The barbarous relic is soaring

As Stephen Miran is imploring

That Fed funds should be

At 2, don’t you see

An idea that Trump is adoring

But what else would happen if Steve

Is Fed Chair, when Powell does leave?

At first stocks would rally

Though bonds well could valley

And ‘flation? There’d be no reprieve

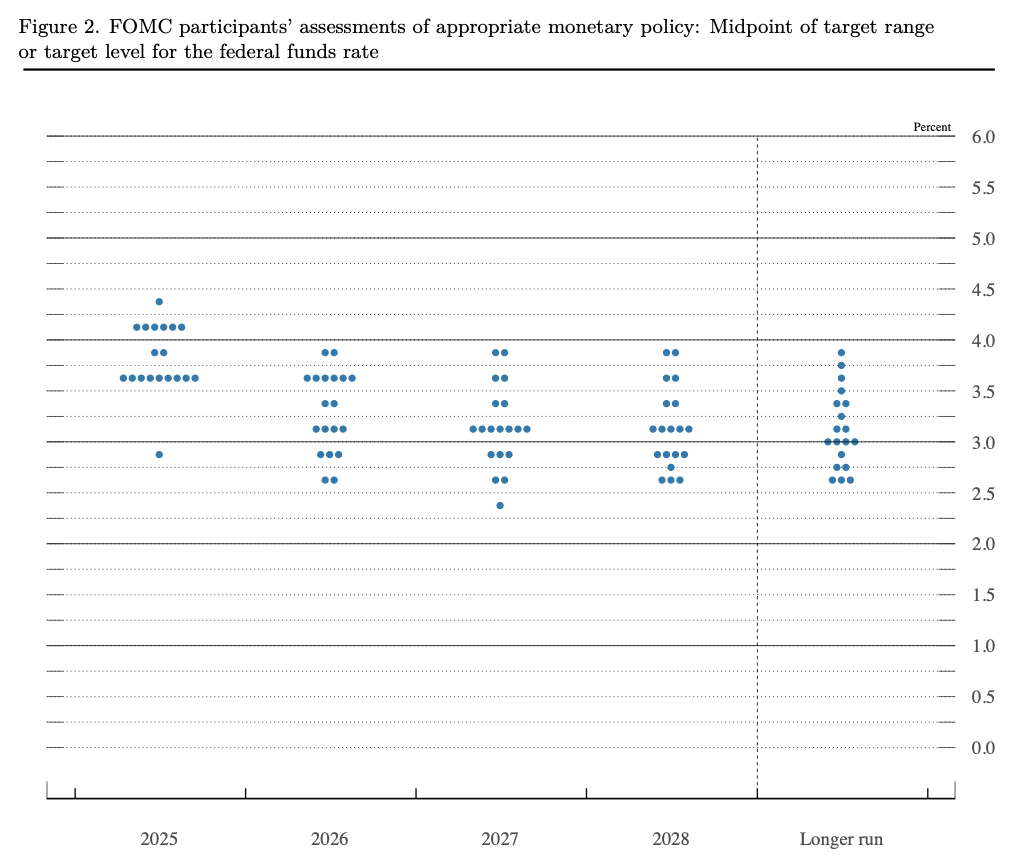

Arguably, the most interesting news in the past twenty-four hours has been the speech given by the newest FOMC member, Stephen Miran, where he explained his rationale for interest rates going forward. There is no point going into the details of the argument here, but the upshot is he believes that 2.0% is the proper current setting for Fed funds based on his interpretation of the Taylor Rule. That number is significantly lower than any other estimate I have seen from other economists, but then, the track record of most economists hasn’t been that stellar either. Who am I to say he is right or wrong?

Well, actually, I guess that’s what I do, comment from the cheap seats, and FWIW, I suspect that number is far too low. But forgetting economists’ views, perhaps the best arbiter of those views is the market, and in this case, the gold market. With that in mind, I offer the following chart from tradingeconomics.com:

Those are weekly bars in the chart which shows us that the price of gold has risen for the past five weeks consecutively, during which time it has gained more than 14% on an already elevated price given the rally that began back in the beginning of 2024. Today’s 1% rise is just another step toward what appears to be much higher levels going forward.

Why, you may ask, is gold rallying like this? The thought process, which Miran defined for us all yesterday, is that he is in line to be the next Fed chair when Powell leaves, and so his effort will be to cut rates as quickly as possible to that 2% level. Of course, the risk is inflation readings will continue to rise while the Fed is cutting. If that occurs, and I suspect it is quite likely, then fears about a weaker dollar are well founded (that has been my view all along, aggressive rate cuts by the Fed will undermine the dollar in the short-run, longer term is different) and gold and other commodities will benefit greatly. As to bonds…well here the picture is likely to be pretty ugly, with yields rising. In fact, I wouldn’t be surprised to see 10-year Treasury yields head back toward 5.0% at which point the Treasury and the Fed, working hand in hand, will cap them via some combination of QE and YCC.

Of course, this is just one hypothesis based on what we know today and won’t happen until Q2 or Q3 next year. Gold is merely sniffing out the probability of this outcome. Remember, too, that the Trump administration has been quite unpredictable in its policy moves, and so none of this is a sure thing.

As an aside, given the inherent dovishness of the current make up of Fed governors, it would seem that a Miran chairmanship with a distinctly dovish bent will not have much problem getting the rest of the FOMC to go along, except perhaps for a few regional presidents. And that doesn’t even assume that Governor Cook is forced out. After all, she is a raging dove, just a political one that doesn’t want to give President Trump what he wants.

And before I start in on the overnight activity, here is another question I have. Generally, economists are much more in favor of consumption taxes (that’s why they love a VAT) rather than income taxes and it makes sense, in that consumption taxes offer folks the choice to pay the tax by consuming or not. If that is the case, why are these same economists’ hair all on fire about the tariffs, which they plainly argue is a consumption tax? I read that the US is set to generate $400 billion in tariff revenue this year which would seem to go a long way to offsetting no tax on tips and other tax cuts from the OBBB. I would expect that if starting from scratch, an honest economist, with no political bias (if such a person were to exist) would much rather see lower income tax rates and higher consumption tax rates. Alas, that feels like a conversation we will never be able to have.

Anyway, on to markets where yesterday saw yet another set of new all-time highs in the US across all the major indices with futures this morning slightly higher yet again. Japan was closed for Autumnal Equinox Day, while the rest of the region had a mixed performance. China (-0.1%) and HK (-0.7%) suffered on continuing concerns over the Chinese economy with news that banks which are still dealing with property loan problems are now beginning to see consumer loan defaults as well. Elsewhere Korea and Taiwan both rallied nicely, following the tech-led US while India suffered a bit on the H1-B visa story with the rupee falling to yet another historic low (dollar high) now pushing 89.00. There were some other laggards as well (Thailand, Philippines) but most of the rest were modestly higher.

In Europe, green is the theme with the CAC (+0.7%) leading the way while the DAX (+0.2%) and IBEX (+0.3%) are not as positive. Ironically, Flash PMI data showed that French activity was lagging the most, with both manufacturing (48.1) and services (48.9) below the 50.0 breakeven level and much worse than expected. It seems the fiscal issues in France are starting to feed into the private sector. As to the UK, weaker Flash PMI data there has resulted in no change in the FTSE 100 as it appears caught between inflation worries and growth worries.

In the bond market, Treasury yields which rose 2bps yesterday have slipped by -1bp this morning while continental sovereigns are all essentially unchanged. The one outlier here is the UK where gilts (-3bps) are rallying on hopes that the PMI data will lead to easier monetary policy.

Elsewhere in the commodity markets, oil (+1.1%) is bouncing from its recent lows but has not made much of a case to breech its recent $61.50/$65.50 trading range as per the below.

Source: tradingeconomics.com

The other precious metals are rocking alongside gold (Ag +0.7%, Pt +2.6%) with silver having outperformed gold since the beginning of the year by nearly 10 percentage points. Oh, and platinum has risen even more, more than 63% YTD!

Finally, the dollar is basically unchanged this morning, with marginal movement against most of its counterparties. There are only two outliers, SEK (+0.5%) which rallied despite (because of?) the Riksbank cutting their base rate by 25bps in a surprise move. However, the commentary indicated they are done cutting for this cycle, so perhaps that is the support. On the other side of the coin, INR (-0.5%) has been weakening steadily with the H1-B visa story just the latest chink in the armor there. PM Modi is walking a very narrow tight rope to appease President Trump while not upsetting Presidents Putin and Xi. His problem is that he needs both cheap oil and the US market for the economy to continue its growth, and there is a great deal of tension in his access to both simultaneously. But away from those currencies, +/- 0.1% describes the session.

On the data front, today brings the Flash PMI data (exp 52.0 Manufacturing, 54.0 Services) and the Richmond Fed Manufacturing Index (-5.0). remember, the Philly Fed Index registered a much higher than expected 23.2 last week, so the manufacturing story is clearly not dead yet.

Arguably, though, of far more importance than those numbers will be Chairman Powell’s speech at 12:35 this afternoon on the Economic Outlook in Providence, RI. All eyes and ears will be on his current views regarding the employment situation and inflation, especially in light of Miran’s speech yesterday.

While the gold market is implying our future is inflationary and fiat currencies will weaken, the FX market has not yet taken that idea to extremes. Any dovishness by Powell, which given the lack of data since we heard from him last week would be a surprise, will have an immediate impact. However, I suspect he will maintain the relatively hawkish tone of the press conference and not impact markets much at all.

Good luck

Adf