The future arrived yesterday

As Amazon’s cloud went astray

Along the East Coast

Much business was toast

The question is, who’s forced to pay?

Meanwhile, contradictions remain

In markets, which rose once again

Both havens and risk

Have seen, buying, brisk

I fear one side soon will feel pain

Arguably, the biggest story yesterday was the outage of Amazon Web Services on the East Coast yesterday morning with the impact dragging through the day. Apparently a supposedly minor code update had an error of some sort, and that was all it took. For every business that has been convinced that it is much cheaper and more efficient to move their computing capacity to the ‘cloud’ (and it certainly is on a daily operating basis), this is the risk being taken. Ease and convenience are wonderful when they are there, but businesses are inherently more fragile because of the movement. I guess the finance question comes down to how much do businesses save by outsourcing their computing vs. how much does it cost when those systems go down?

I am sure there will be lawsuits galore vs. Amazon for recompense. I have no idea what the AWS contract looks like, and if they leave themselves an out for situations like this, a sort of force majeure, but you can bet we will hear a lot about it going forward. Interestingly, Amazon’s stock price rose 1.6% yesterday despite the issue. Clearly nobody is worried yet.

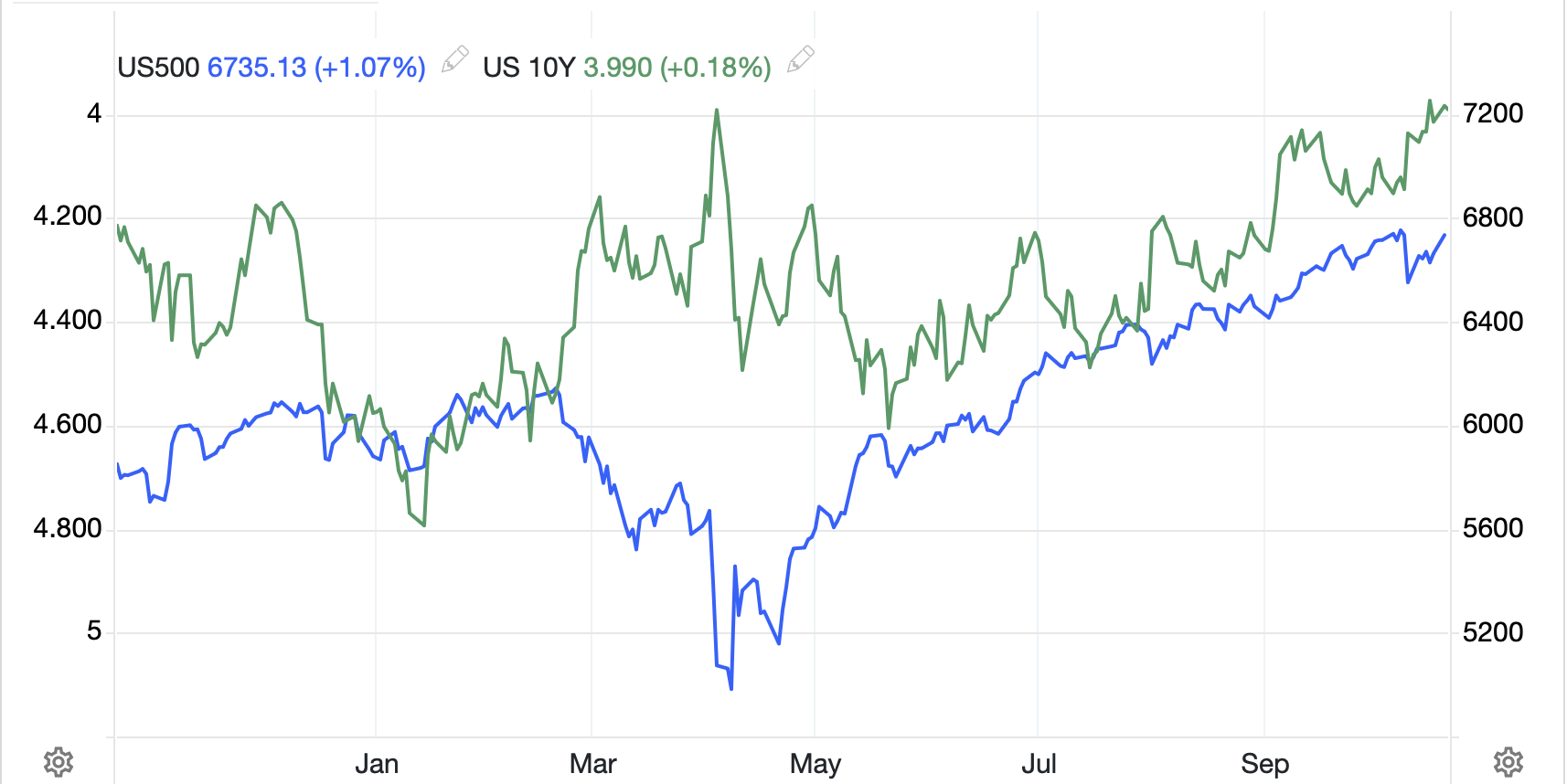

Speaking of rising stock prices, I continue to observe the ongoing equity rally alongside the ongoing bond market rally and wonder. As you can see from the chart below, for the past three to four months, the S&P 500 has rallied alongside 10-year bonds (yields falling as the price rose). For a very long time, those two markets were negatively correlated. In fact, that was the very genesis of the 60:40 portfolio being a lower risk way to remain invested.

The thesis was when stocks were rallying (the 60), things were good and while yields might rise, the gain in stocks would outperform the loss in bonds. Meanwhile, in tough times, when stocks suffered declines, bonds would rally to mitigate some of the losses. But lately, the two have traded synchronously.

Source: tradingeconomics.com

Perhaps, if we zoom out a little further, though, and look at this behavior over the past five years, we can make an observation. Here is the same chart since late 2020.

Source: tradingeconomics.com

Now, who can remember anything that changed in 2022 in the economy? That’s right, inflation re-entered the conversation in a very big way. It turns out that the 60:40 portfolio, and all its adjuncts, like risk parity and volatility targeting, were all designed when inflation was low and stable. But it appears that once inflation moves above the 3% level, the correlation that was the underlying basis of all those strategies flips. I’m sure you all remember how awful 2022 was for most investors with both stocks and bonds showing negative returns. As inflation continues to rise, and there is no reason to expect it to stop that I can see, be prepared for 2022 redux going forward. Maybe not quite as dramatic, but similar directionally.

The one thing that can change that would be the reintroduction of QE or YCC or whatever they decide to call it, as that would, by definition, prevent bonds from selling off dramatically. Of course, that will only stoke the inflationary fires, so there will still be many issues to address.

In the meantime, let’s see how markets behaved overnight, with the truly noticeable movement continuing in the precious metals space. Markets are funny things, with the ability to move very far very quickly for no apparent reason. With that in mind, a case can certainly be made that there is a serious amount of intervention in the precious metals markets lately. While I am not expert in these markets, I am well aware of the stories that there are a number of major banks, JPM among them, that are running large short positions in these metals and have been charged with preventing the prices rising too far. The concern seems to be the signal that a runaway gold or silver price would be to markets and people in general. Last Friday was a major option expiration in the SLV contract and it was remarkable to see the price of silver tumble below a number of large open strike prices. Seemingly to prevent calls to deliver. A look at the chart below, showing how quickly the price declined into the close, and it is easy to understand the genesis of those conspiracy theories.

Source: tradingeconomics.com

Yesterday, the metals all rallied nicely, but this morning, they are all, once again, under severe pressure (Au -2.2%, Ag -4.1%, Cu -1.5%, Pt -4.3%). Generally, I follow the precious metals as a signal of overall market sentiment, as I believe they are better indicators of fear than bonds. But I cannot get these movements out of my head as straight up price manipulations and so any signals we are getting are very murky. This will not last forever, but for now, I expect them to remain quite volatile. As to oil (+0.8%) it is getting a respite after a really tough run lately, with the price testing its recent lows and a growing chorus of analysts looking at the private data coming out and calling for a US recession. I don’t know about that, but things are not fantastic, that’s for sure.

But equity markets feel no pain. After yesterday’s US rally, with all three major indices rising by more than 1%, we saw gains throughout Asia (Nikkei +0.3%, Hang Seng +0.7%, CSI 300 +1.5%) as Takaichi-san was elected PM, as widely expected and investors believe that China is getting set to add fiscal stimulus as an outcome of their Fourth Plenum, with a focus on domestic demand, rather than exporting. While it is certainly possible that is what they will do, I believe this is the third time, at least, that has been the narrative, and thus far, anything they have done has been ineffectual at best. Remember, they still have a massively deflating property bubble which is weighing on the domestic economy there. In the rest of the region, almost all bourses were higher, certainly those of larger nations, with Indonesia (+1.8%) the leader.

In Europe, gains are also widespread, albeit far less impressive with the CAC (+0.4%) the leader and the rest of the major indices higher by between 0.1% and 0.2%. At this hour, (7:40) US futures are unchanged.

In the bond market, yields around the world continue to edge lower with Treasuries (-1bp) showing the way for all of Europe and for JGBs as well. it is a bit surprising that JGBs are holding in so well given Takaichi-san’s platform of more unfunded spending. Perhaps the BOJ is supporting there.

Finally, the dollar is firmer this morning rising against all its G10 counterparts with JPY (-0.8%) the laggard. It seems the FX market has listened to Takaichi’s plans even if the JGB market hasn’t. But otherwise, declines of -0.2% to -0.4% are the order of the day in the G10. In the EMG bloc, ZAR (-0.5%) is feeling the weight of the precious metals rout, while KRW (-0.65%) is under pressure as well with lingering concerns over a trade deal with the US being reached. Otherwise, though, that -0.2% level is a good proxy for the entire bloc.

The only data today is API oil inventories, and for some reason, despite the Fed’s quiet period, Governor Waller will be speaking today, although he will be making opening remarks at the Payments Innovation Conference in Washington, so will probably not focus on monetary policy.

And that’s really the story. The government remains shut down with no end to that in sight. Metals markets are a mess with stories rampant about who is manipulating them, but through it all, stocks go higher, and the dollar remains right in the middle of its recent trading range. I’m not sure what it will take to change that dynamic and I suspect it will be a gradual situation rather than a single catalyst. In the end, though, I still like the dollar better than most other currencies.

Good luck

Adf