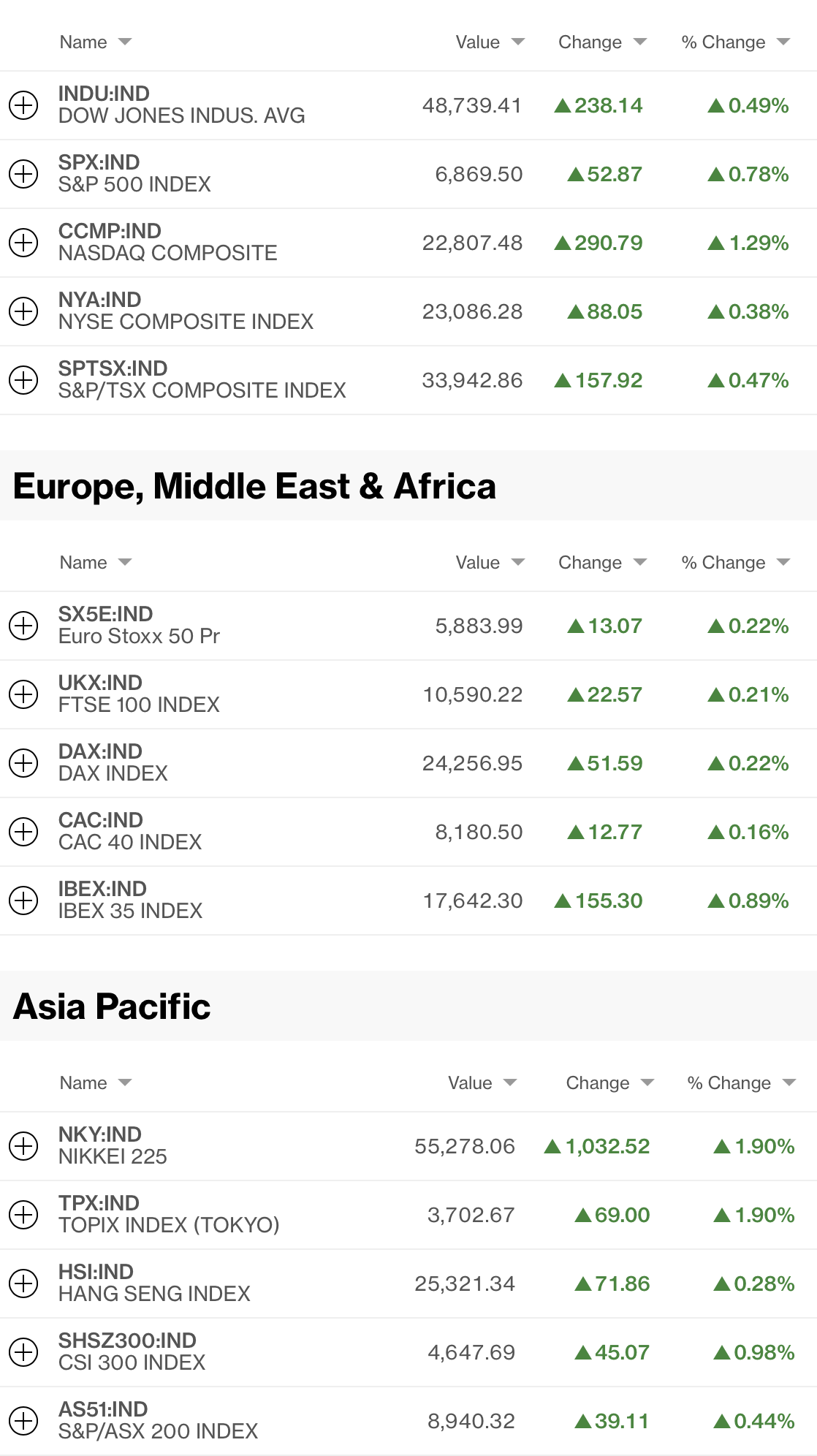

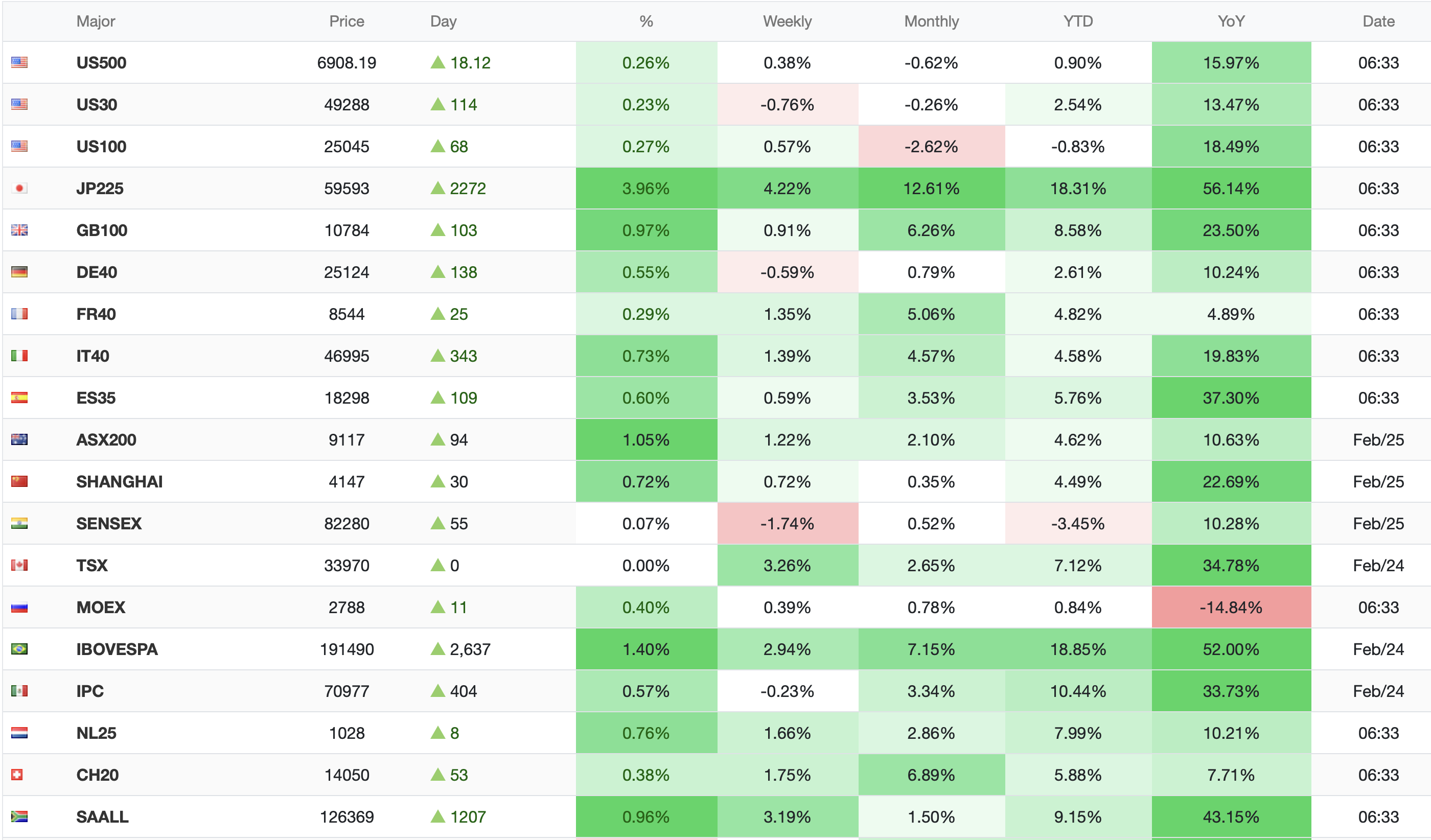

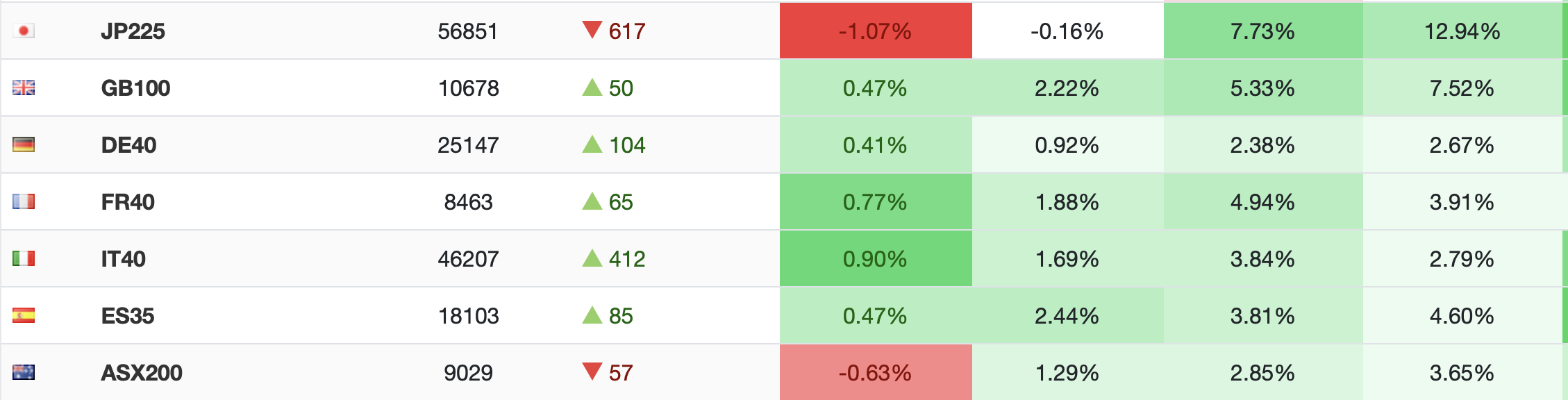

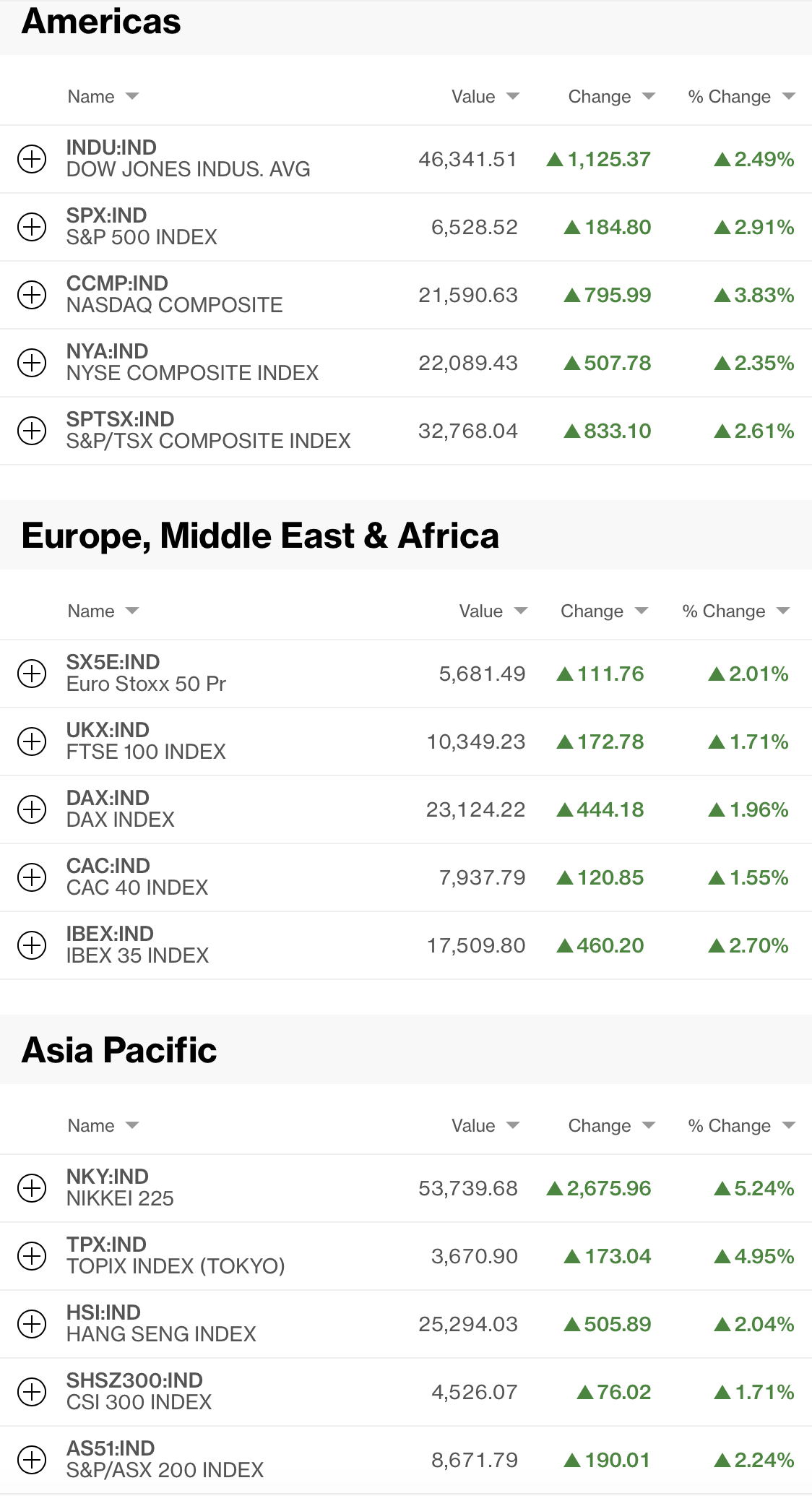

As March and Q1 ended, it appears that there have been some changes in opinions in the investment community. At least that is what I glean from the following Bloomberg screenshot of major global equity markets including yesterday’s US session and the overnight activity.

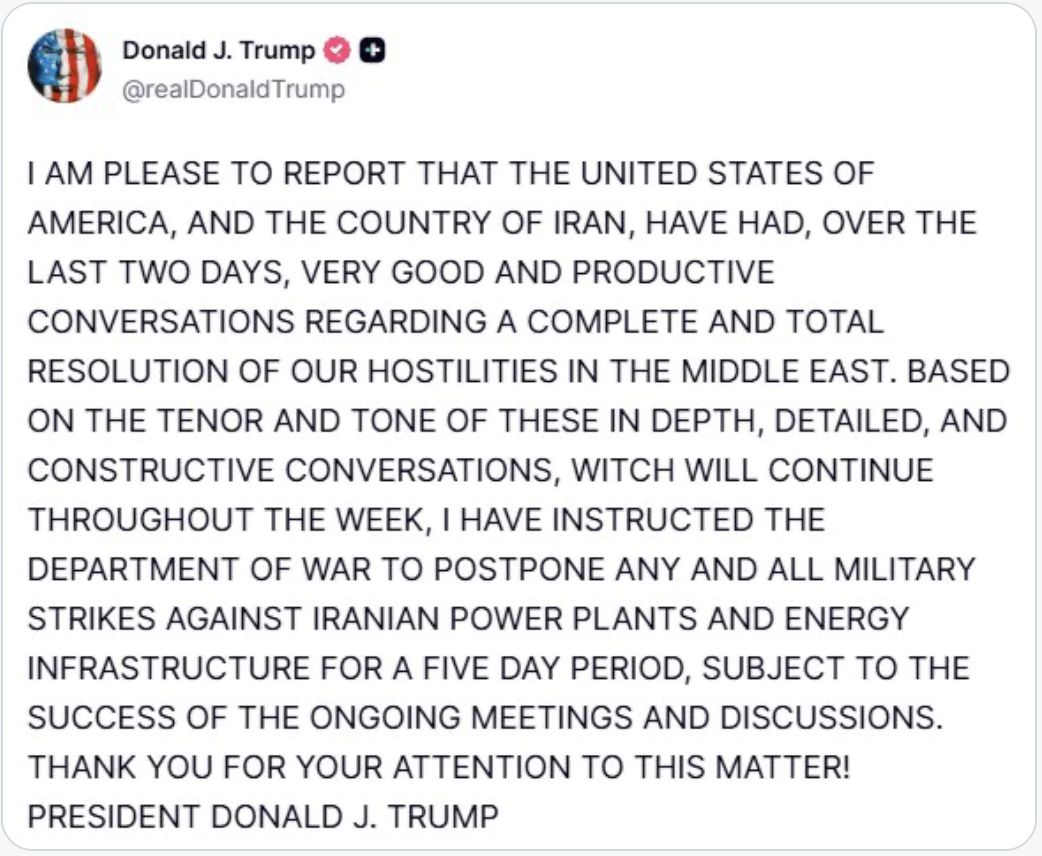

As far as I can tell, missiles are still flying in the Middle East, the US and Israel continue to attack specific targets with B-52’s dropping significant amounts of precision guided bombs, the Strait of Hormuz continues to have extremely restricted movement and the UAE, according to the WSJ, is now ready to join the war directly. None of that seems like de-escalation of fighting, but then I am not a military strategist, so perhaps I don’t understand the concept of de-escalation well.

One take I saw this morning was that equity markets are pricing in the increased likelihood that the US will be leaving the conflict. On the surface, I liked that idea, and that would certainly explain some of the US rally yesterday, but that doesn’t explain why Asia soared and Europe has rallied as well, given they would have to deal with the rest of the process. This evening at 9:00 President Trump will be addressing the nation, so I presume we will have a better understanding of things after that.

One other thing to remember is that the president uses his Truth Social posts to add to the fog of war and create strategic uncertainty for all parties involved. I read this morning that the administration has been speaking (not directly) with some Iranians and creating a plan for the future, but it is not clear if those people have sufficient power to unite the country there yet. All in all, while anything is possible, it strikes this poet that things in Iran have not ended, nor will they until the Strait of Hormuz is back to full operational capacity regardless of the President expressing the view that the US (and Israel) have done the hard part and Europe and Asia can deal with the Strait themselves.

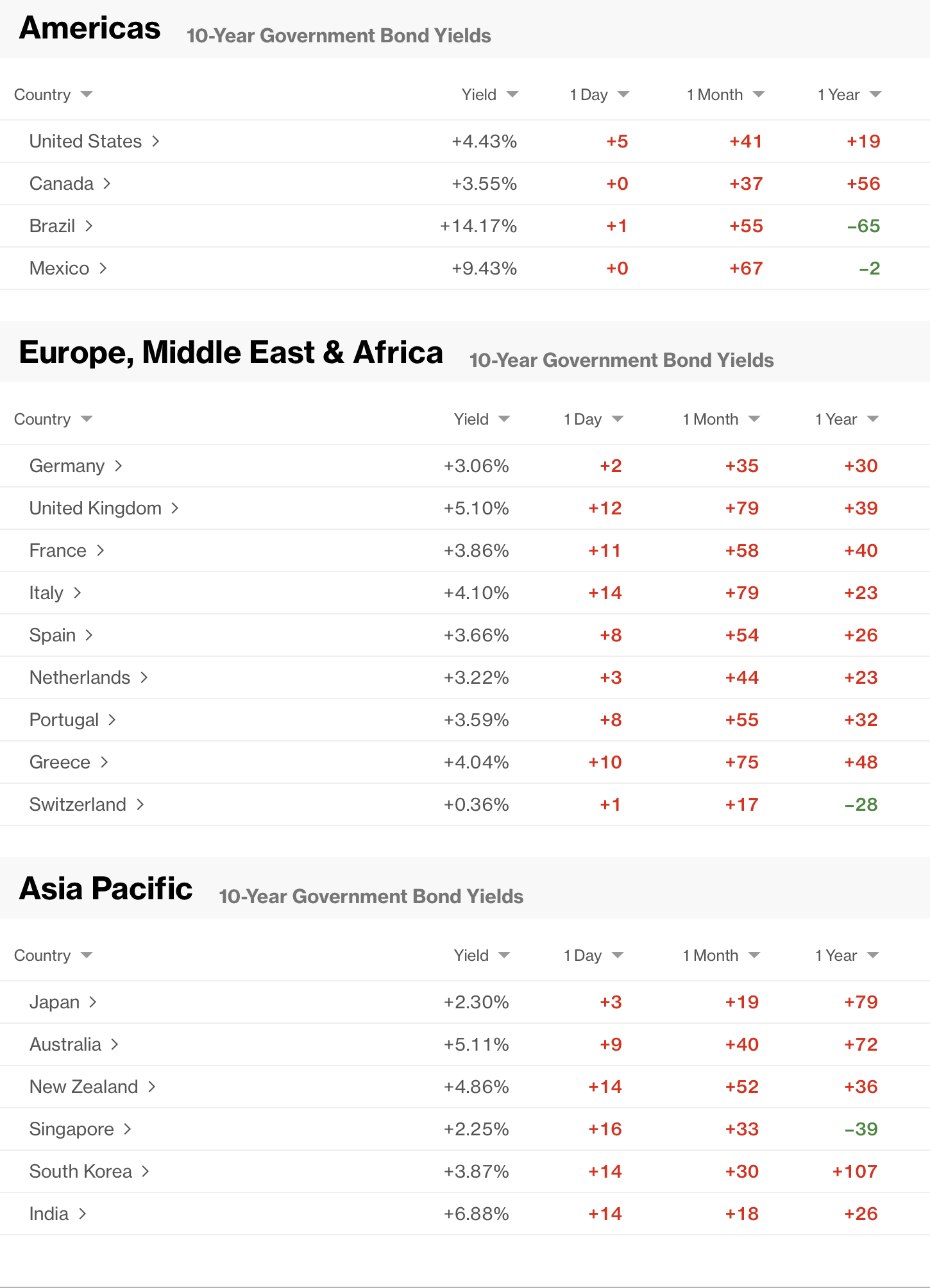

But that is where we stand this morning, with risk back in vogue across the board as oil (-1.5% and back below $100/bbl) slipping while gold (+1.5%) continues its rebound. Bonds (-3bps this morning and down by 20bps from their peak on Friday) continue to rally and have taken European sovereigns along for the ride with most of Europe seeing yields slide between -7bps and -9bps although German bunds, which have held up the best, are only lower by -4bps. Happy Days are here again!

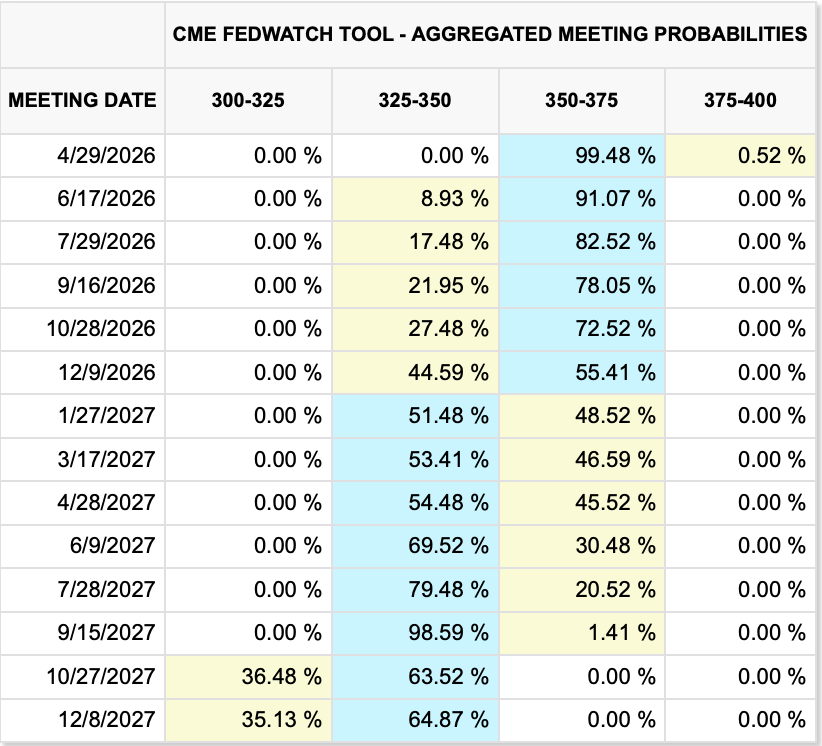

With all that good news, let’s consider what else is going on, away from Iran, that may impact markets. At this point, we know the Fed is on hold this month, and likely through the autumn, at least, given the short-term inflation impacts of the oil situation.

Source: cmegroup.com

As an aside, there have been a number of analysts who are calling for a significant rise in food inflation but be careful on that front. As @inflation_guy, Mike Ashton points out, [emphasis added]

“…secondary knock-on effects that will be felt eventually in CPI. One that has gotten a lot of press recently is that less oil means less fertilizer and less fertilizer means less crop production and less crop production means higher prices for food. I actually think that’s probably overblown in terms of what the consumer will see, because most of the cost of consumer food items is in the packaging and delivery and not the raw goods, and so as raw food commodity prices go up it will likely be partially offset by transportation prices declining.”

In fact, I expect that most central banks are terrified of the current situation as they understand, intellectually, that the oil price shock will be temporary, but will feel significant pressure when inflation starts to rise to “do something about it”. Australia already hiked rates, but that was assumed prior to the onset of the war. The calculation they are all trying to make is will the negative impacts on growth outweigh the rising pressure on inflation and what will the timeline be like. In the end, my take is very few will hike in response to this event, especially if the military activity ends before the end of April. And that is why they get paid the big bucks, to get those decisions right. Alas, their collective track record is not great.

And beyond that, I don’t see much news directly driving the narrative. It is still the war, and all the individual takes there, and a much lesser role to the Fed and other central banks. Economic data is decidedly not part of the current discussion in any meaningful way and given the impact the war is going to have on data for a while going forward, it will be very difficult to suss out underlying trends from headline numbers.

I’ve already discussed most market segments, leaving just currencies untouched at this point. Given the reversal in views, we cannot be surprised that the dollar, which has been a major beneficiary of the war, has reversed its recent price action as well. In fact, using the euro as our proxy, we can see in the below chart that the reversal started at 7:00am yesterday morning and the single currency has rebounded by 1.25% since then.

Source: tradingeconomics.com

And while the euro (+0.5% today) has rallied this morning, it mostly lags other currencies with the pound (+0.7%), AUD (+0.8%), CHF (+1.0%) and SEK (+1.0%) all having very strong sessions. As well, the yen (+0.2%) has backed away from the 160 level and even CAD (+0.2%) and NOK (+0.5%) are stronger despite the decline in oil prices. It should be no surprise that the EMG bloc is also showing strength with CLP (+1.1%) leading the way followed by HUF (+1.0%) and ZAR (+0.9%). One disappointment is KRW (+0.2%) which has been one of the worst performers for the past month (-4.0%) and is barely rebounding. Chile is intricately bound to the price of copper, which has rallied slightly (+1.0%) in the past week, but continues to lag the precious metals. However, there is a story about the major copper company there, Codelco, which is supporting the currency this morning. Net, the dollar is giving back some of its recent gains today and will likely continue to do so if risk appetite remains robust.

While data hasn’t had much impact, this morning we see ADP Employment (exp 40K) as well as Retail Sales (+0.5%, +0.3% ex autos) and then ISM Manufacturing (52.5) and Prices Paid (73.0). Yesterday’s data was in line with expectations and did nothing to alter any perceptions about the economy or path of interest rates.

And that’s all we have. US futures are rising this morning (+1.0% across the board at 8:00) and for now, risk is the way. I guess we will have to hear what the President says this evening to consider changing views.

Good luck

Adf