The temperature’s starting to fall

With Israel and Iran’s brawl

On hold for the moment

Though either could foment

Resumption, and break protocol

But that truce combined with the news

That Trump’s team are pushing full schmooze

On trade, has the markets

Increasing their bull bets

While skeptics are singing the blues

President Trump is having a pretty remarkable week. The successful attack and destruction of Iran’s nuclear enrichment facilities combined with the news that the US and China have agreed the details of the trade framework that was outlined in Geneva and followed up in London has market participants feeling a lot better about the world this morning. Add to that the news that a particularly onerous part of the BBB, Section 899, which was nicknamed the Revenge clause for its tax targeting anybody from nations that imposed excess taxes on US companies internationally, being stripped after negotiations with European leaders, and the fact that NATO has gone all-in on increasing their spending, and Mr Trump must be feeling pretty good this morning. Certainly, most markets are feeling that, except those that thrive on chaos and fear, like precious metals.

In fact, this morning it seems that the entire discussion is a rehash of what has occurred all week with very little new added to the mix. Data from the US yesterday was mixed, with Claims a bit softer and Durable Goods quite strong while the third look at Q1 GDP was revised lower on more trade data showing imports were greater than first measured while Consumer Spending and Final Sales were a bit weaker than expected. Net, there was not enough to push a view of either substantial strength or weakness in the economy, so investors and their algorithms continue to buy shares.

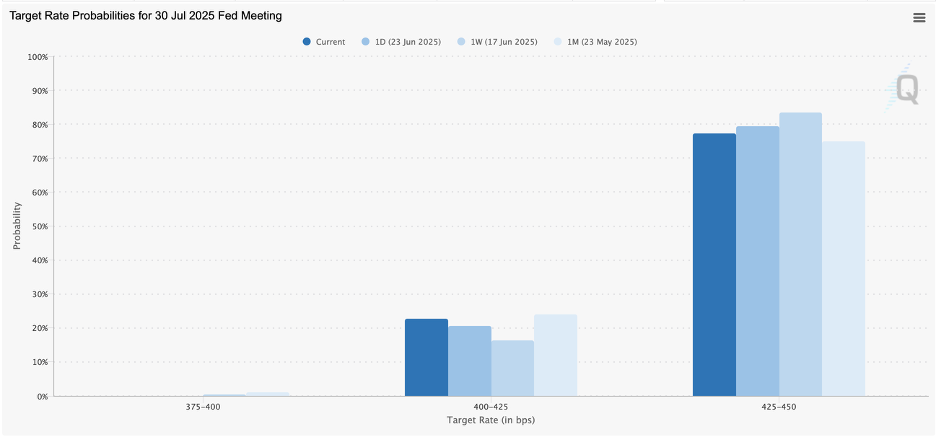

The other story that continues to get airplay is the pressure on Chairman Powell and questions about whether at the July meeting Fed governors are going to vote against the Chairman. Apparently, it has been 32 years since that has occurred (and you thought they were actual votes!) and the punditry is ascribing the dissent to politics, not economics. It should, of course, be no surprise that there is a political angle as there is a political angle to every story these days, but the press is particularly keen to point out that the two most vocal Fed governors discussing rate cuts were appointed by Trump.

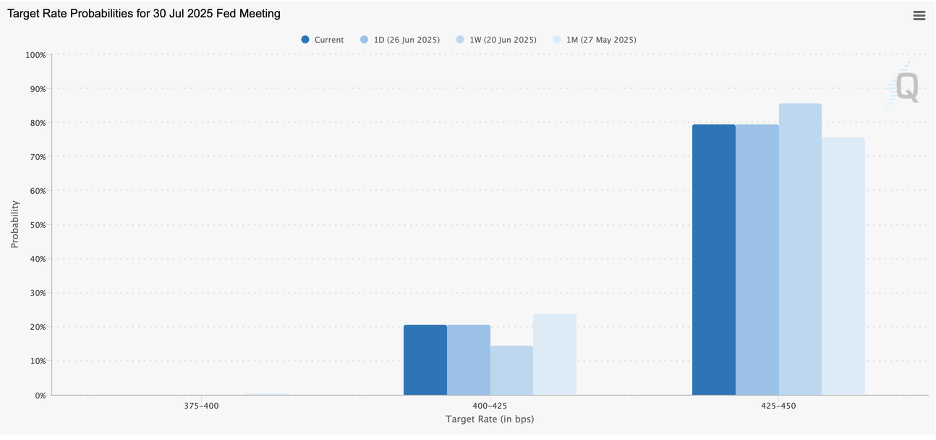

However, despite all the talk, the futures market does not appear to have adjusted its opinion all that much as evidenced by the CME chart of probabilities below. In fact, over the past month, the probability of a cut has declined slightly. Rather, I would contend that on a slow news Friday, the punditry is looking for a story to get clicks.

The last story of note is about the dollar and its ongoing weakness. This is an extension of the Fed story as there is alleged concern that if the Fed is perceived to lose some of its independence, that will be a negative for the dollar in its own right, as well as the fact that the loss of independence would be confirmed by a rate cut when one is not necessary (sort of like last autumn prior to the election. Interestingly, I don’t recall much discussion about the Fed’s loss of independence then.)

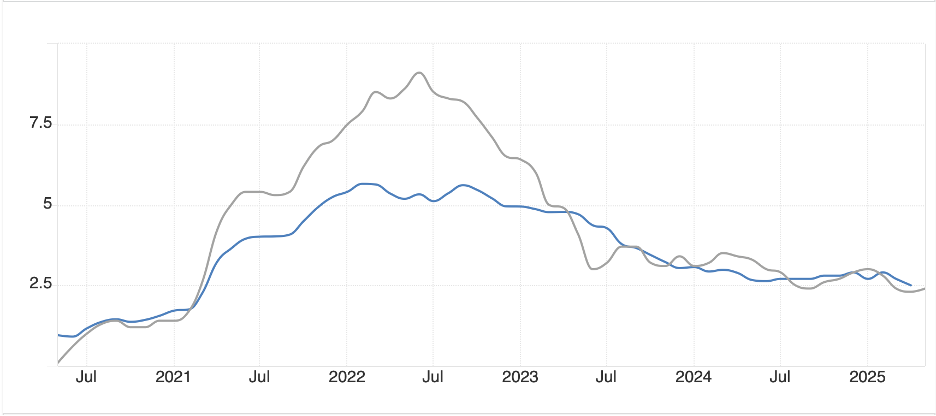

But, in fairness, the dollar has continued to decline with the euro trading to its highest level, above 1.17, in nearly four years. It is hard to look at the story in Europe and think, damn, what a place to invest with high energy costs and massive regulatory impediments, so it is reasonable to accept that what had been a very long dollar position is getting unwound. But look at the next two charts (source: tradingeconomics.com) of the euro, showing price action for one year and for five years, and more importantly notice the trend lines that the system has drawn. There is no doubt the dollar is under pressure right now, but I am not in the camp that believes this is the beginning of the end of the dollar’s global status. Remember, too, that President Trump would like to see the dollar soften to help the export competitiveness of the US, and so I would not expect to hear anything from the Treasury on the matter.

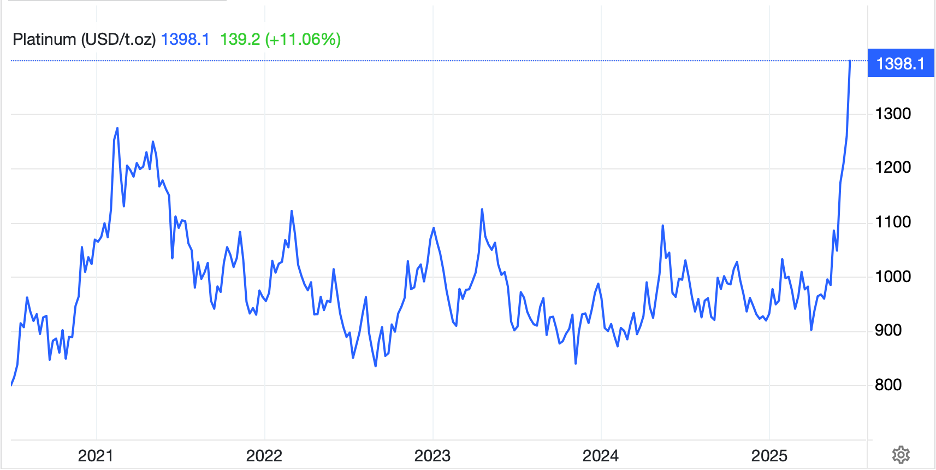

However, while these medium and long-term trends are clear, the overnight session was far less exciting with the largest move in any major currency the ZAR (+0.5%) which is despite the decline in gold and platinum prices. Otherwise, today’s movement is basically +/- 0.2% across both G10 and EMG currencies.

Speaking of the metals, though, they are taking it on the chin this morning as we approach month end and futures roll action. Gold (-1.3%), silver (-1.7%), copper (-0.9%) and platinum (-4.4%) are all under pressure, although all remain significantly higher YTD. However, to the extent that they represent a haven and the fact that havens seem a little less necessary this morning seems to be the narrative driver adding to the month end positioning. Meanwhile, oil (+0.5%) continues to bounce ever so slowly off the lows seen immediately in the wake of the bombing attacks.

Circling back to equity markets, after a nice day in the US yesterday, with gains across the board approaching 1% and the S&P 500 pushing to within points of a new all-time high, Japan (+1.4%) followed suit as did much of the region (India, Taiwan, New Zealand, Indonesia) but China (-0.6%) and Hong Kong (-0.2%) didn’t play along. Europe, though, is having a positive session with gains ranging from 0.65% (DAX) to 1.3% (CAC) and everything in between. It seems that the NATO spending news continues to support European arms manufacturers and the cooling of tensions in the Middle East has lessened energy concerns. US futures are also bright this morning, up about 0.5% at this hour (7:40).

Finally, bond markets are selling off slightly after a further rally yesterday and yields since the close have risen basically 3bps in both Treasury and European sovereign markets. There is still no indication that any government is going to stop spending, rather more increases are on the horizon, but there is also no indication that central banks are going to stop supporting this action. No central bank is going to allow their nation’s bond market to become unglued, regardless of the theories of what they can do and what they control. Ultimately, they control the entire yield curve.

On the data front, this morning brings Personal Income (exp 0.3%), Personal Spending (0.1%) the PCE data (Core 0.1%, 2.6% Y/Y; Headline 0.1%, 2.3% Y/Y) and at 10:00 Michigan Consumer Sentiment (60.5) and Inflation Expectations (1yr 5.1%, 5yr 4.1%). There are several more Fed speakers, including Governor Cook, a Biden appointee who is a very clear dove, but has not yet agreed that rate cuts make sense. It will be interesting to see what she has to say.

It is a summer Friday toward the end of the month. Unless the data is dramatically different than forecast, I expect that the dollar will continue to slide slowly for now, although I do expect the metals complex to find a bottom and turn. As to equities, apparently there is no reason not to buy them!

Good luck and good weekend

Adf