It wasn’t all that long ago

That folks really wanted to know

What Jay and the Fed

Implied was ahead

And if more cuts were apropos

But later today when they break

Their words are unlikely to shake

The narrative theme

That whate’er they deem

Important, is just a mistake

Presidents Trump and Putin spoke at length yesterday, but no solution was achieved so the Ukraine War will continue unabated for now. While talks are better than not, certainly this is a disappointment to some. As well, the astronauts who have been stranded in space for the past 8 months are safely back on earth. I mention these things because they are seemingly far more important than central banks these days, and today, that is all we have to discuss regarding financial markets.

To begin, last night the BOJ left rates on hold as universally anticipated. The initial market response was for the yen to weaken through 150 briefly, but then Ueda-san spoke and discussed the expected wage increases and how the economy was doing fine, and the new market assessment is that the BOJ will hike rates by 25bps in May at their next meeting. The market response was to buy back the yen, at least for a little while, although right now, USDJPY seems to be attracted to the 150 level overall.

Source: tradingeconomics.com

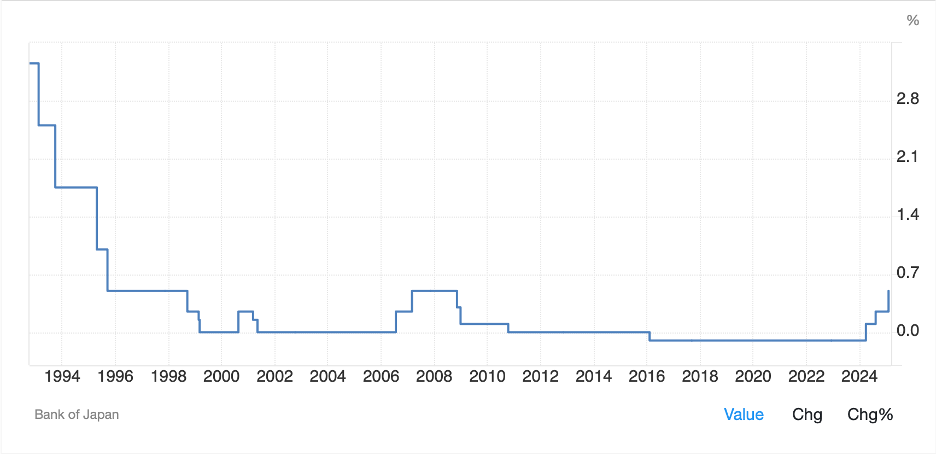

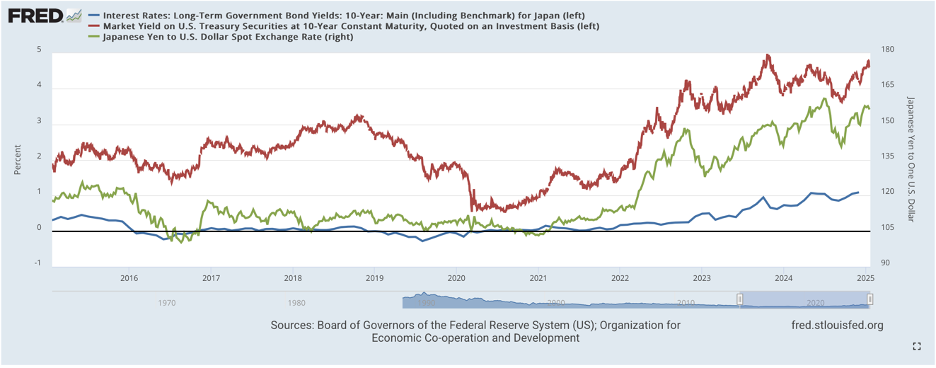

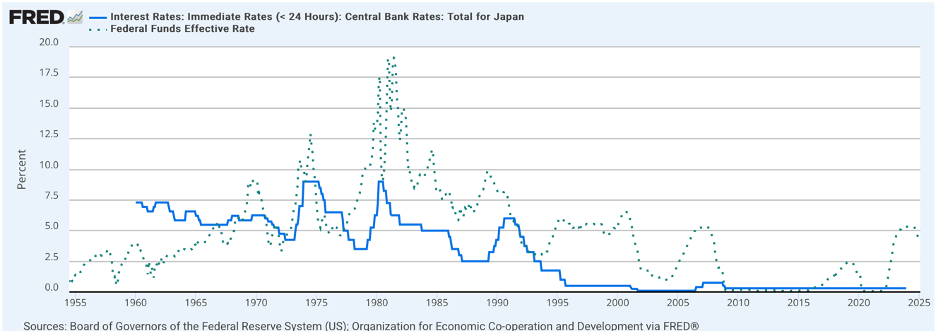

It is worth understanding, though, that the last time short-term interest rates were that high in Japan was back in July 2008. And they have not been above that level since August 1995. The below chart from FRED database speaks volumes about just how low interest rates have been in Japan over time, and as an adjunct, just how long the opportunity for shorting JPY on the carry trade has been around. That dotted line is the Fed funds rate compared to the Japanese overnight rate.

Along the central bank thesis, Bank Indonesia, too, met last night and left policy on hold with their policy rate at 5.75%. Governor Warjiyo explained that he felt falling inflation and improving growth would help prevent rupiah weakness despite the fact that the currency has been the worst performing Asian currency this year and is trading at historic lows.

But on to the FOMC meeting which will conclude at 2:00 this afternoon with the policy statement (no change expected although some tweaking of the verbiage is likely) and the release of the latest dot plot. You have probably forgotten that at the December meeting, the FOMC reduced the median expectation of rate cuts for 2025 from 4 prior to the election to just 2. In the interim we have seen Fed funds futures trade to where barely one rate cut was priced in, although we are now back to three cuts, seemingly on the idea that tariffs will cause significant economic weakness, and the Fed will need to respond. At least that’s what the punditry maintains.

Here is the last dot plot for information purposes and it will be interesting to see just how much things have changed. will longer run rates continue to move higher? Will 2 rate cuts still be the median outcome for 2025? All this we get to learn at 2:00.

Source: federalreserve.gov

But arguably, of far more import will be Chairman Powell’s press conference beginning at 2:30. Prior to the Fed’s quiet period, the broad assessment was that patience in future rate moves was appropriate and they were happy with the current situation. However, I am confident there will be numerous questions regarding the potential impact of tariffs on monetary policy responses, as well as other things like DOGE and an audit of the Fed. Will any of it matter? Maybe at the margin, but for most markets, I suspect that fiscal issues will remain dominant. The one exception is the FX market, where unalloyed hawkishness could change views on the dollar’s recent weakness (although it is firmer this morning) while a dovish tone will almost certainly undermine the greenback. So, with no other data of note to be released beforehand, it is clearly the day’s major event.

Ahead of that event, let’s see how markets have behaved overnight. Following a weak session in the US, where all three major indices were lower by about -1.0% on average, Asia had a mixed picture. The Nikkei (-0.25%) found no love from Ueda-san and drifted lower. Both Hong Kong (+0.1%) and China (+0.1%) edged higher but continue to doubt the benefits of the mooted Chinese stimulus program while the rest of the region was mixed with some gainers (Indonesia, Korea, India) and some laggards (Taiwan, Australia, Malaysia). In Europe, too, the picture is mixed with the DAX (-0.4%) lagging while the CAC (+0.5%) is gaining. In Germany, the historic breech of the debt brake is not having the positive impact anticipated, or perhaps this is just selling the news. Overall, though, shares in Europe seem to be awaiting the Fed’s actions, or comments, rather than focusing on anything else. As to US futures, at this hour (7:30), they are pointing slightly higher, about 0.25% across the board.

In the bond market, Treasury yields have edged up 1bp this morning but continue to hang around 4.30%. European sovereign debt has seen yields slip -1bp to -2bps, arguably on the Eurozone inflation data released 0.1% lower than forecast at 2.3%. This continues the idea that the ECB will be cutting rates again at their next meeting. As to JGBs, they are unchanged yet again, seemingly affixed at 1.50%.

Commodity prices show oil (-0.2%) continuing yesterday’s decline. From the time I wrote to the end of the session, WTI fell $2/bbl, perhaps on the idea that the Putin/Trump phone call was bringing the war closer to an end. Regardless, if economic activity is slowing, that will lessen demand everywhere, a clear price negative. As to gold (+0.25%) it continues to trade higher undaunted by any news on any front. While silver is little changed this morning, copper (+0.7%) has now crested $5.00/lb and is pushing to the all-time highs seen back in May 2024.

Finally, the dollar is rallying this morning, higher against all its G10 counterparts by between 0.2% and 0.4%. This looks to me like a trading correction, not a new trend. The same price action is true in the EMG bloc with one real outlier, TRY (-4.2%) which actually traded down by as much as -10% earlier in the session (see chart below) on the news that President Erdogan had his key political rival, Istanbul mayor Ekrem Imamoglu, arrested on charges of fraud and terror, while his university diploma was revoked, seemingly in an effort to prevent him from running for president in the future. Thank goodness we never have things like that happen in this country!

Source: tradingeconomics.com

There is no data released today other than EIA oil inventories where a modest net build across products is currently expected. So, until the Fed, I would anticipate very little net movement. After that, it all depends. However, Powell will need to by extremely hawkish to shake any of my view that the dollar is headed lower overall.

Good luck

Adf