The State of the Union Address

Was, as is Trump’s wont, to excess

He touted his claims

And handed out blames

While focusing on his success

The market responded, it seems

Like Trump answered all of its dreams

Stocks round the world rose

Which shows, I suppose

The world does approve of his schemes

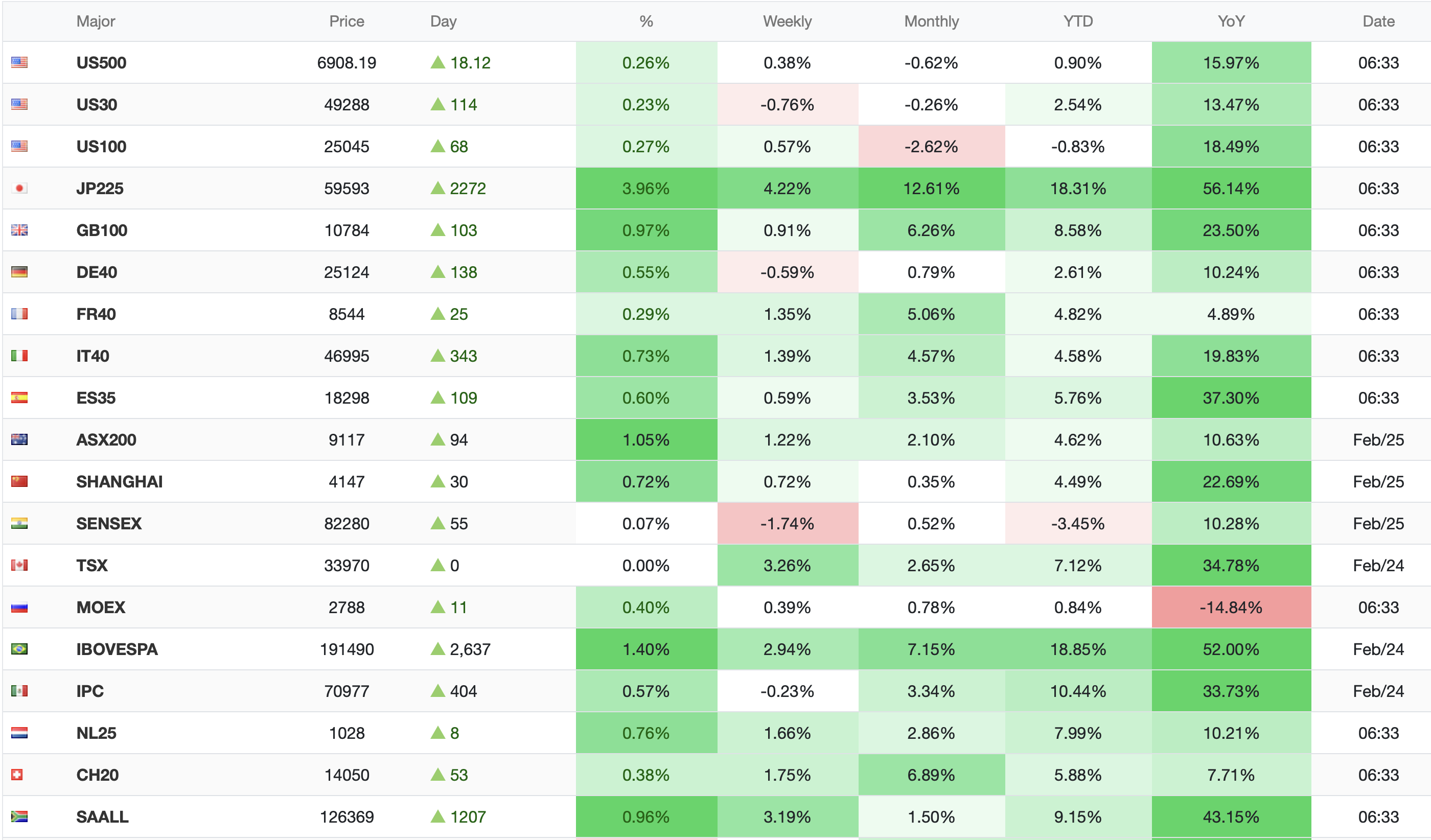

As I look at my screen this morning, literally every major equity market is higher, as per the below screenshot, as are US futures.

Source: tradingeconomics.com

In fact, if you ignore Russia, which hasn’t really been relevant since the Ukraine invasion-imposed sanctions, every market is higher over the last year, and US markets are the true laggards as seen by their monthly performance. But you cannot look at this picture and determine that anything President Trump said last night was negative for the global economy. I guess it’s full speed ahead now.

In true Trumpian fashion, the president remains incredibly optimistic about the future for the US and the Western world and perhaps that is what is reflected here this morning. However, there were precious few new initiatives announced so it is unclear to me that this is going to be a topic of discussion in the financial markets going forward, although you can be sure that the political narrative is going to be very active.

So, let’s move on to things that matter for markets.

Is she hawk or dove?

Takaichi hates China,

Not easy money

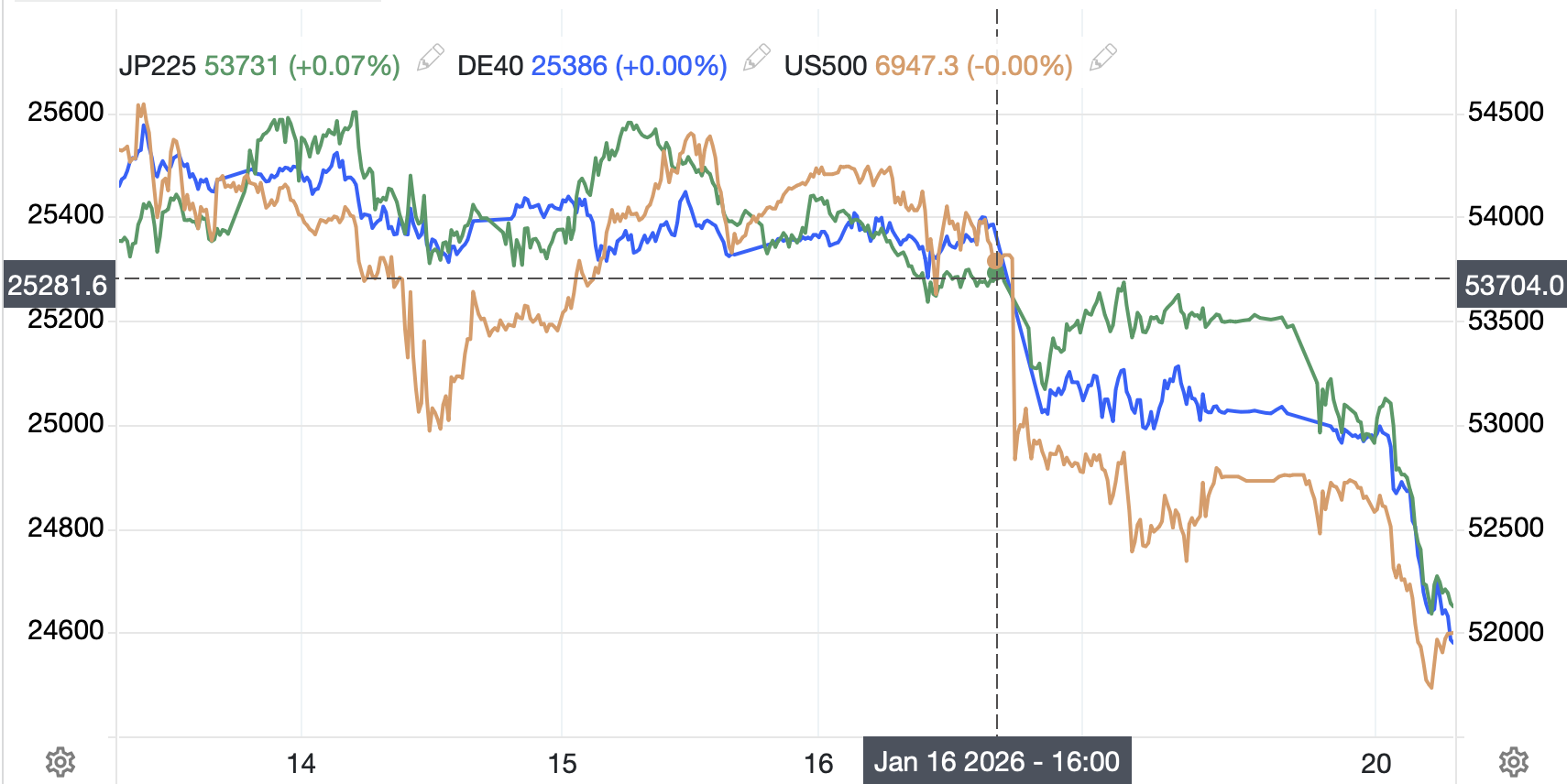

As you can see in the above table, Japan’s Nikkei 225 rose sharply, nearly 4%, but that had nothing to do with the SOTU. Rather, her administration named two new BOJ governors (it was simply time to rotate some) and both were seen as quite dovish. In fact, one, Toichiro Asada, is known for his belief in the benefits of MMT (you remember the magical money tree idea that governments that print their own currency don’t need to worry about overborrowing). The upshot is that while Japanese stocks raced to yet more new highs, as per the below chart, JGB yields reversed their recent declines and rose (10yr +5bps, 30yr +10bps) and the yen (-0.6%) continued its recent slide, although remains well above (dollar below) the 160.00 level, which many see as the BOJ’s line in the sand regarding intervention.

Source: tradingeconomics.com

But other than this story, it is much harder to find things that have been market drivers. To my eye, we continue to see market participants laying back in most places as they are still recuperating from the raucous first six weeks of the year.

So, let’s go to the tape. We’ve already seen the equity performance around the world, with the narratives forming that the US tariff situation is now a reduced stress on global trade as they have been reduced to 10% globally. As well, there have been an increasing number of rebuttals to the AI piece I mentioned on Monday, with this one, I think, the most succinct takedown of the idea that AI is going to eat the world and drive us into a recession with no jobs left for people. As such, Monday’s narrative of all stocks being worthless has changed. Elsewhere, the tariff story and tech rally have been the key discussion points across markets.

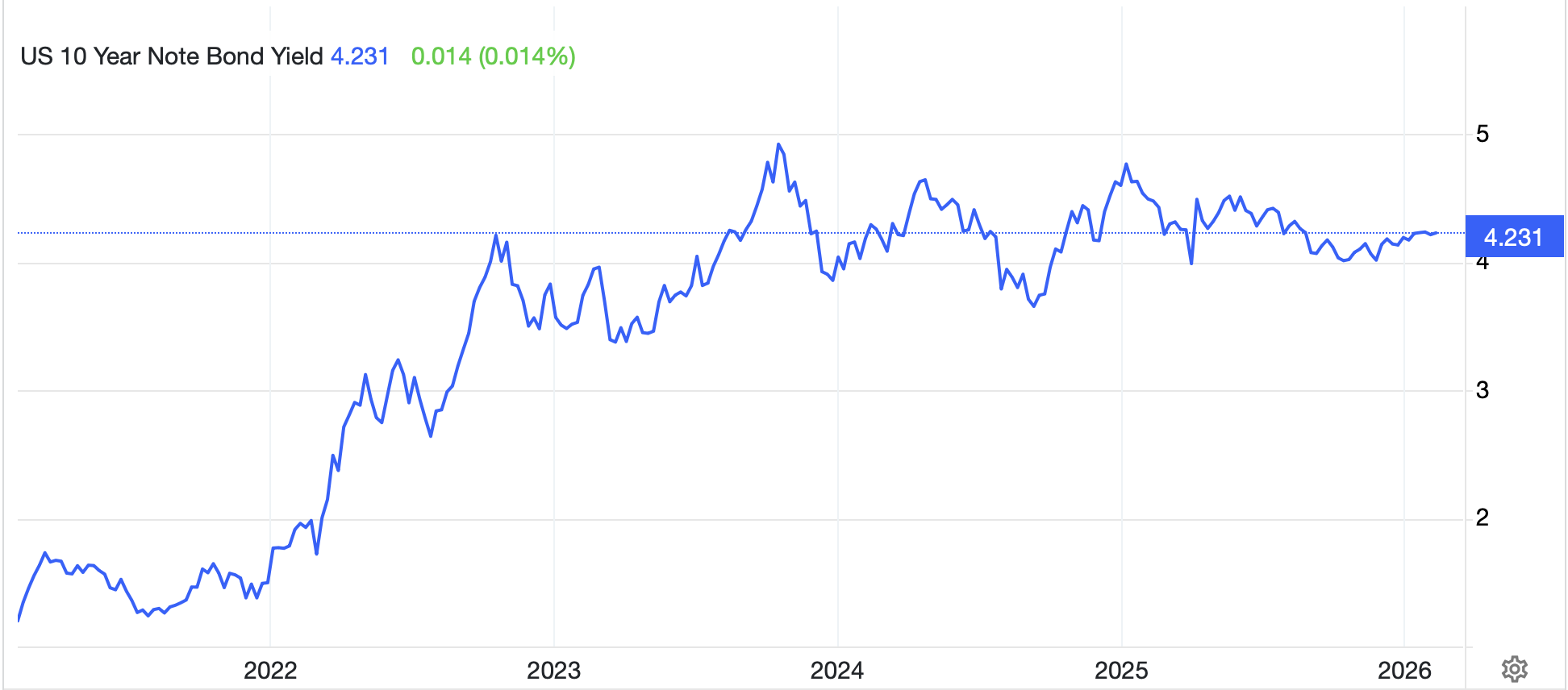

In the bond market, yields are a touch higher with Treasuries (+2bps) edging up on what seems like ordinary trading. The short-term trend here is lower yields, as per the chart below, but we know that nothing moves in a straight line.

Source: tradingeconomics.com

As to European sovereign yields, they, too, are mostly a few ticks higher this morning although, this also appears to be simple trading activity rather than a new narrative. It is interesting that there are more stories today about ECB President Lagarde stepping down early, which is diametrically opposed to what she said when asked the question recently. As I said before, I think she steps down and is going to run for President of France.

The commodity markets continue to be the place with the most price action and this morning is a continuation of that recent trend. Gold (+0.9%), silver (+3.7%) and platinum (+5.5%) are all continuing their rebound from the extreme declines seen back on January 29th.

Source: tradingeconomics.com

I do not have any inside track as to the driver of those moves, but I continue to read and hear about significant intervention designed to burst those bubbles (and they were clearly bubbles) and allow key institutions to cover short positions at better prices. The problem with these stories is that we have heard for years about the manipulation of the prices of both gold and silver by large banks, and the purveyors of those stories have neither great reputations nor track records, so it is always a tough sell in my mind. There is no question that when markets go parabolic, as the precious metals did through January, the reversals have always been dramatic. However, I cannot speculate on the driver as often times, there doesn’t need to be one. This cartoon from Kaltoons demonstrates it perfectly.

Turning to oil (+0.8%), Iran remains a key narrative and continues to support the front month pricing. However, it appears that several futures spreads are falling sharply, indicating a potential glut in physical supplies has developed, at least for now. As I look at the front contracts in the futures curve, we are still in backwardation, which implies a shortage, although I suppose that is the Iran effect.

Source: barchart.com

I understand the short-term concerns here regarding potential military escalation there, but nothing has changed my view that the long-term energy situation is one of abundance and maintaining much higher oil prices will be very difficult for the long-term. After all, look at Venezuela, which has already increased production back above 1mm barrels per day with contracts being signed for more activity. Too, Argentina’s Vaca Muerta shale production is at new record levels, also ~1 mmm bpd and we continue to see growth offshore Brazil and Guyana. Longer term, there is plenty around, I think.

Finally, the dollar is mixed this morning as the yen’s weakness is being offset by modest strength in the euro (+0.1%) and pound (+0.2%). However, the big movers today are KRW (+0.9%) which has benefitted from inward equity flows and hopes for tariff relief, as well as ZAR (+0.5%) on the back of the precious metals rally and CLP (+0.4%) on copper’s strength. Remember, the US is not overly concerned about USD weakness in the FX markets as it suits the administration’s goals of reducing the trade deficit and encouraging onshoring of production. But even with that, looking at the DXY, it is just below 98.00 and remains right in the middle of its trading range for the past 9 months.

Source: tradingeconomics.com

There is no major data out this morning with only the EIA oil inventories where a very modest build is anticipated.

Big picture, I don’t think anything has changed. Fiat currencies continue to lose value relative to ‘stuff’. Equity markets continue to benefit from the global ‘run it hot’ policy and there is no clarity regarding the outbreak of a war in Iran. With this in mind, it is hard to see a large move in the dollar in the near future.

Good luck

Adf