Said Powell, there’s simply no need

To hike rates, we all have agreed

But likewise, no case

To cut, lest we face

An outcome where, jobs, we impede

Said Trump ‘bout the Strait of Hormuz

Be careful and do not confuse

Our aims in this war

As more than before

Which has been, Iran, to defuse

Now, the one thing I will say about President Trump is that strategic ambiguity is one of his strengths, as he continues to make so many seemingly contradictory statements, nobody knows what he is working to achieve. Based on the framework that Secretary Rubio laid out again yesterday:

- Destruction of Iran’s Navy

- Destruction of Iran’s Air Force

- Severe diminishment of their missile launching capability

- Destruction of their armaments factories

It is not hard to believe the US and Israel are close to their goals. However, none of this discusses Iran’s nuclear weapons program, which has clearly been a goal, nor the 440Kg of 60% enriched U308 that they retain.

Again, I wouldn’t dare claim to have any idea when this will end, but the political calculus indicates it is unlikely to go on for very much longer. However, it is not just the political calculus that implies that, but also market pricing of certain things. For instance, one of the things that initially surprised me was that Brent crude (+0.6% today) did not initially rise more rapidly than WTI (+2.0% today). After all, zero WTI transits the Strait and it is not a pricing benchmark for anything that happens over there, while Brent is the basis for all Middle Eastern oil. As the Strait of Hormuz has been effectively closed since March 4th, a look at the below chart shows that Brent did not separate itself from WTI until 2 weeks later. But last night, that spread collapsed back to its current $3/bbl, similar to the levels that preceded the onset of the war.

Source: tradingeconomics.com

One interpretation of that price action is that there is a growing belief that the Strait will reopen for transit soon. Of course, it could simply be that neither Brent nor WTI are representative of the oil grades that are impacted, and thus the large premium no longer makes sense, but given the totality of the news, I’m inclined to lean toward the former idea. Of course, both benchmarks are currently solidly above $100/bbl so still causing great pain.

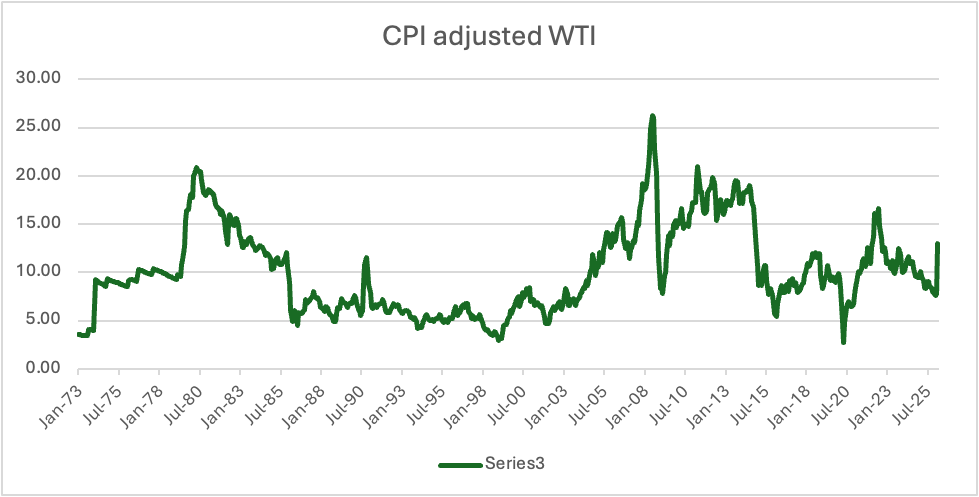

However, on this topic, as most of us live and think in a nominal world, we consider $100/bbl as extremely expensive. But if we take a moment to consider the real (inflation adjusted) price of oil, we can see in the chart below that energy remains pretty cheap, and well below levels seen ahead of the GFC or even in the wake of the Russian invasion of Ukraine.

Source: data FRED, calculations and chart, @fx_poet

My point is that over time, energy has become less of a cost in the economy, and even with the current situation, my take is the US, and frankly global, economy is quite resilient and will get through this. I’m not suggesting there won’t be some pain, just that this is not going to lead to economic Armageddon.

The other interesting story from yesterday came from Chairman Powell, who in a speech at Harvard explained there was a great deal of uncertainty currently, while admitting that the tariffs were likely a one-off modest inflation pressure. He indicated rate cuts were likely over, although hikes were possible, and then the man who printed $5 trillion to pay for every one of President Biden’s Covid and ESG bills, explained that debt is growing too fast and could be a problem going forward. And you wonder why there are those who are skeptical of his concerns over politicization of the Fed.

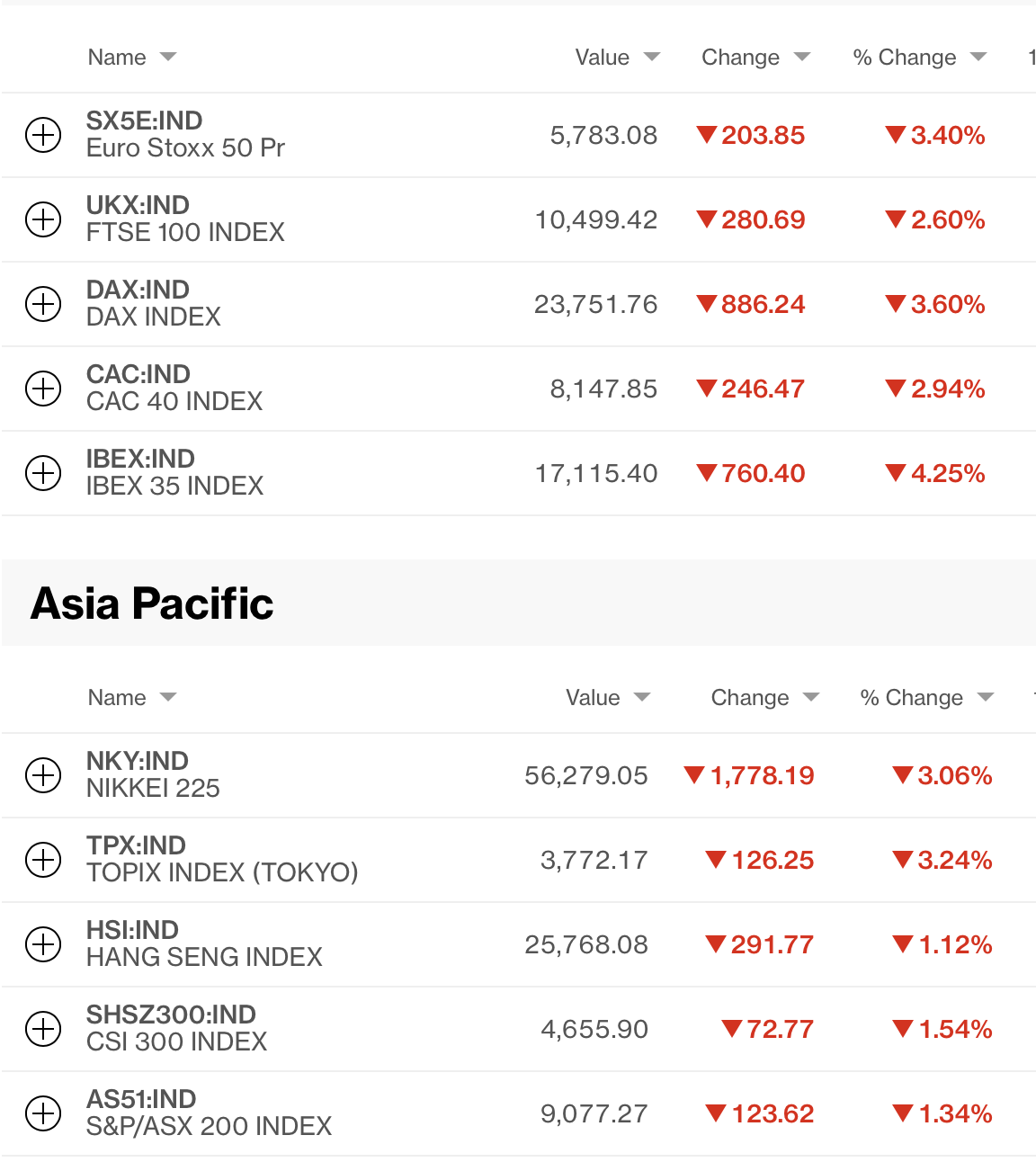

Ok, let’s turn to markets. Yesterday’s morning positivity faded all day and both the NASDAQ and S&P 500 closed lower on the session. That mostly followed in Asia with Tokyo (-1.6%), China (-0.9%), Korea (-4.3%) and Taiwan (-2.5%) all under real pressure, although HK (+0.2%) and Australia (+0.25%) managed some gains. Other regional exchanges were mixed as investors around the world are trying to figure out the next steps. At this hour (7:00), US futures are pointing solidly higher, +0.8% or so. Turnaround Tuesday? Certainly, that is the case in Europe where despite widely expected higher Flash inflation data for March, green is today’s color with gains ranging from 0.2% (CAC) to 0.5% (FTSE 100) with others somewhere in between.

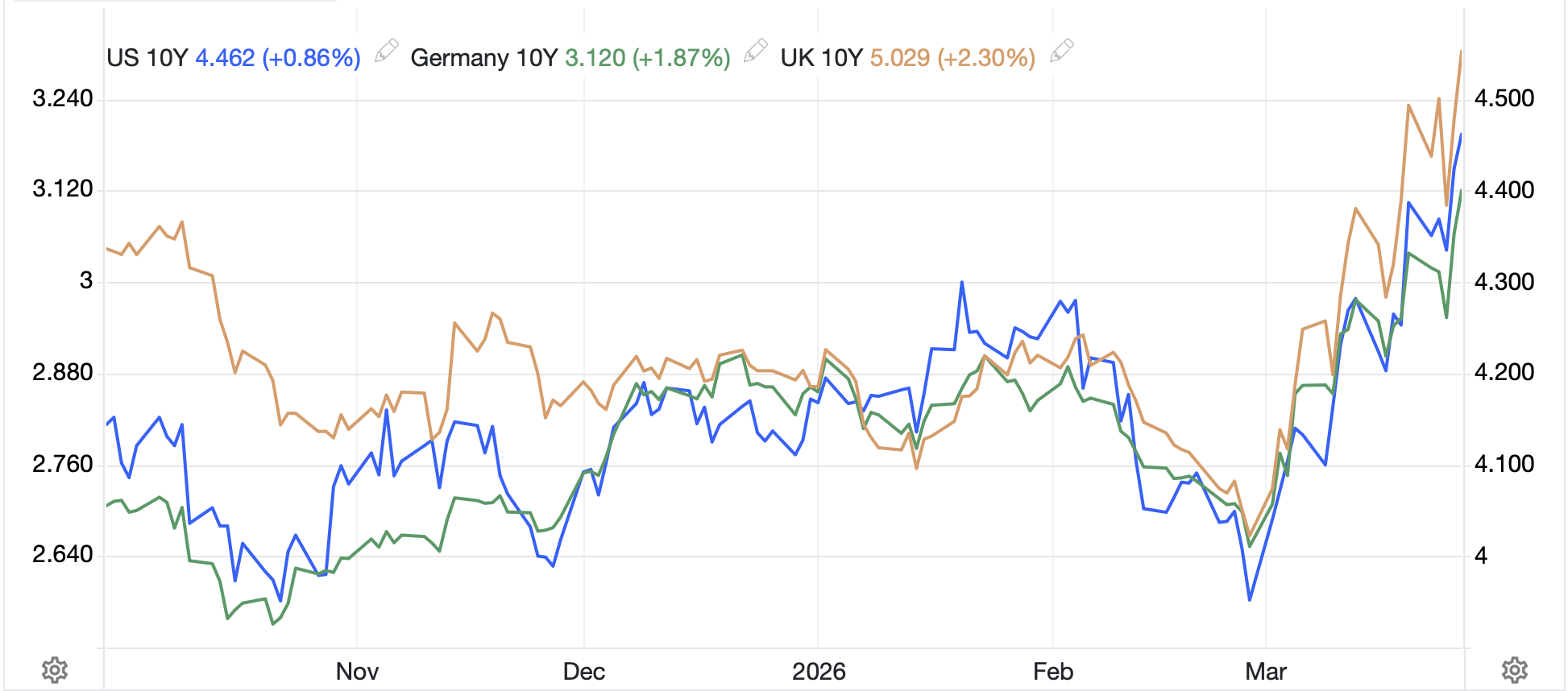

Bond investors have seemingly turned their views from inflation concerns to growth concerns, at least based on the fact that yields around the world are lower this morning than yesterday. In fact, since Friday morning, 10-year Treasury yields have fallen -14bps, including -2bps this morning. in Europe, yields did slide somewhat yesterday, about half that in the US, and this morning they are little changed throughout the continent. But we did see JGB yields slip -2bps overnight as well.

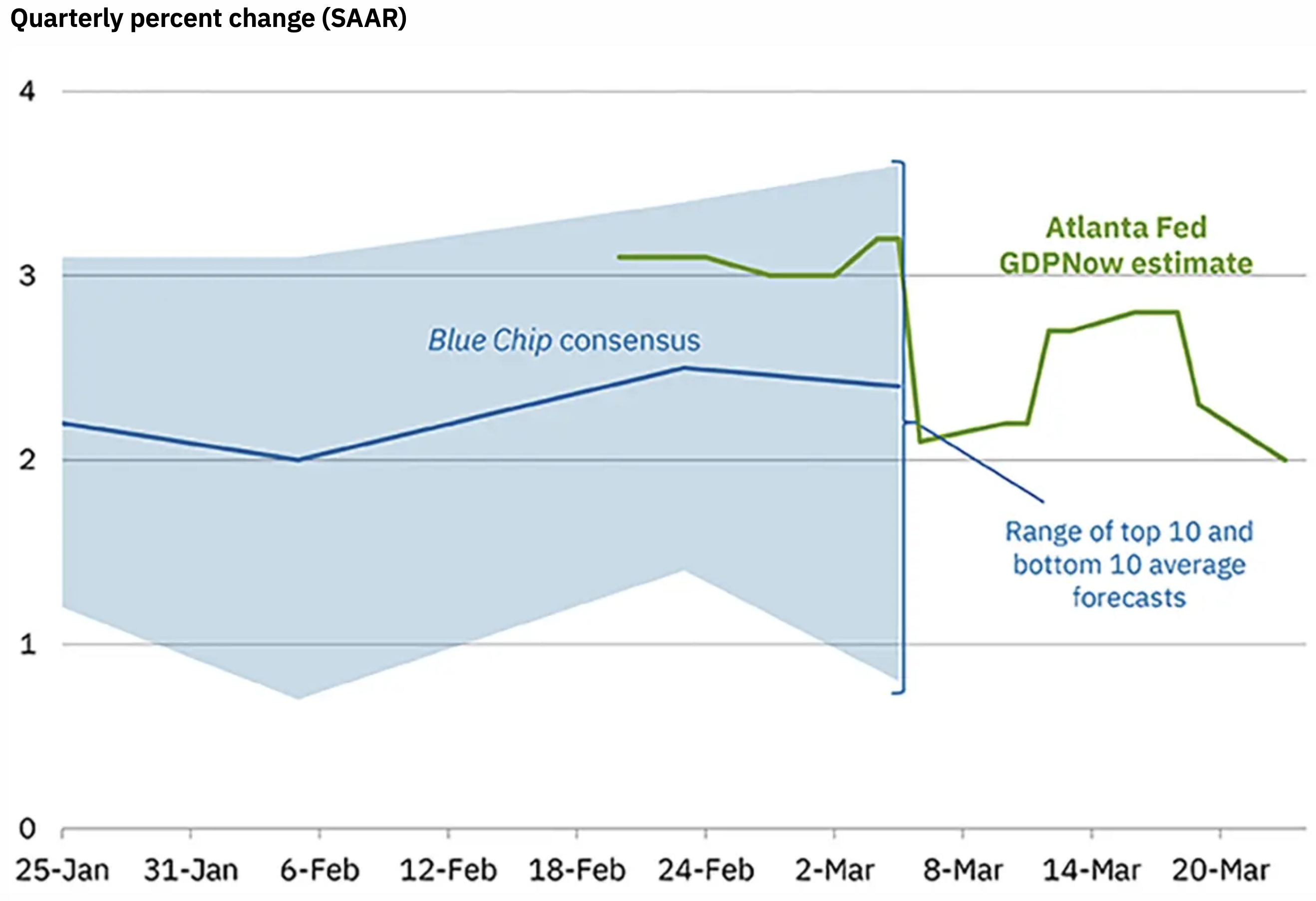

On the growth side, the Atlanta Fed’s GDPNow is running at 2.0% for Q1, well below its first readings from before the Iran activity, although still in decent shape. The next update comes tomorrow, so will be interesting to see. And, of course, the payroll report on Friday will be critical for that reading. It is, though, still well above the Blue Chip Consensus readings.

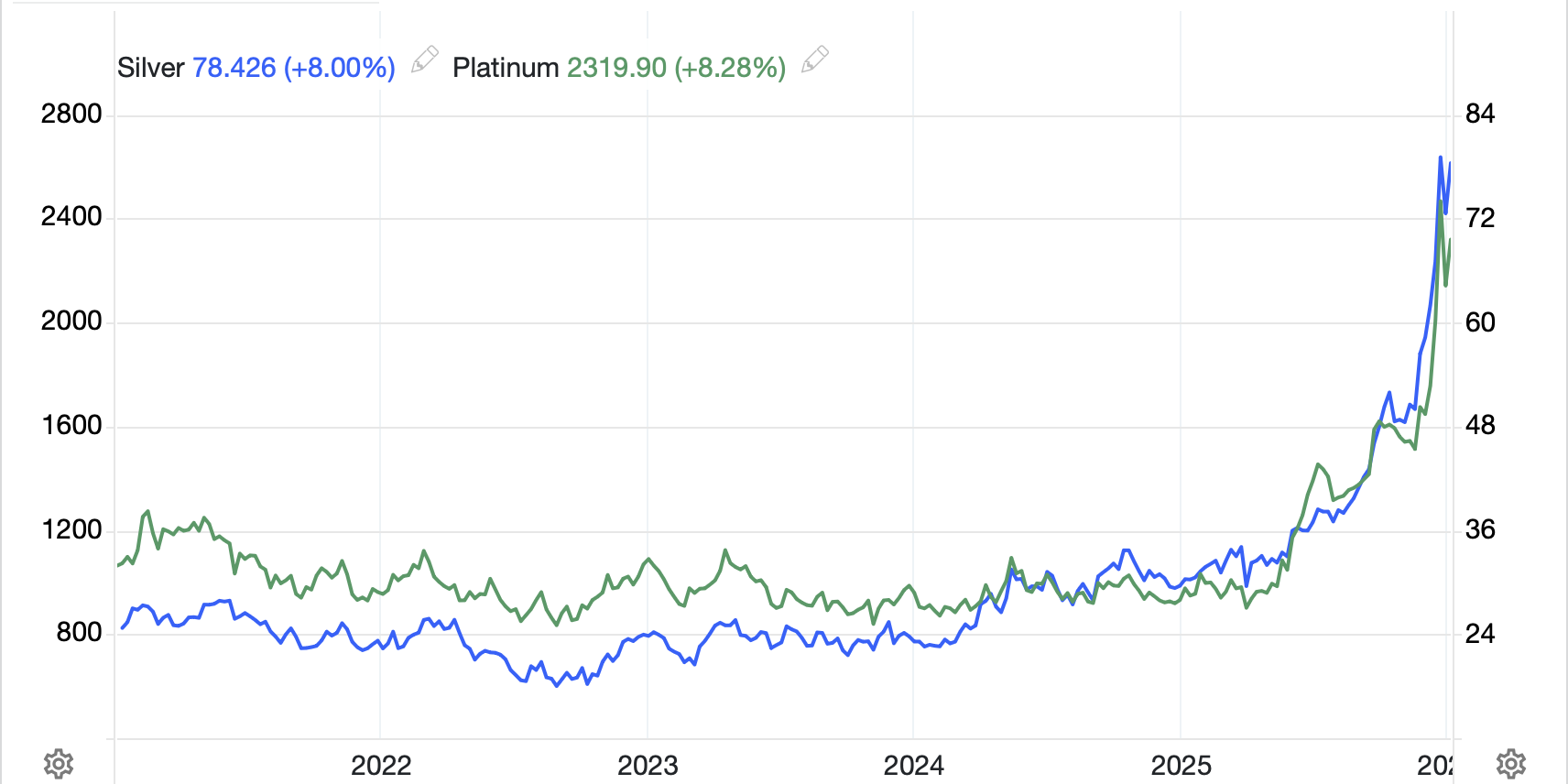

We’ve discussed oil, but a quick peek at precious metals shows they are regaining their luster, with gold (+0.8%) and silver (+3.6%) both nicely higher this morning. As this price action continues, with the current price more than 10% above the spike low from March 23rd, I believe whatever was driving things during the first part of the war, may now have passed.

Finally, the dollar is little changed this morning, but sitting on its recent highs with the DXY at 100.53 as I type. Here’s the thing about the current level. As you can see from the long-term chart below, while during the first 4 months of 2025, the dollar did decline sharply, about 10%, the longer history shows that the current level has acted as support for a very long time. As well, if you take the really long view, we are within spitting distance of the DXY’s average since the 1970’s.

Source: tradingeconomics.com

All I’m saying is the dollar is neither strong nor weak right now, it just is. It is, though, worth looking at the yen (0.0%) which pushed back to just below 160 during yesterday’s session and got more jawboning from Mimura-san, the Vice Finance Minister for International Affairs (aka Mr Yen) who explained they are ready to take “decisive action” against speculative moves. But otherwise, this morning’s session is unremarkable with only KRW (-0.6%) continuing to suffer from the energy issues there.

On the data front, we get Case Shiller Home Prices (exp +1.3%) and then Chicago PMI (55.0) and perhaps most importantly, the JOLTs Job Openings (6.92M) report at 10:00. There are two more Fed speakers, Goolsbee and Barr, but with Powell just having confirmed no moves are coming soon, what can they possibly add to the story?

The war and its headlines remain the key drivers and I don’t see anything changing that dynamic for now. I wonder if markets are prepared for an announcement that it is ending and Iran has come to terms. I’m not suggesting that is the likely outcome, just that it would be the biggest surprise, I believe. In the meantime, there are precious few reasons to sell the dollar outright, that’s for sure.

Good luck

Adf