The Strait of Hormuz remains closed

And right now, both sides seem disposed

To keep up the fighting

While pundits keep writing

That Trump will soon find himself hosed

Meanwhile, this week central banks meet

And none are expected to treat

The oil price spike

With any rate hike

Though keep eyes on each balance sheet

Nothing seems to have changed dramatically in Iran with US bombing attacks continuing and Iranian missile and drone attacks continuing. It remains a daunting challenge to discern reality on the ground there as every news source spins any information to their political viewpoint, and I, for one, have been unable to pull much signal from the noise. This is truly the fog of war.

With that in mind, it does appear that different markets are taking very different cues from the situation, with some (oil and the dollar) continuing to hew to a strong risk-off viewpoint while others, equities and bonds, remain unconvinced that the world is about to end.

As such, perhaps we should take a few moments to consider the fact that this week, we are going to see interest rate decisions from every major Western central bank in the following order: RBA, BoC, FOMC, ECB, BOE, BOJ, SNB, starting tonight and concluding on Thursday.

Of all these banks, only the RBA is expected to move, raising its base rate by 25bps to 4.10%, although that was baked in prior to the events in Iran beginning. I would contend this is not a response to the oil price. In fact, one must assume that central bankers are aware of the history of responses to exogenous price shocks, like an oil spike, and that any attempt to offset the inflationary consequences in the past has led to major economic pain. It is not hard to understand that a sharp rise in oil prices, and the concurrent rise in gasoline and diesel, acts as a “tax” on the economy which tends to reduce economic activity. Hiking rates into that scenario would very likely result, and historically has resulted, in a recession in short order.

Remember, the reason central banks, in general, look to core inflation, is because they know they cannot impact the prices of food or energy via interest rate policy. While the ultimate impact of this oil price spike will only be known many months from now, if the conflict ends in the next several weeks, it is likely that any structural price issues will be avoided. Of course, we have no idea how long things will last right now, so as investors and hedgers, reduced exposure to financial markets is likely the best advice for almost everyone.

Which means, it’s time to look at the markets and see what they are telling us. After Friday’s soft close in the US, Asia saw a mix of outcomes. Tokyo (-0.1%) did little overall, and we saw some weakness in Australia (-0.4%), New Zealand (-0.3%) and the Philippines (-0.9%) with Indonesia (-1.6%) the regional laggard. However, there were numerous markets who ignored the oil price and rallied including Hong Kong (+1.5%), Korea (+1.1%), India (+1.3%) and Singapore (+0.6%) with mainland China essentially unchanged in the session. China released a raft of data showing that the economy there continues to have property troubles (House Prices -3.2%), but the rest of things were largely in line with their reduced GDP expectations excepting Unemployment, which rose to 5.3%.

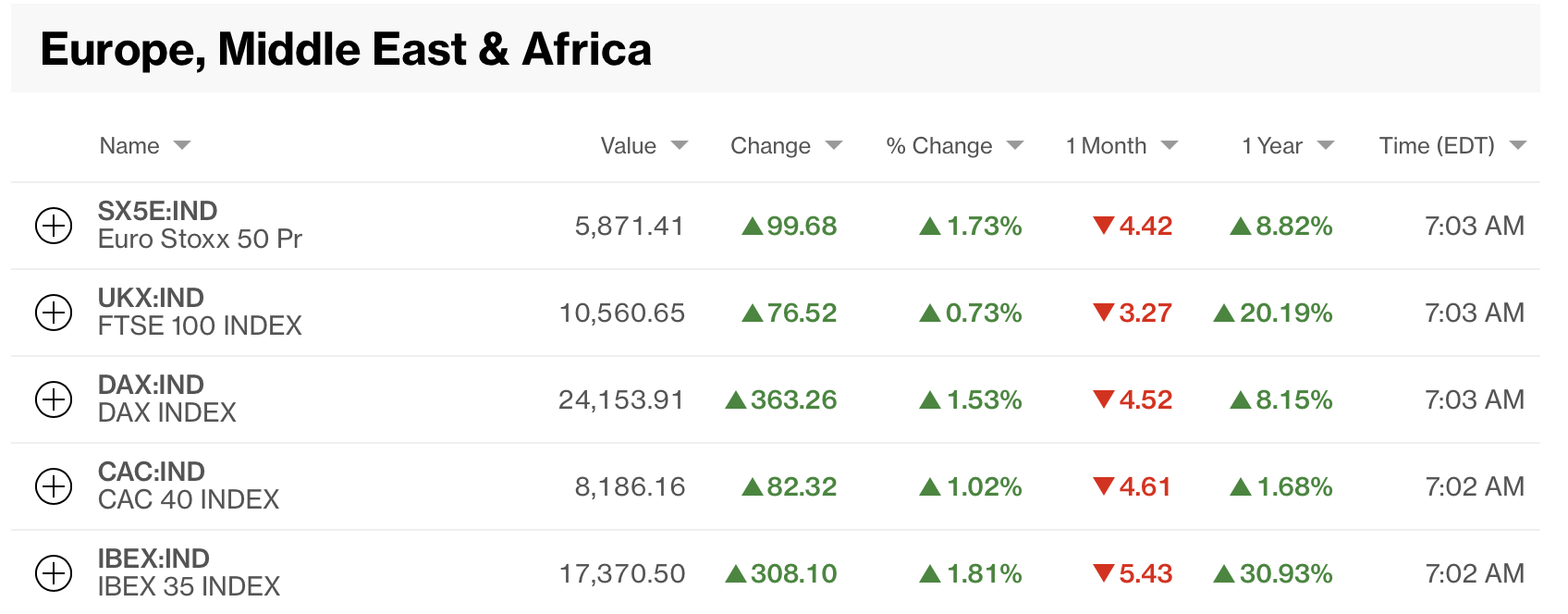

Europe, too, is seeing a mixed picture this morning with some gainers (Germany, UK) and some laggards (Spain, France, Italy) although none of the movement is very significant, < 0.3% in every case. US futures at this hour (7:10) are all pointing nicely higher, in fact, by 0.5% to 0.8%.

My point is that despite fears of the death of the equity rally, as I type this morning, the S&P 500 is just 4.5% from its all-time high made at the end of January. I am no technician, but the chart below shows both the long-term direction and the 52-week moving average, and the current price is well above both of these indicators. This is not to say the market cannot decline from here, just that the broader trend remains higher. It does not feel very apocalyptic to me at this point.

Source: tradingeconomics.com

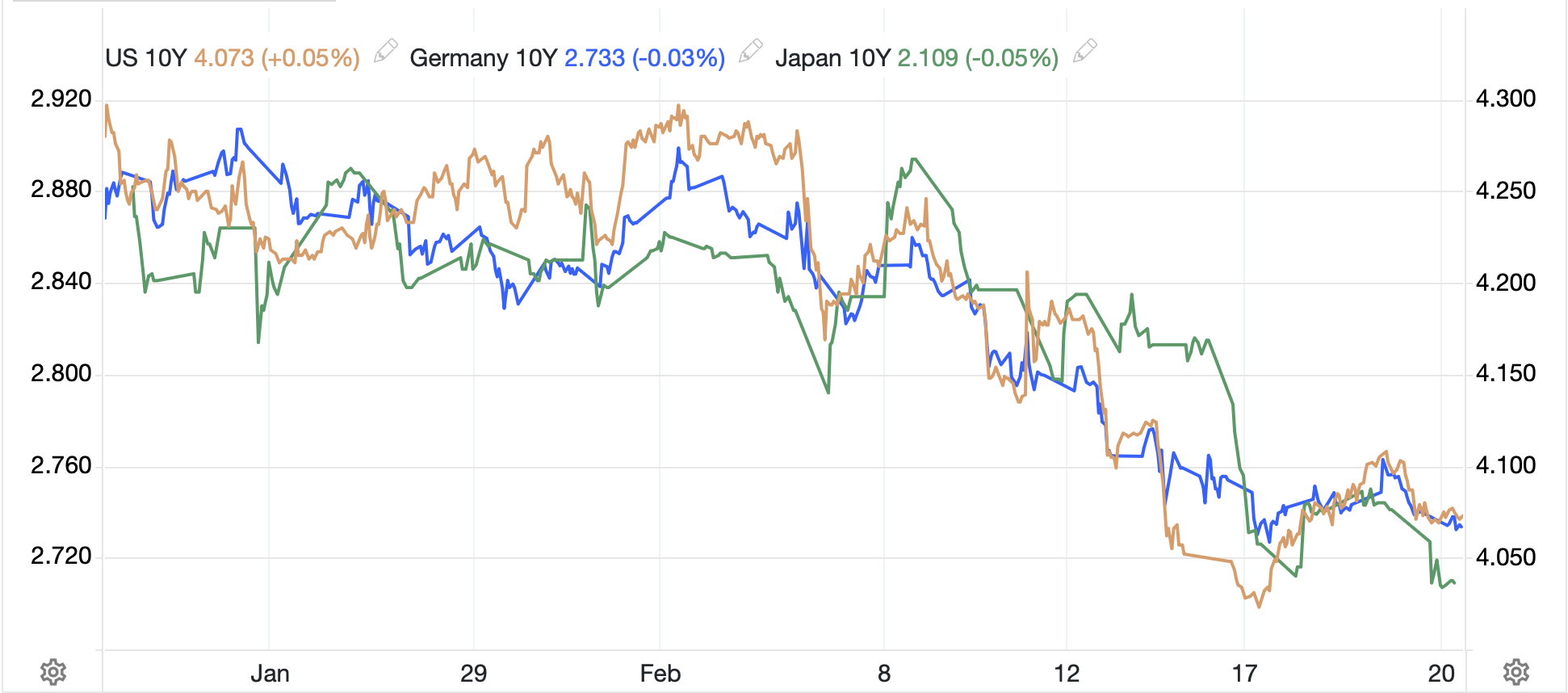

Turning to the bond market, yields are lower across the board this morning with Treasuries (-3bps) backing off the highest levels seen last week, and currently at 4.25%. While that rate is clearly above the lows, it hardly smacks of panic nor of a bond-buying strike. Of course, historically, when uncertainty rises, Treasuries have been a primary safe haven, and that has not been the case this time either. It appears to me that investors are caught between fears of rising inflation and fears of economic contraction so don’t know whether they want to hold their bonds or sell them. As to European sovereigns, all are in fine fettle this morning with yields slipping between -2bps (Germany) and -6bps (UK). Again, this does not smack of inflation fears today.

Which takes us to the key driver of almost everything, oil. Right now, WTI is trading lower by -1.5% and is back below the $100/bbl level. While, of course, the recent trend is higher, that is entirely on the back of the Iran situation. If/when that is resolved, I expect the price to retreat sharply right away, although probably not to its prewar levels for another few months. But if it traded back to $70/bbl, that would remove virtually all the inflation talk and investors would need to look elsewhere for cues.

Source: tradingeconomics.com

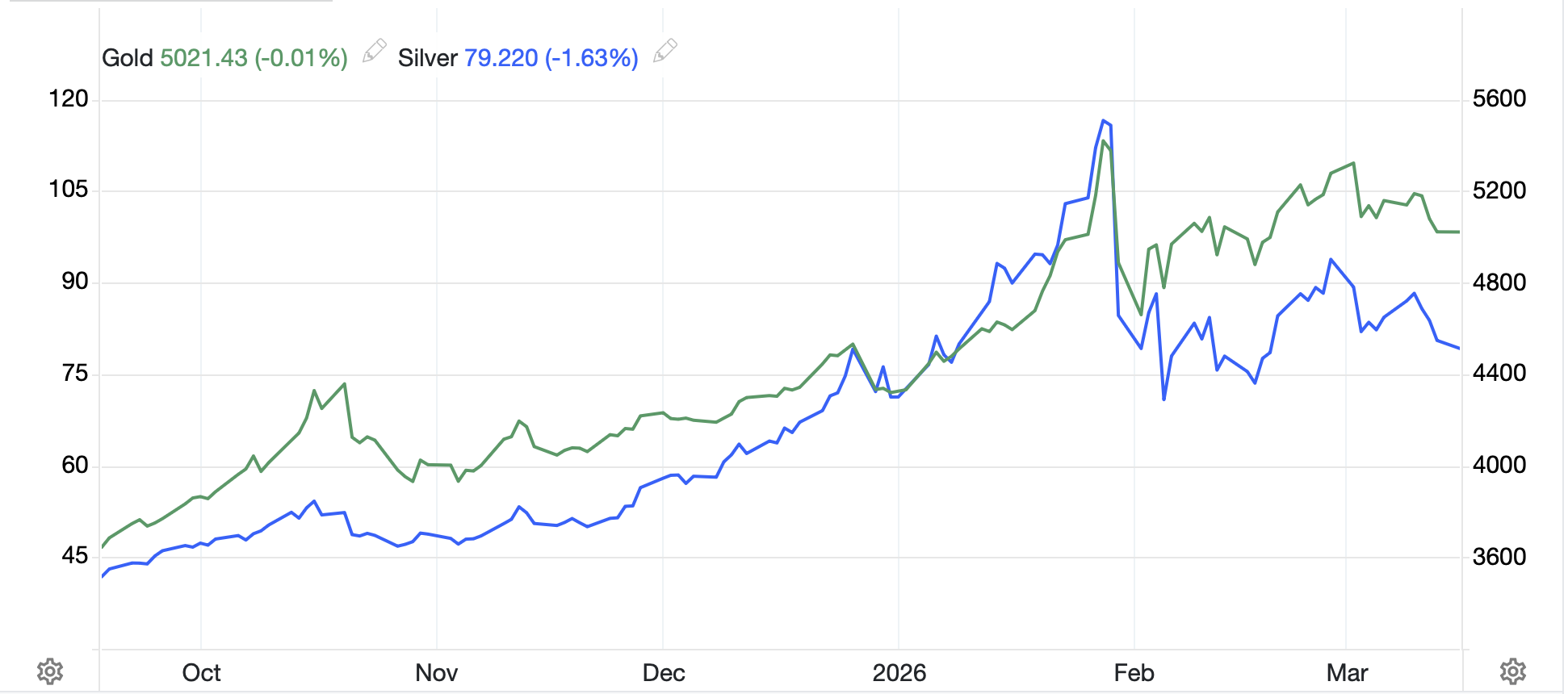

In the metals markets, gold (0.0%) is trading just above $5000/oz and silver (-1.6%) just below $80/oz, and neither has responded as would have been expected prior to the Iran conflict. Recall, both peaked at the end of January, just before the Kevin Warsh as Fed chair announcement, and as you can see below, both have largely gone nowhere, albeit with a lot of daily volatility attached to that lack of movement.

Source: tradingeconomics.com

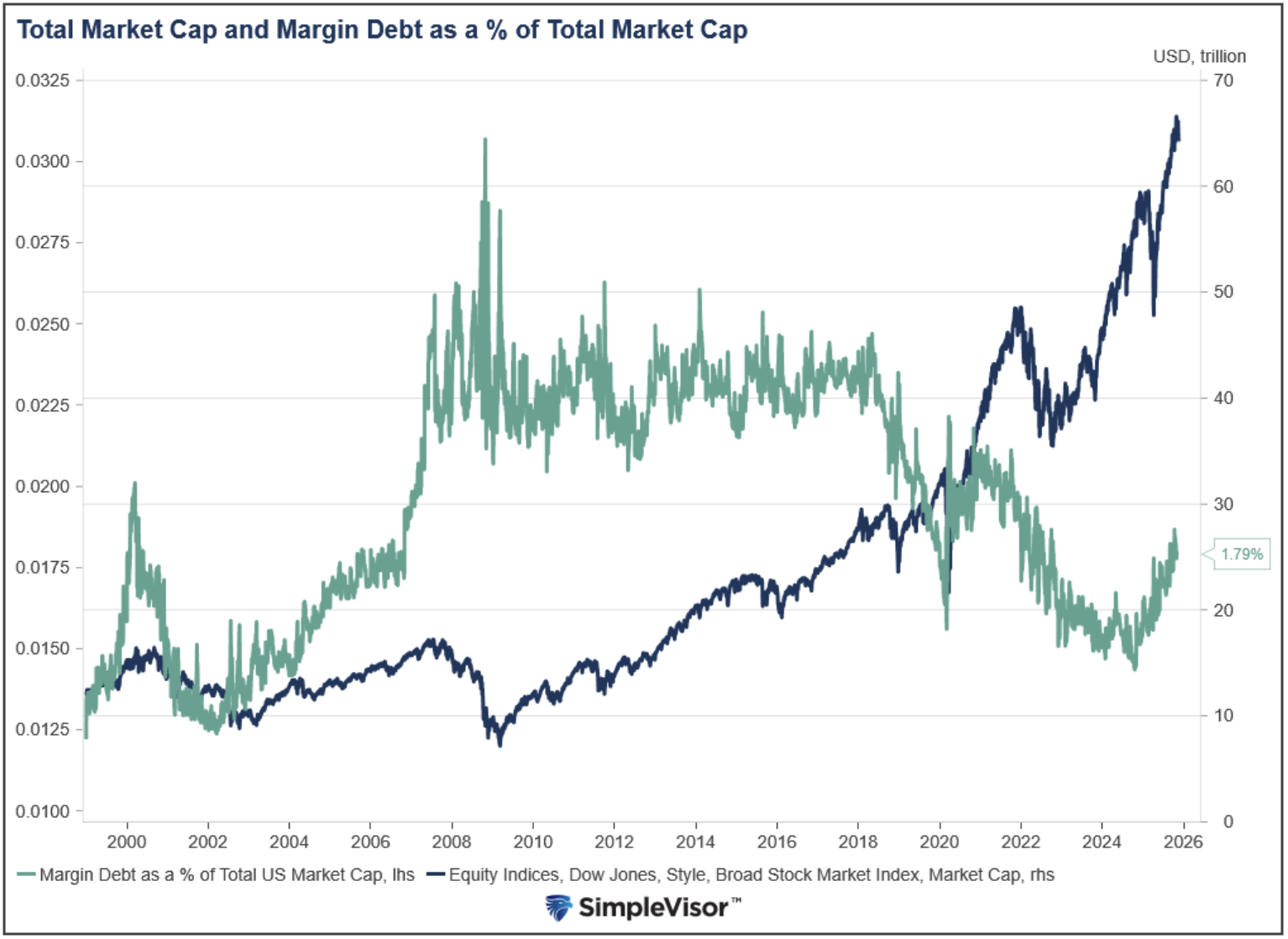

It makes no sense to me that after a 5000-year history as the ultimate monetary safe haven, gold has suddenly lost its allure in that capacity. As such, I continue to believe that the lack of follow-through higher during this war is a result of leveraged investors needing to raise cash to cover margin calls and given the gains that were available in their gold positions, and the liquidity in the market, gold was the most convenient way to manage positions. Remember, leverage has been a key part of the story of recent market moves, with margin debt at all-time highs, > $1.1 trillion, although it represents just 1.9% of outstanding market capitalization, less than the all-time high percentages seen ahead of the financial crisis.

Source: investing.com

Nothing has changed my take on the underlying demand for precious metals at this point.

Finally, the dollar is a bit softer this morning but has retained most of its gains from this move. However, as a descriptor of today’s lack of fear, the dollar’s pull back is as clear a signal as any. So, the euro (+0.5%) is rebounding away from the 1.1400 level seen Friday, while the yen (+0.4%) is backing away from the 160 level. AUD (+1.0%) seems like it is preparing for this evenings’ RBA rate hike, but the dollar is lower across the board after a solid run ever since the Warsh announcement. Looking at the DXY (-0.35%) below, you can see that today’s move is modest in the scheme of things, and we will need to see a lot more dollar selling before this trend changes.

Source: tradingeconomics.com

EMG currencies are having a very strong day, almost like the war is over. CZK (+1.8%), HUF (+1.7%), PLN (+1.1%), ZAR (+1.0%), MXN (+0.9%) and KRW (+0.9%) are representative of today’s price action. I’m wondering if I missed the news that the war ended!

On to the data this week, which in addition to all those central bank meetings includes a large array of generally secondary data, although PPI is part of the mix.

| Today | Empire State Manufacturing | 3.2 |

| IP | 0.1% | |

| Capacity Utilization | 76.2% | |

| Wednesday | PPI | 0.3% (2.9% Y/Y) |

| -ex Food & Energy | 0.3% (3.7% Y/Y) | |

| Factory Orders | 0.2% | |

| FOMC Rate Decision | Unchanged | |

| Thursday | Initial Claims | 215K |

| Continuing Claims | 1855K | |

| Philly Fed | 9.0 | |

| New Home Sales | 720K |

Source: tradingeconomics.com

I imagine that folks will look at the PPI data to see if they can glean anything about inflation going forward, but it, too, is a February number, so will not have anything from the war. It will also be interesting to see what Chairman Powell says in his press conference, but I can’t imagine much new information will flow there either. After all, with the war, they are kind of stuck for now.

So, it continues to come down to market interpretations of commentary regarding the war. As I said, this morning, investors don’t seem that worried things will get worse. The Greed and Fear index is at 22, not great, but we have seen worse just recently. Again, lighter positions are the way to go in my view.

Good luck

Adf