The war in Iran rages on

But markets are starting to yawn

Initial concern

Led traders to spurn

Risk assets each dusk until dawn

But now, just a few days have passed

And fear mongers all seem downcast

Most stocks have rebounded

And that has confounded

The bears who, gross shorts, had amassed

In fact, today’s story of note

Is China’s decision to float

A lower growth rate

To be their new fate

As Xi seeks a different scapegoat

This morning is the sixth day of the military action in Iran and depending on the source, the US is either kicking ass or setting up for the greatest collapse of all time. Perhaps the most interesting statistic of this war is the number of casualties reported thus far, which when summed across all the theaters, appears to be somewhere between 1000 and 1200. It seems to me that given the ferocity of the attacks on both sides, that is a remarkably low number. I certainly hope it stays low, for everyone’s sake.

In the meantime, market participants have absorbed the ongoing information and much of the initial FUD has been ameliorated. I only say this because yesterday and overnight, equity markets are almost universally higher, and in some cases, by substantial amounts. Arguably, this is a bigger disaster for the Iranians than almost anything else. If financial markets continue to motor along despite the war, it removes a potential pressure point on President Trump to deescalate. In fact, the only market that is continuing to demonstrate any price concerns is the oil market, where WTI (+2.6%) and Brent (+2.2%) are both back close to the highest levels seen in the first days.

Source: tradingeconomics.com

The Strait of Hormuz continues to be effectively closed, and that remains a problem for both Europe and Asia, especially China. In fact, this morning I read that China has ceased exporting refined products amid concerns of how long this war will continue.

Now, permanently higher oil prices would definitely have severe negative consequences for the global economy if that were to be the outcome. But I don’t see that as the outcome. Rather, the world is awash in oil as the US and Canada and Venezuela and Brazil and Argentina continue to pump like crazy. As well, Saudi Arabia has two major pipelines that ship oil to the Red Sea rather than require transit of the Strait, so I am not hugely concerned about a much higher price. All of the fears of $100/bbl or higher oil in the event of a closure of the Strait of Hormuz have not come to pass, at least not yet, and I see no reason for that to be the case going forward.

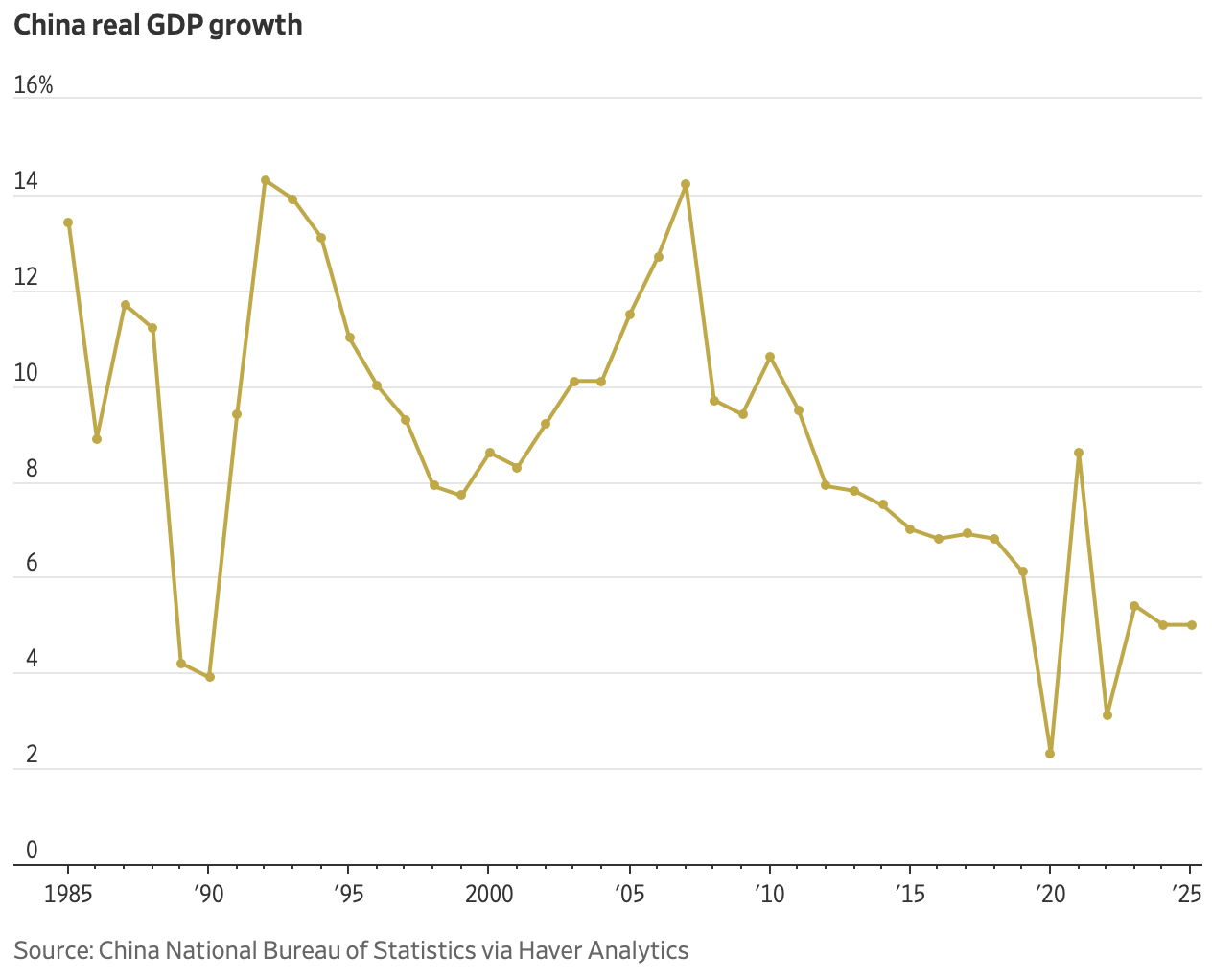

But away from oil, things are remarkably ordinary in markets, so much so that the real story of the day, I believe, is that China has targeted GDP growth of ‘just’ 4.5%. – 5.0% for this year. The WSJ had a very nice graph of the trajectory of Chinese GDP since 1985 showing a 4.5% outcome would be the lowest (excluding Covid) since 1991.

For a good explanation of things regarding the Chinese economy, it is always worthwhile to turn to @michaelxpettis on X and he didn’t disappoint this morning. In a nutshell, his point is that while the statement claims they will be focusing more on domestic consumption in their effort to rebalance the economy, that has been the stated aim for at least 5 years, and we know that hasn’t happened. President Xi’s problem is that if that goal were to be achieved, it would result in GDP growth somewhere on the order of 2%, and that is not acceptable. For my money, nothing has changed there. Chinese companies will still over produce, prices in China will still be pressured lower and the Chinese trade surplus will remain well in excess of $1 trillion.

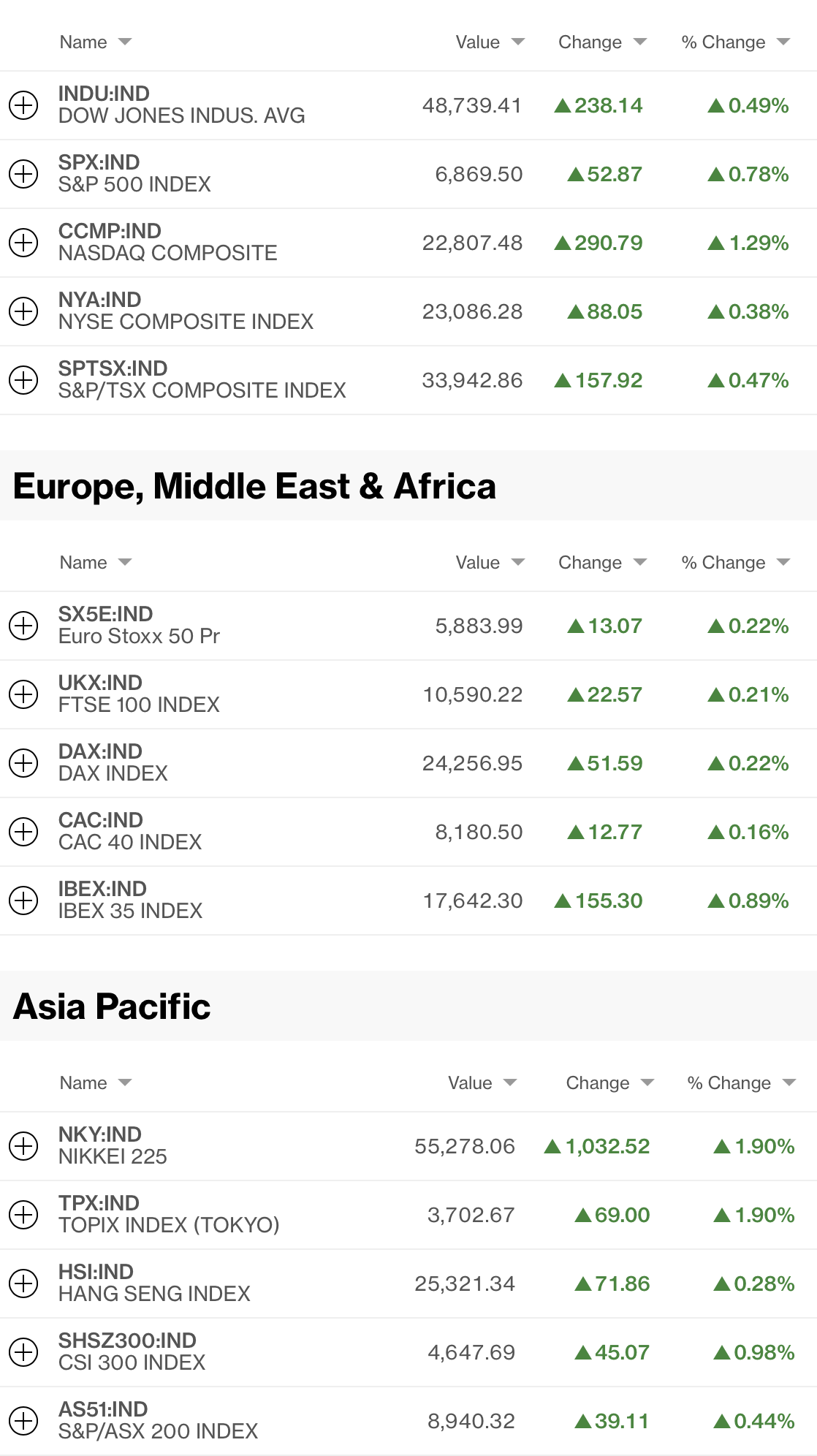

And that’s really what we have today. I am not a war correspondent, so will not be highlighting anything there. Rather, let’s turn to the markets and see what happened overnight. under the guise of a picture is worth 1000 words, I give you major equity market performance in the past 24 hours below from Bloomberg.

Of course, this doesn’t consider Korea (+9.6%) which was the biggest winner overnight, and recouped most of the previous day’s losses as per the below.

Source: finance.yahoo.com

But virtually every market in Asia rallied overnight with Taiwan, Indonesia and Thailand all higher by 2% or more. As to Europe, the euphoria is not as high, but still fear is not evident and at this hour (7:10), US futures are flat to -0.15%, so basically unchanged.

The bond market is having a tougher time around the world with Treasury yields rising yesterday by 4bps and up another 2bps this morning. European sovereign yields are all higher by between 6bps and 8bps as inflation fears start to get built into investment theses. Remember, Europe is probably the worst hit regarding the oil/LNG supply disruptions and prices there are likely to climb further than in the US or Western Hemisphere. Too, JGBs (+4bps) are feeling a little strain, despite (because of?) Ueda-san and his cronies expressing concern over the war’s impact on inflation in Japan and maintaining that a rate hike in April is still a possibility.

Speaking of inflation, the Fed’s Beige Book was released yesterday as well as a NY Fed survey on prices in their region and both pointed to much more underlying inflation than the CPI data currently implies. Wolf Richter had an excellent write-up here, and the numbers are eye opening.

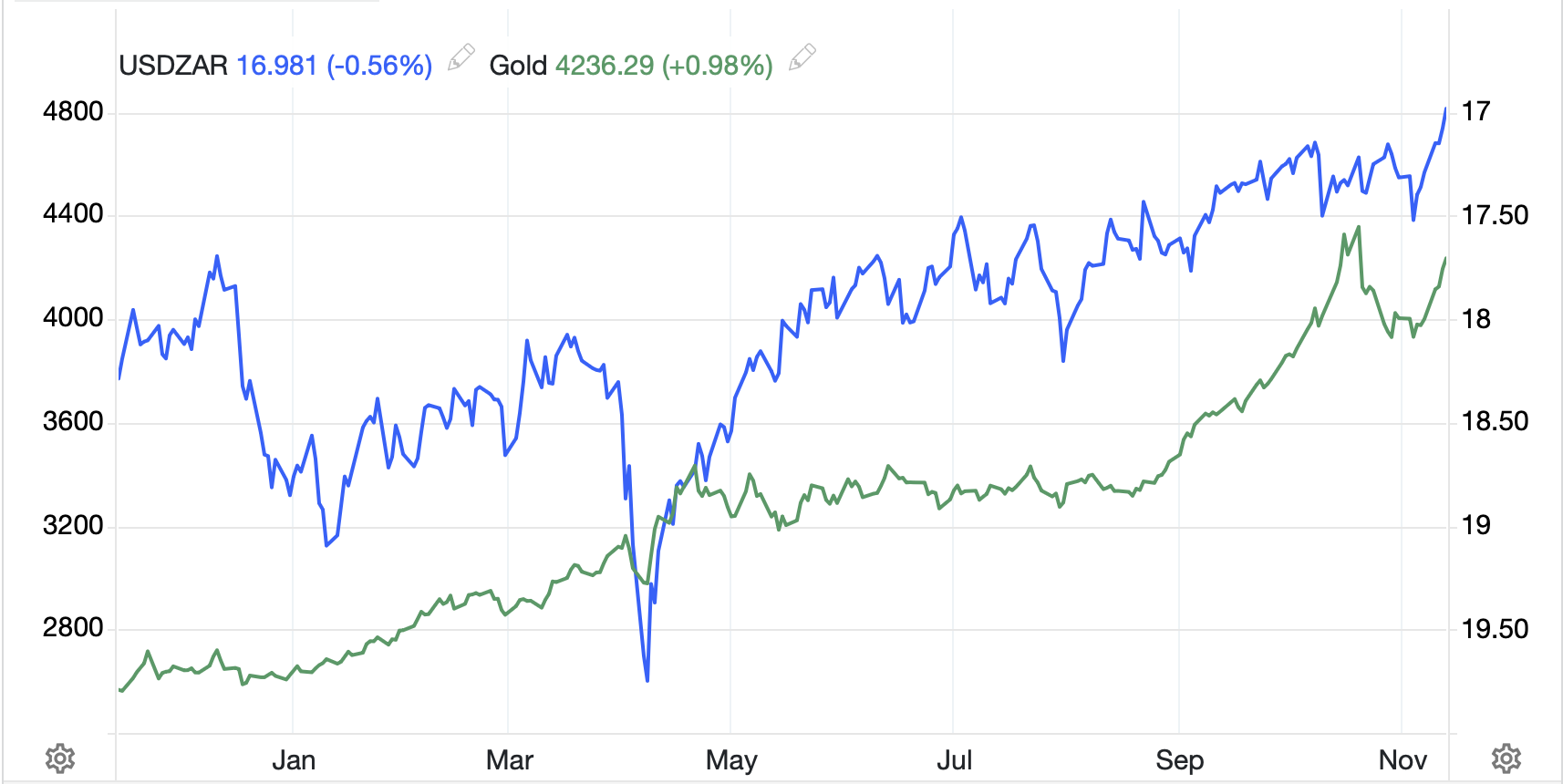

In the metals markets, gold (+0.6%) really has a remarkable amount of support under all conditions. Whether I look at a mechanically drawn trend line or the 50-day moving average, the barbarous relic remains in demand and shows no signs of breaking lower. I continue to believe that the recent volatility and liquidations were the result of leveraged traders in other products needing to sell something to make margin calls, and gold was available for the job.

Source: tradingeconomics.com

As to the other metals, silver (+1.1%) and platinum (+0.9%) are both modestly firmer while copper (-1.3%) is bucking the trend, although I see no good reason for it to decline. One interesting thing to note is that silver in the COMEX vaults continues to decline which many see as a potential point of supply issues going forward. Nothing has changed that story.

Finally, the FX markets are once again hewing toward dollars with the DXY (+0.15%) back around 99.00. The worst performer today is CLP (-1.1%) which is feeling the pressure from copper’s struggles, but ZAR (-0.9%) is also under pressure despite gold’s rebound. Interestingly, NOK (-0.2%) cannot seem to gain any ground despite oil’s rally, although arguably, the dollar itself has become a major petrocurrency with a positive correlation to oil. This space is not that interesting right now.

On the data front, I neglected to mention ADP Employment yesterday, which wound up at a better-than-expected 63K. Too, oil inventories in the US rose again last week. This morning, Initial (exp 215K) and Continuing (1850K) Claims are due as well as Nonfarm Productivity for Q4 (1.9%) and Unit Labor Costs (2.0%). But does the data really matter right now? Perhaps tomorrow’s NFP will have impact, but with the war and higher oil prices, it is very difficult for me to see a scenario where the Fed will impose itself here, not where the market will care that much, at least not the stock market. Bonds would react I suppose. But it ain’t gonna happen, so don’t worry about it.

Absent a change in the war’s current trajectory, I think investors are going to focus on trying to estimate how long oil prices will remain elevated as that is really the big question for most markets. I can only hope it doesn’t take that much longer for a conclusion.

Good luck

Adf