There once was a time when the Fed

When meeting, and looking ahead

All seemed to agree

The future they’d see

And wrote banal statements, when read

But this time is different, it’s true

Though those words most folks should eschew

‘Cause nobody knows

Which way the wind blows

As true data’s hard to construe

So, rather than voting as one

Three members, the Chairman, did shun

But crazier still

The dot plot did kill

The idea much more can be done

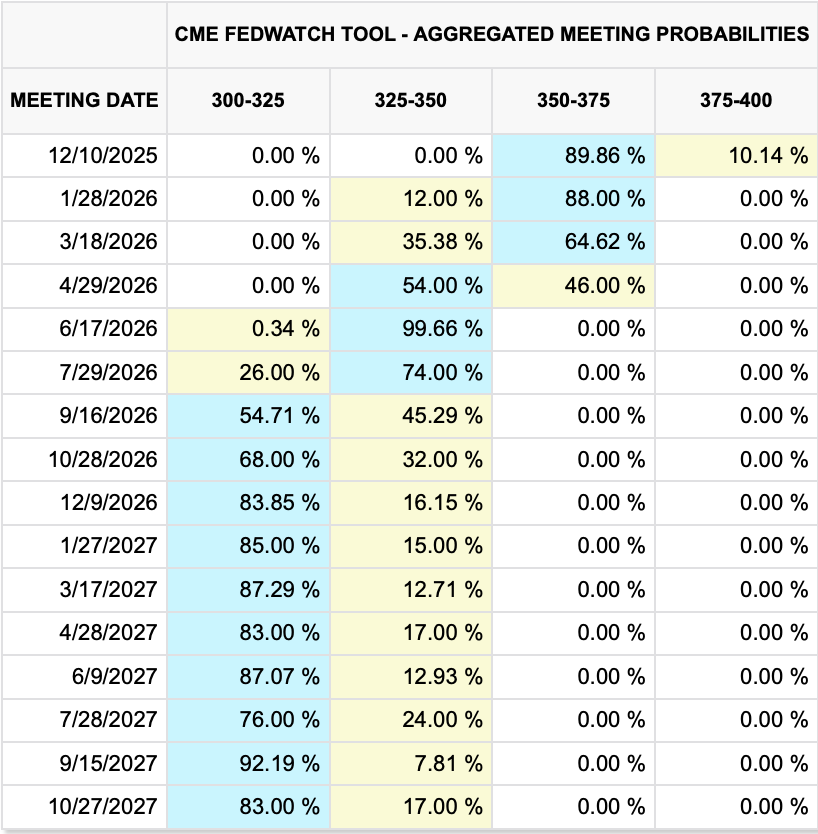

I think it is appropriate to start this morning’s discussion with the dot plot, which as I, and many others, expected showed virtually no consensus as to what the future holds with respect to Federal Reserve monetary policy. For 2026, the range of estimates by the 19 FOMC members is 175 basis points, the widest range I have ever seen. Three members see a 25bp hike in 2026 and one member (likely Governor Miran) sees 150bps of cuts. They can’t all be right! But even if we look out to the longer run, the range of estimates is 125bps wide.

Personally, I am thrilled at this outcome as it indicates that instead of the Chairman browbeating everyone into agreeing with his/her view, which had been the history for the past 40 years, FOMC members have demonstrated they are willing to express a personal view.

Now, generally markets hate uncertainty of this nature, and one might have thought that equity markets, especially, would be negatively impacted by this outcome. But, since the unwritten mandate of the Fed is to ensure that stock markets never decline, they were able to paper over the lack of consensus by explaining they will be buying $40 billion/month of T-bills to make sure that bank reserves are “ample”. QT has ended, and while they will continue to go out of their way to explain this is not QE, and perhaps technically it is not, they are still promising to pump nearly $500 billion /year into the economy by expanding their balance sheet. One cannot be surprised that initially, much of that money is going to head into financial markets, hence today’s rally.

However, if you want to see just how out of touch the Fed is with reality, a quick look at their economic projections helps disabuse you of the notion that there is really much independent thought in the Marriner Eccles Building. As you can see below, they continue to believe that inflation will gradually head back to their target, that growth will slow, unemployment will slip and that Fed funds have room to decline from here.

I have frequently railed against the Fed and their models, highlighting time and again that their models are not fit for purpose. It is abundantly clear that every member has a neo-Keynesian model that was calibrated in the wake of the Dot com bubble bursting when interest rates in the US first were pushed down to 0.0% while consumer inflation remained quiescent as all the funds went into financial assets. One would think that the experience of 2022-23, when inflation soared forcing them to hike rates in the most aggressive manner in history, would have resulted in some second thoughts. But I cannot look at the table above and draw that conclusion. Perhaps this will help you understand the growth in the meme, end the fed.

To sum it all up, FOMC members have no consensus on how to behave going forward but they decided that expanding the balance sheet was the right thing to do. Perhaps they do have an idea, but given inflation is showing no signs of heading back to their target, they decided that the esoterica of the balance sheet will hide their activities more effectively than interest rate announcements.

One of the key talking points this morning revolves around the dollar in the FX markets and how now that the Fed has cut rates again, while the ECB is set to leave them on hold, and the BOJ looks likely to raise them next week, that the greenback will fall further. Much continues to be made of the fact that the dollar fell about 12% during the first 6 months of 2025, although a decline of that magnitude during a 6-month time span is hardly unique, it was the first such decline that happened during the first 6 months of the year, in 50 years or so. In other words, much ado about nothing.

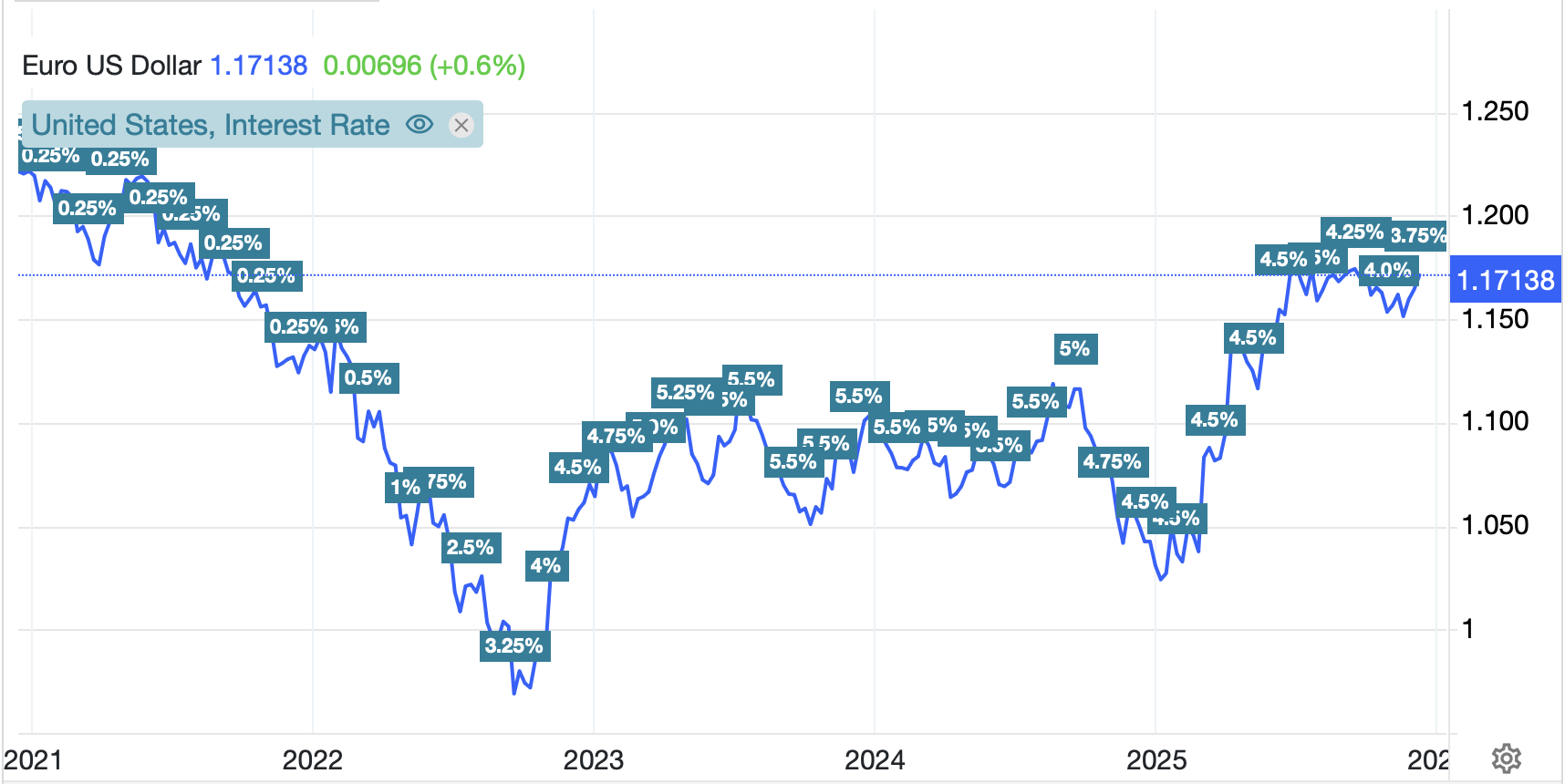

The latest spin, though, is look for the dollar to decline sharply after the rate cut. I have a hard time with this concept for a few reasons. First, given the obvious uncertainty of future Fed activity, as per the dot plot, it is unclear the Fed is going to aggressively cut rates from this level anytime soon. And second, a look at the history of the dollar in relation to Fed activity doesn’t really paint that picture. The below chart of the euro over the past five years shows that the single currency fell during the initial stages of the Fed’s panic rate hikes in 2022 then rallied back sharply as they continued. Meanwhile, during the latter half of 2024, the dollar rallied as the Fed cut rates and then declined as they remained on hold. My point is, the recent history is ambiguous at best regarding the dollar’s response to a given Fed move.

Source: tradingeconomics.com

I have maintained that if the Fed cuts aggressively, it will undermine the dollar. However, nothing about yesterday’s FOMC meeting tells me they are about to embark on an aggressive rate cutting binge.

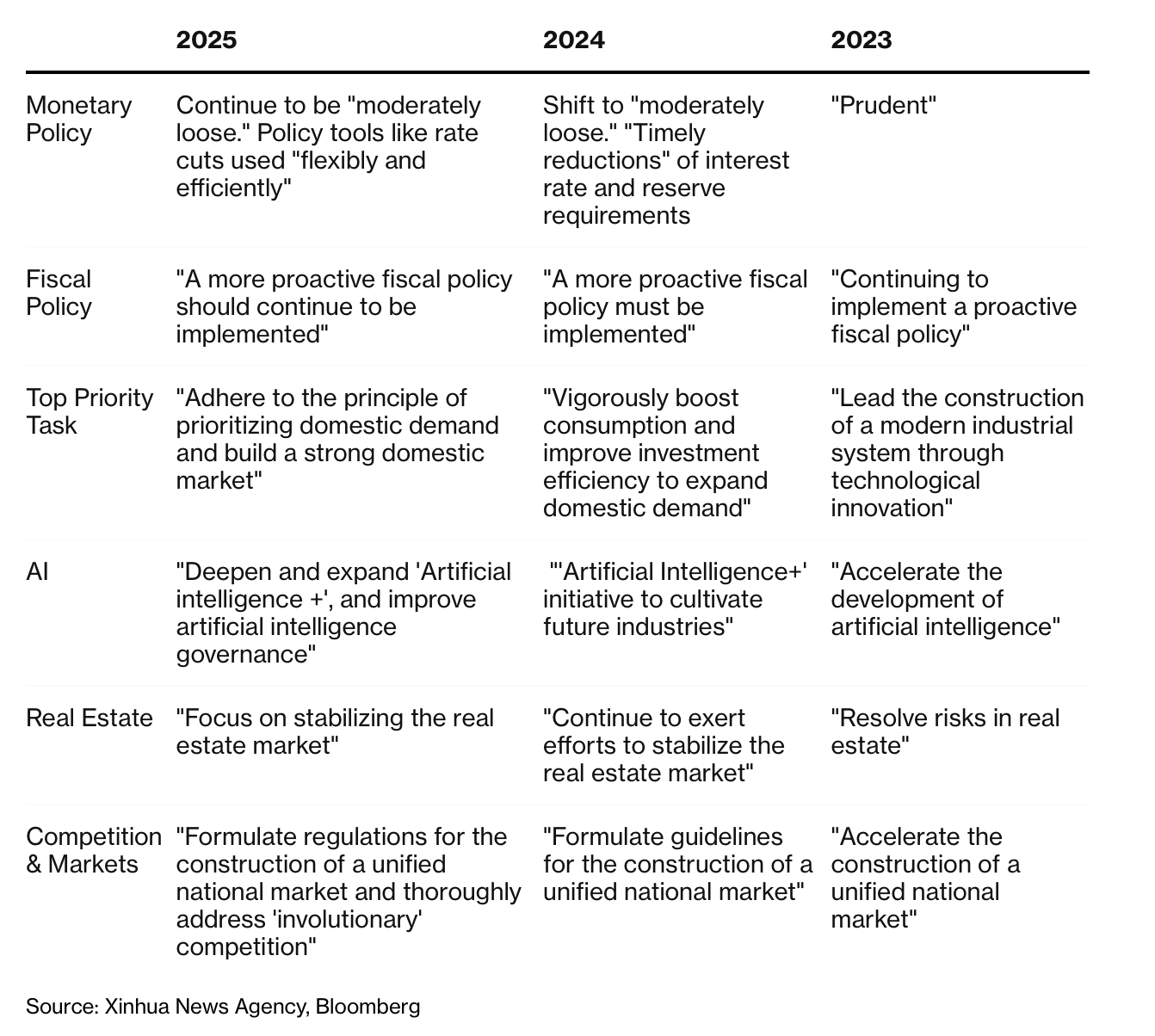

The other noteworthy story this morning is the outcome from China’s Central Economic Work Conference (CEWC). I have described several times that the President Xi’s government claims they are keen to help support domestic consumption and the housing market despite neither of those things having occurred during the past several years. Well, Bloomberg was nice enough to create a table highlighting the CEWC’s statements this year and compare them to the past two years. I have attached it below.

In a testament to the fact that bureaucrats speak the same language, no matter their native tongue, a look at the changes in Fiscal Policy or Top Priority Task, or even Real Estate shows that nothing has changed but the order of the words. The very fact that they need to keep repeating themselves can readily be explained by the fact that the previous year’s efforts failed. Why will this time be different?

Ok, a quick tour of markets. Apparently, Asia was not enamored of the FOMC outcome with Tokyo (-0.9%) and China (-0.9%) both sliding although HK managed to stay put. Elsewhere in the region, both Korea (-0.6%) and Taiwan (-1.3%) were also under pressure as most markets here were in the red. The exceptions were India, Malaysia and the Philippines, all of which managed gains of 0.5% or so.

In Europe, things are a little brighter with modest gains the order of the day led by Spain (+0.5%) and France (+0.4%) although both Germany and the UK are barely higher at this hour. There was no data released in Europe this morning although the SNB did meet and leave rates on hold at 0.0% as universally expected. There has been a little bit of ECB speak, with several members highlighting that ECB policy is independent of Fed policy but that if Fed cuts force the dollar lower, they may feel the need to respond as a higher euro would reduce inflation. Alas for the stock market bulls in the US, futures this morning are pointing lower led by the NASDAQ (-0.7%) although that is on the back of weaker than expected Oracle earnings results last night. Perhaps promising to spend $5 trillion on AI is beginning to be seen as unrealistic, although I doubt that is the case 🤔.

Turning to the bond market, Treasury yields have slipped -2bps overnight after falling -5bps yesterday. Similar price action has been seen elsewhere with European sovereign yields slipping slightly and even JGB yields down -2bps overnight. Personally, I am a bit confused by this as I have been assured that the Fed cutting rates in this economy would result in a steeper yield curve with long-dated rates rising even though the front end falls. Perhaps I am reading the data wrong.

In the commodity markets, the one truth is that there are no sellers in the silver market. It is higher by another 0.5% this morning and above $62/oz as whatever games had been played in the past to cap its price seem to have fallen apart. Physical demand for the stuff outstrips new supply by about 120 million oz /year, and new mines are scarce on the ground. This feels like there is further room to run.

Source: tradingeconomics.com

As to the rest of the space, gold (-0.2%) which had a nice day yesterday is consolidating, as is copper. Turning to oil (-1.1%) it continues to drift lower, dragging gasoline along for the ride, something that must make the president quite happy. You know my views here.

As to the dollar writ large, while it sold off a bit yesterday, as you can see from the below DXY (-0.3%) chart, it is hardly making new ground, rather it is back to the middle of its 6-month range.

Source: tradingeconomics.com

This morning more currencies are a bit stronger but in the G10, CHF (+0.45%) is the leader with everything else far less impactful. And on the flip side, INR (-0.7%) has traded to yet another historic low (USD high) as the new RBI governor has decided not to waste too much money on intervention. Oh yeah, JPY (+0.2%) has gotten some tongues wagging as now that the Fed cut and the BOJ is ostensibly getting set to hike, there is more concern about the unwind of the carry trade. My view is, don’t worry unless the BOJ hikes 50bps and promises a lot more on the way. After all, if the Fed has finished cutting, something that cannot be ruled out, this entire thesis will be destroyed.

On the data front, Initial (exp 220K) and Continuing (1950K) Claims are coming as well as the Trade Balance (-$63.3B). There are no Fed speakers on the docket, but I imagine we will hear from some anyway, as they cannot seem to shut up.

It would not surprise me to see the dollar head toward the bottom of this trading range, but I think we need a much stronger catalyst than uncertainty from the Fed to break the range.

Good luck

Adf