The clock to the deadline is ticking

And right now, most traders are kicking

All risk to the curb

But they won’t disturb

The hodlers who spend time wound-licking

The market focus right now is on the deadline that President Trump has imposed for Iran to reopen the Strait of Hormuz, which is at 7:45pm EDT this evening. I have read several takes on the likely impact of a destruction of Iran’s power grid, all explaining the consequences would be calamitous for the nation and its people. Within a week or two, the humanitarian crisis would be unprecedented. And that is only on the Iranian side. Almost certainly the Iranians would retaliate and seek to destroy as much Gulf and Israeli infrastructure as possible to inflict the same pain there. Ultimately, I cannot believe anybody really wants to see this happen. Alas, it is out of all of our hands.

We remain extremely fortunate that we live thousands of miles from the action and although there will be economic consequences, those are easier to adapt to then the destruction of your home and nation. Beyond that, I have nothing to offer regarding the situation there and since I discussed the end of last week in my note last evening, let’s see how things are going this morning (spoiler alert, it ain’t pretty!)

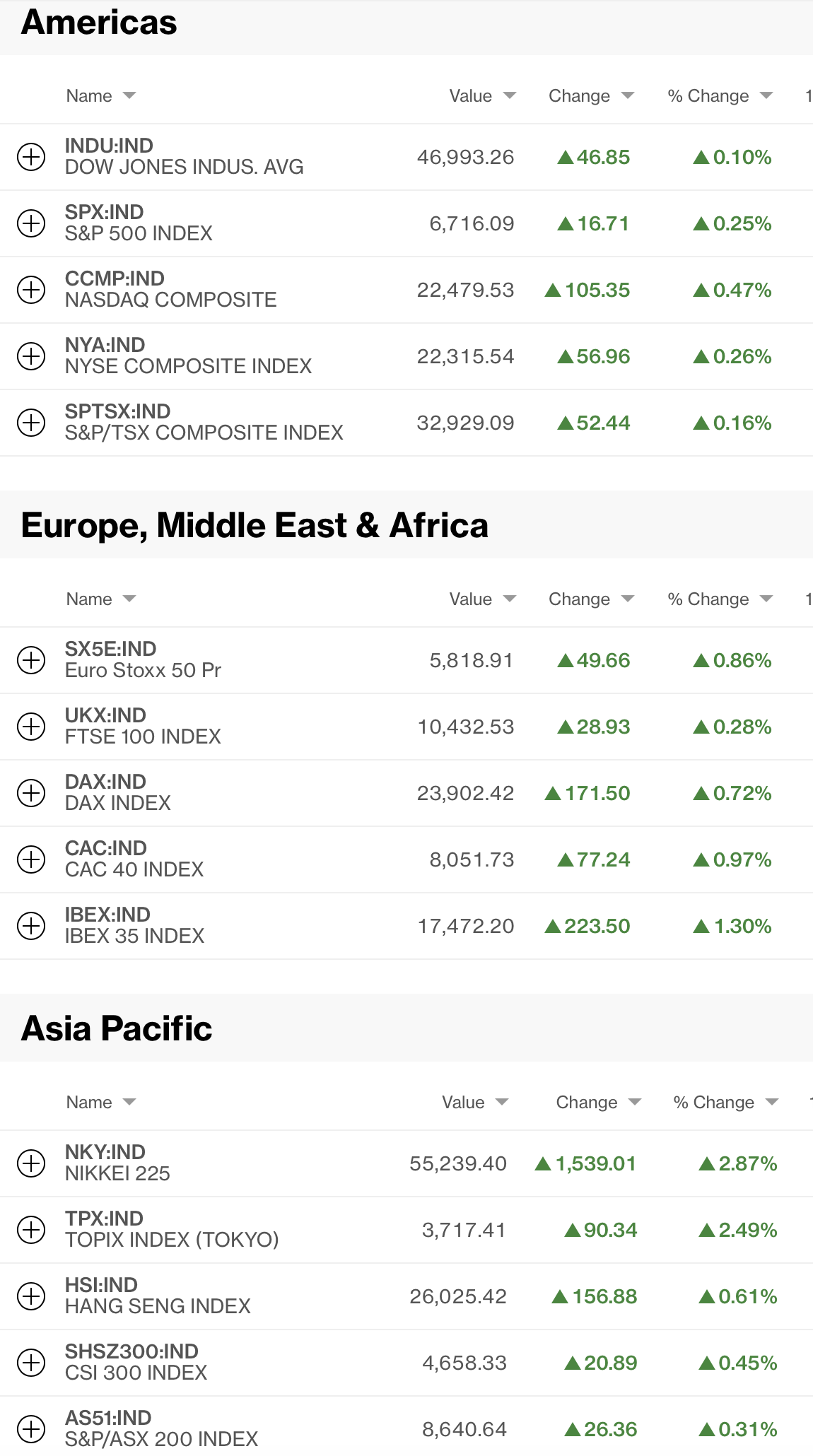

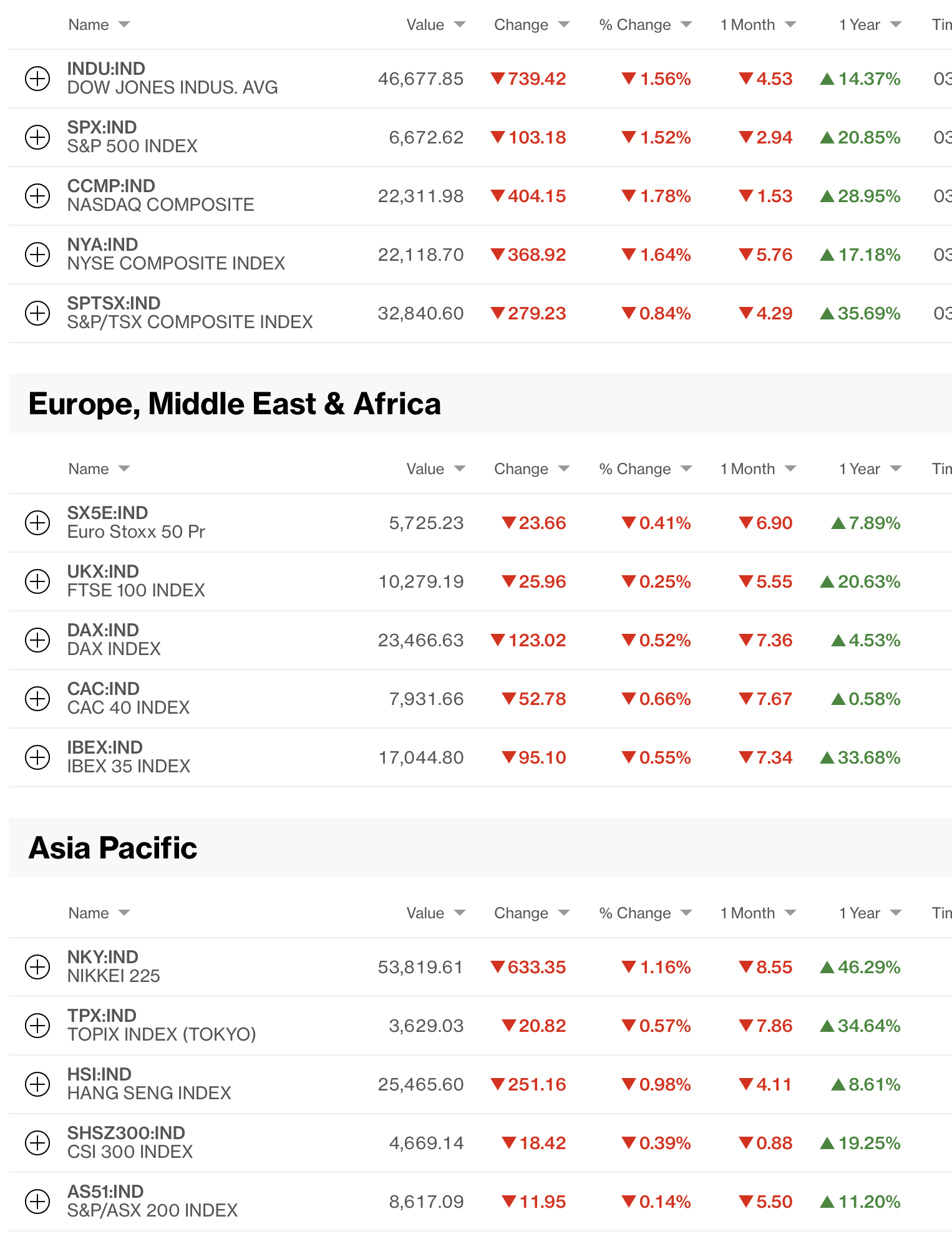

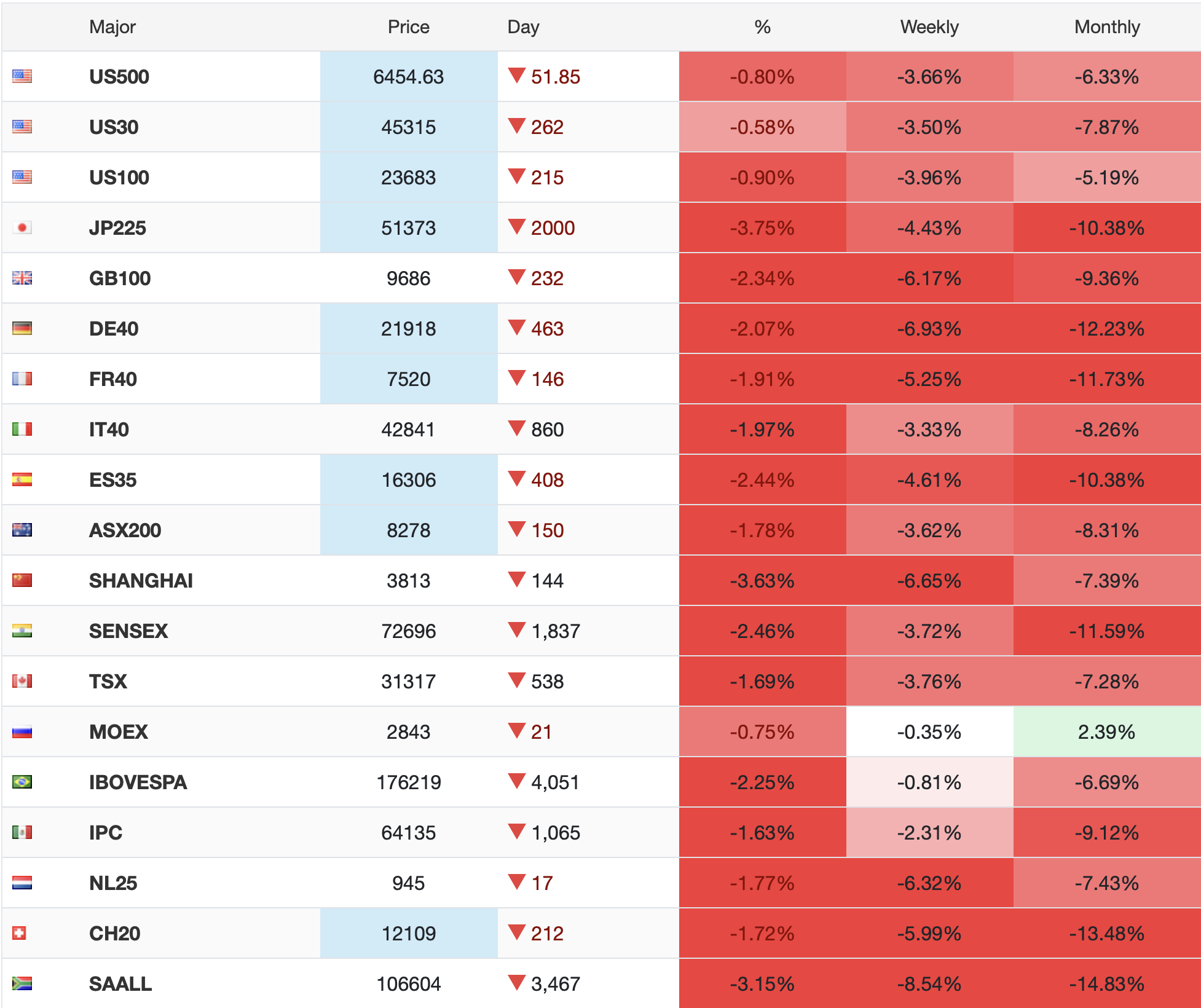

As has been the case for the past several weeks, screens everywhere are red this morning and it is easier to show a screenshot than list them all here.

Source: tradingeconomics.com

This picture was taken of futures markets at 6:55 this morning but you can see that Asian markets and European markets are all meaningfully lower. As has been the case since the beginning of the conflict, the rise in oil prices and its knock-on effects have been the driver. It appears that there are two broad groups of investors right now, the leveraged ones who are being forced out of positions rapidly as every decline brings further margin calls, and the cash investors who are trying to stick it out, at least in the areas they feel will rebound. But the pain is real, at least on a mark-to-market basis, if one is marking to market every day.

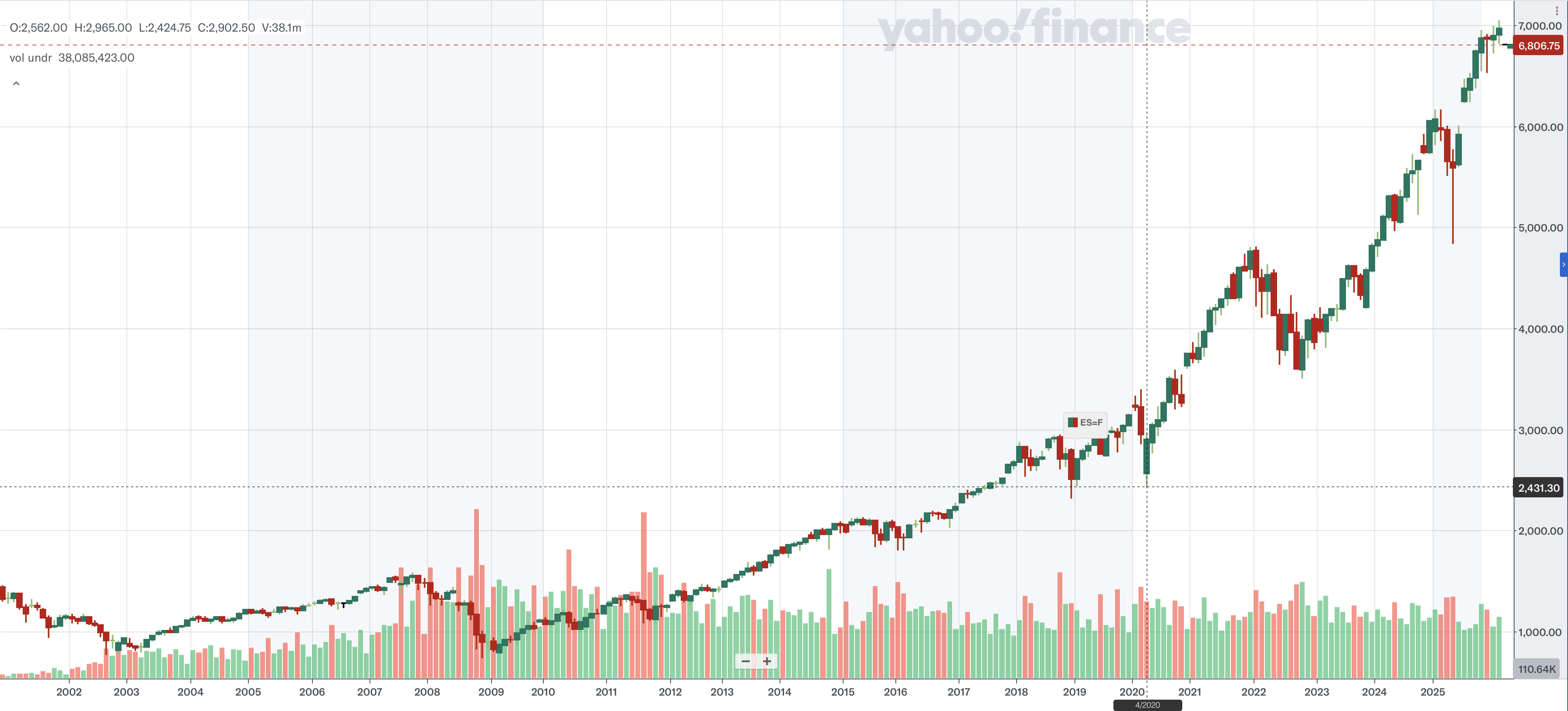

History has shown that declines of this nature tend to offer tremendous buying opportunities for those who have the means to do so. Consider the chart below showing the S&P 500 from the year 2000 on.

Source: finance.yahoo.com

It is easy to see the sharp decline from the GFC, as well as the Covid dip and then 2022, which was a particularly difficult year for both stocks and bonds. But the direction of travel remains up and to the right and this dip will almost certainly be followed by significant gains going forward. Of course, the timing of those gains remains uncertain, but absent a complete collapse of the economy, this seems the most likely outcome. That doesn’t, however, mean it will be a painless trip.

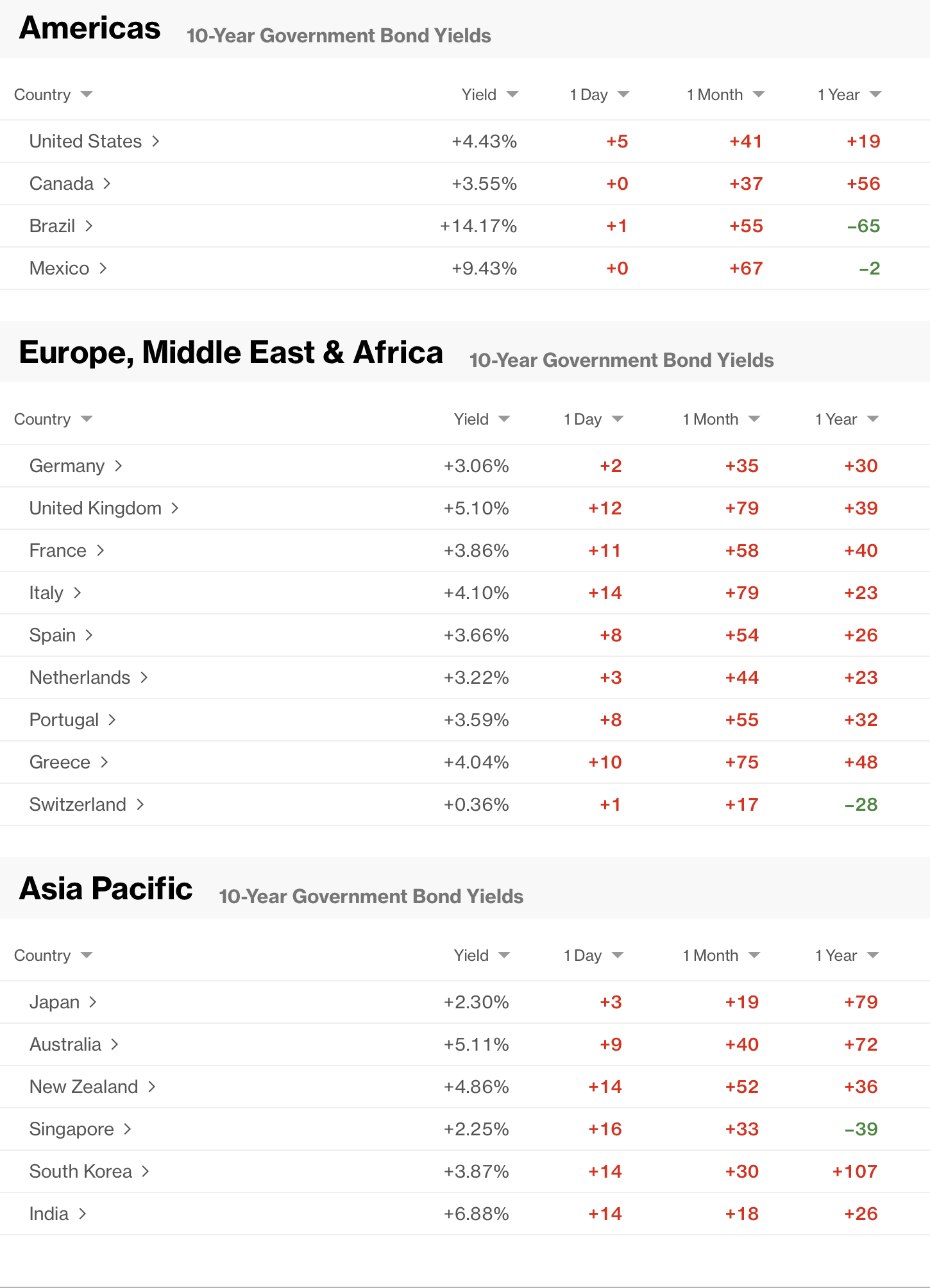

Turning to bonds, yields everywhere are higher as inflation fears remain the feature topic throughout the world. Here, too, a Bloomberg screenshot does all the work for me.

However, I think it is worth stepping back and looking at how bonds have behaved over the past five years. the chart below shows the percentage change in 10-year bond yields in the US and Japan since early 2021. While I am using Treasuries, despite the rise in yields everywhere in Europe, the charts there would be similar.

Source: tradingeconomics.com

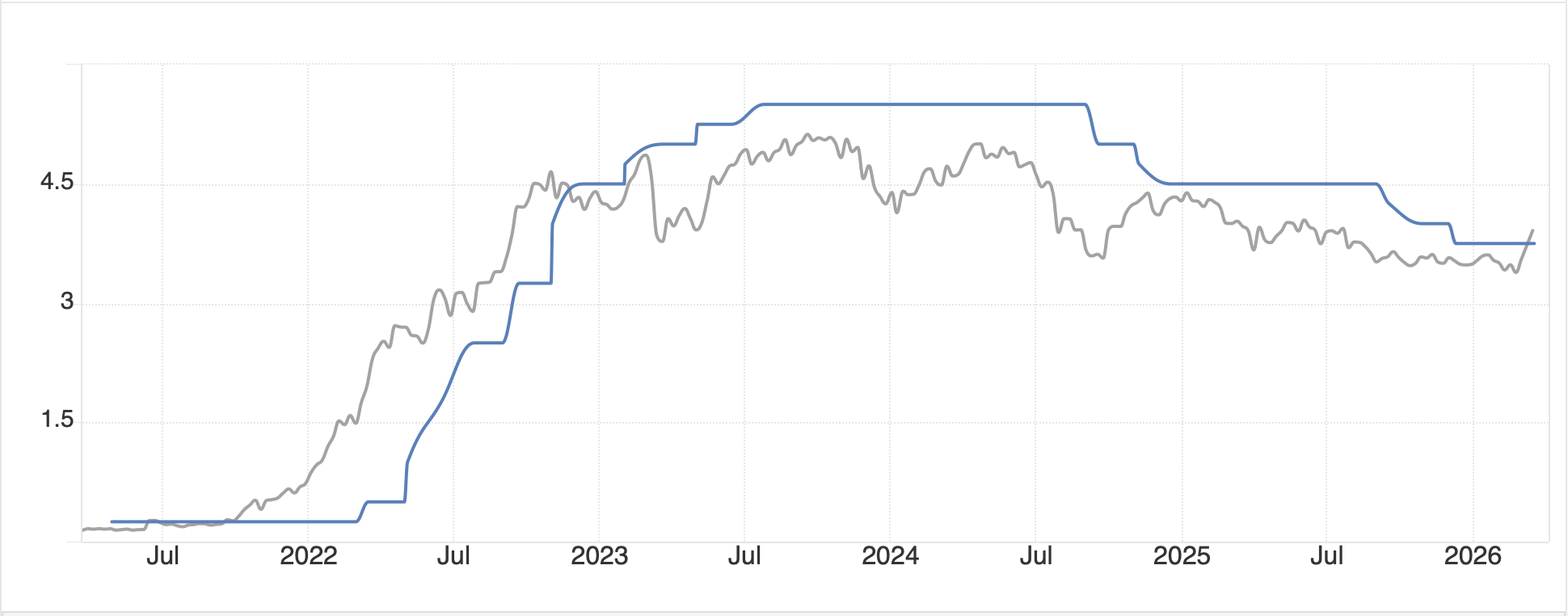

My point is that while there is great angst daily regarding each basis point of movement in yields, US yields have been pretty stable for a long time. Of course, we all know the story of JGB yields, which had been stable at extremely low levels for a decade, and have now moved much higher. The thing is JGB yields moved much higher long before the Iran events, so while at the margin, that is having an impact, there was a strong trend already.

Once again, I believe perspective on markets is important as unless you are a professional trader, the day-to-day can drive you crazy and there is little you can do to change it. Long-term investors need to understand that reality.

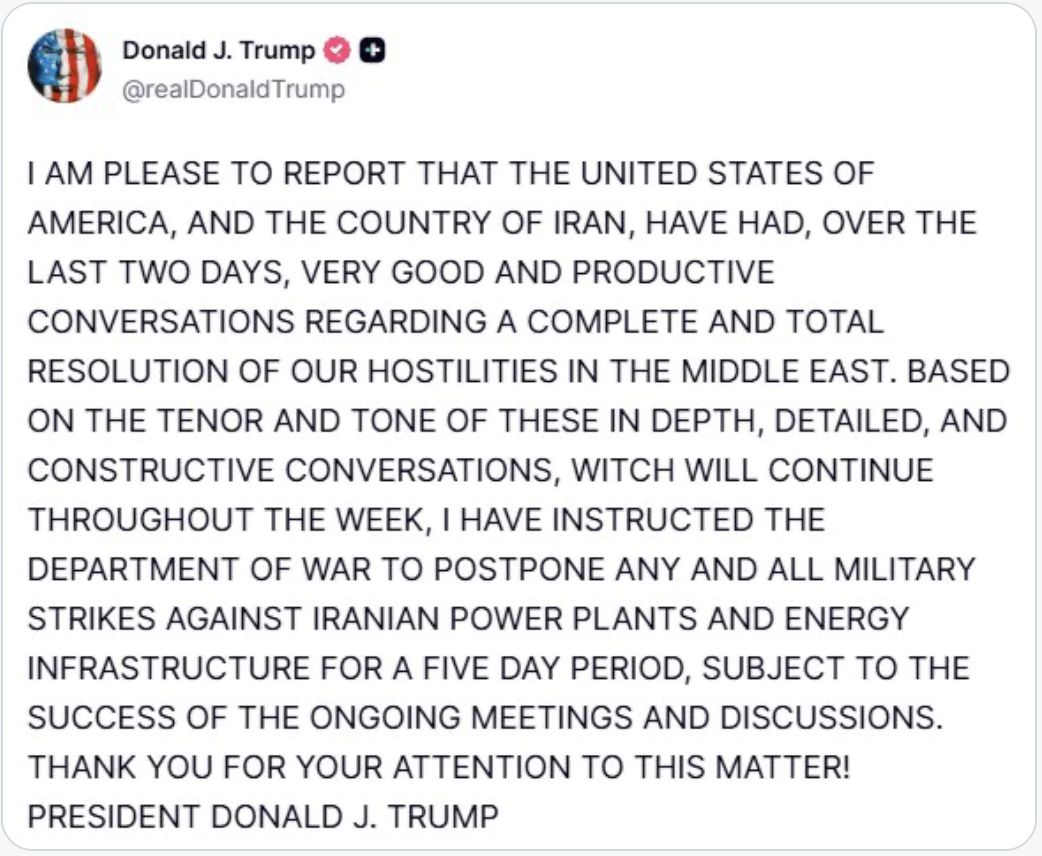

Turning to commodities, I have to wait as things have changed dramatically based on the following post by President Trump.

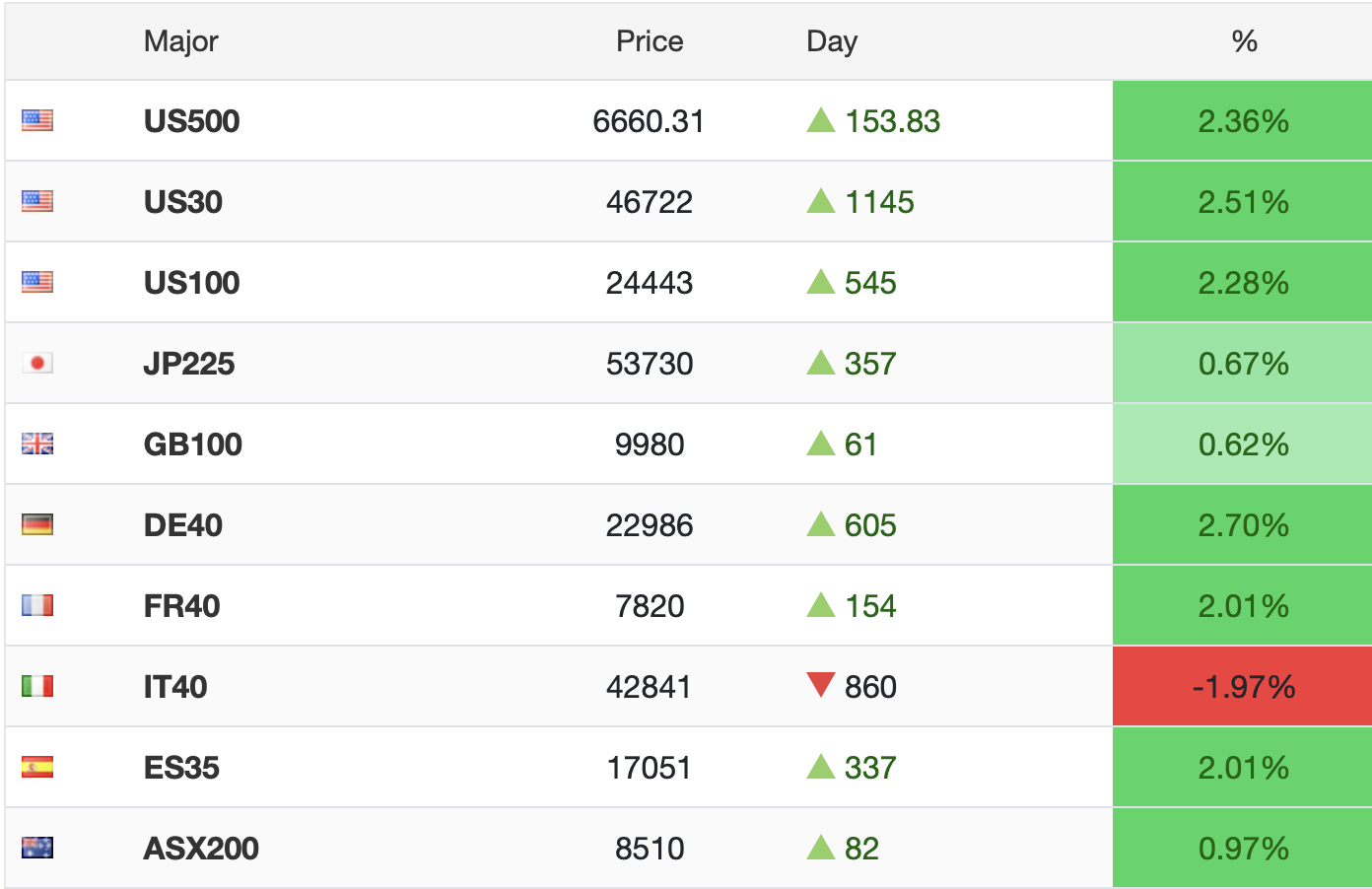

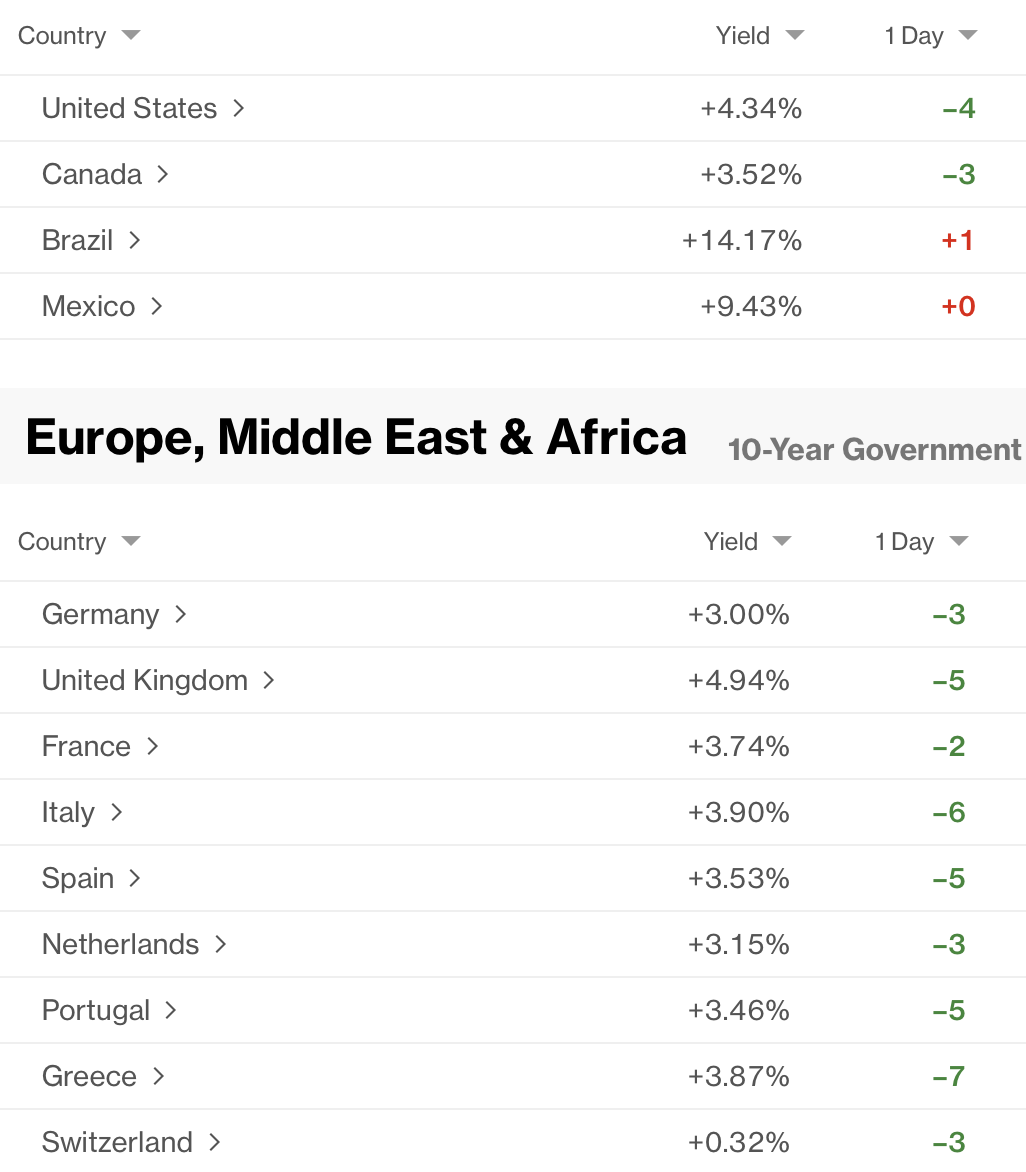

You will not be surprised that the worst-case declines in both stocks and bonds have reversed as per the below screen shot taken at 7:34

Source: tradingeconomics.com

And bonds from Bloomberg:

Back to commodities, below is oil’s response to the Truth Social post, falling sharply from relatively unchanged prior to the comments.

Source: tradingeconomics.com

And while gold is still lower on the day, you can see how much it, too, has adjusted based on the post.

Source: tradingeconomics.com

You won’t be surprised that the dollar, which had been much stronger earlier this morning has reversed course and is slightly lower now.

It is extremely difficult to keep up sometimes and I apologize for the numerous charts, but they truly are worth thousands of words in this situation.

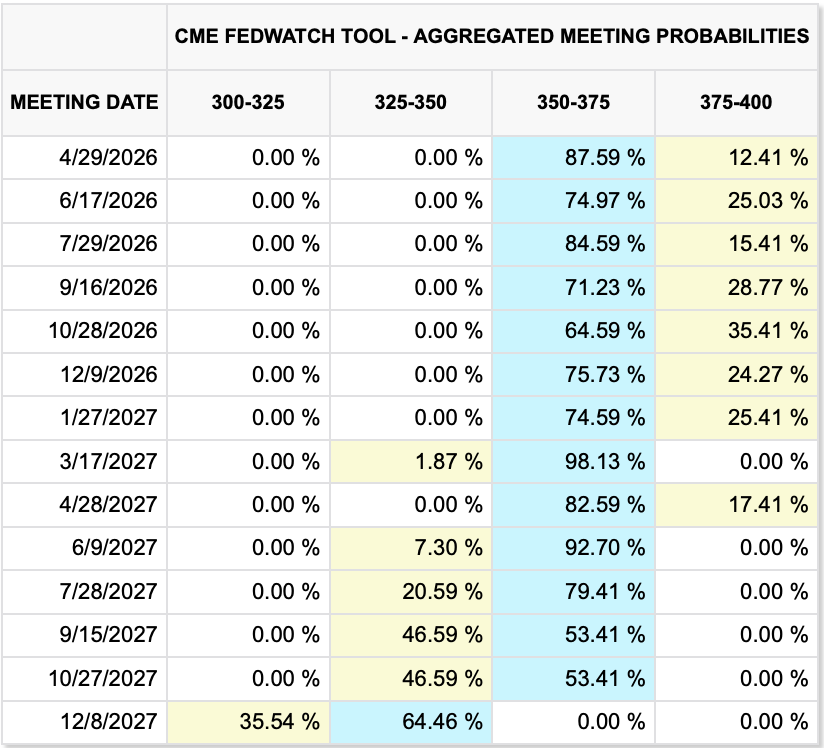

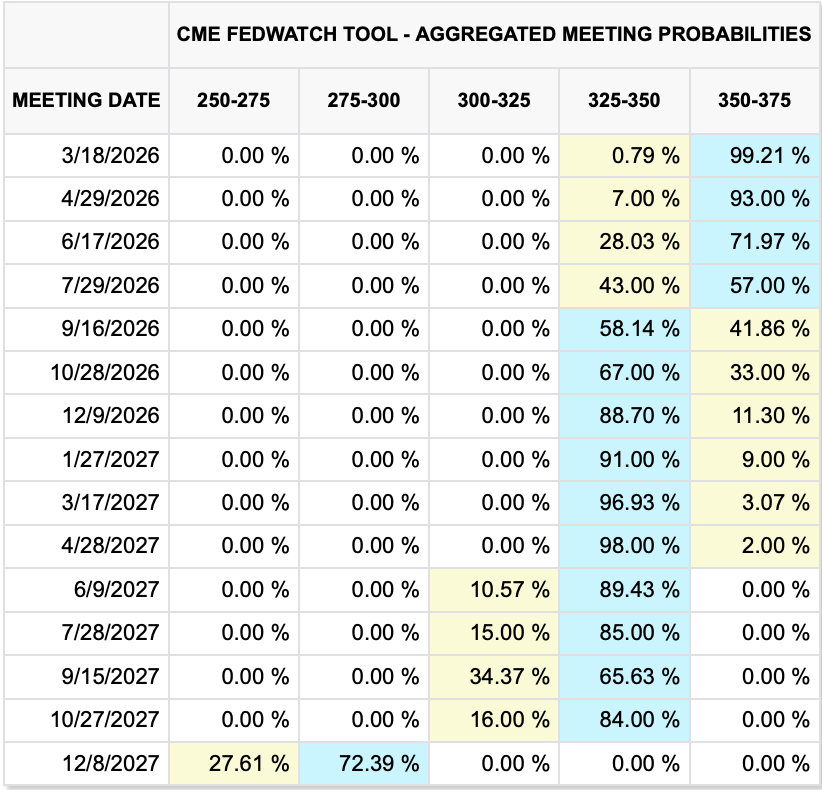

I would talk about data, but I cannot believe that will really matter right now. The growing consensus was that central banks around the world were preparing to tighten policy as oil driven inflation was going to need to be addressed, even if history showed this to be a categorical error. And the first inkling from the Fed funds futures markets is that the probability of a rate hike is being reduced somewhat compared to the end of last week.

Frankly, nobody knows how things are going to evolve from here. Many will say that Trump TACO’d but it is not hard to believe that whatever Iranian leadership remains has looked around and decided they couldn’t take it anymore either.

As I have maintained for a while, play it close to the vest for now, but I expect that there are many value opportunities around, just in tiny bites.

Said Trump, we have had some good talks

And so, we will set back the clocks

On when we attack

Iran’s power stack

As doves take the lead, not the hawks.

Good luck

Adf