This month has seen traders dismiss

The idea that risk led to bliss

Stocks worldwide have fallen

And those who were all in

With leverage now face the abyss

But it’s not just war in Iran

That’s scrambled most everyone’s plan

The data, as well

Are heading to hell

With no central banking wise man

As I didn’t write on Friday, and it seems some things happened while I was away, I thought I might offer my views of where things stand as we enter the new week.

🤯🤯 😱😱 🤮🤮

I think that sums it up nicely.

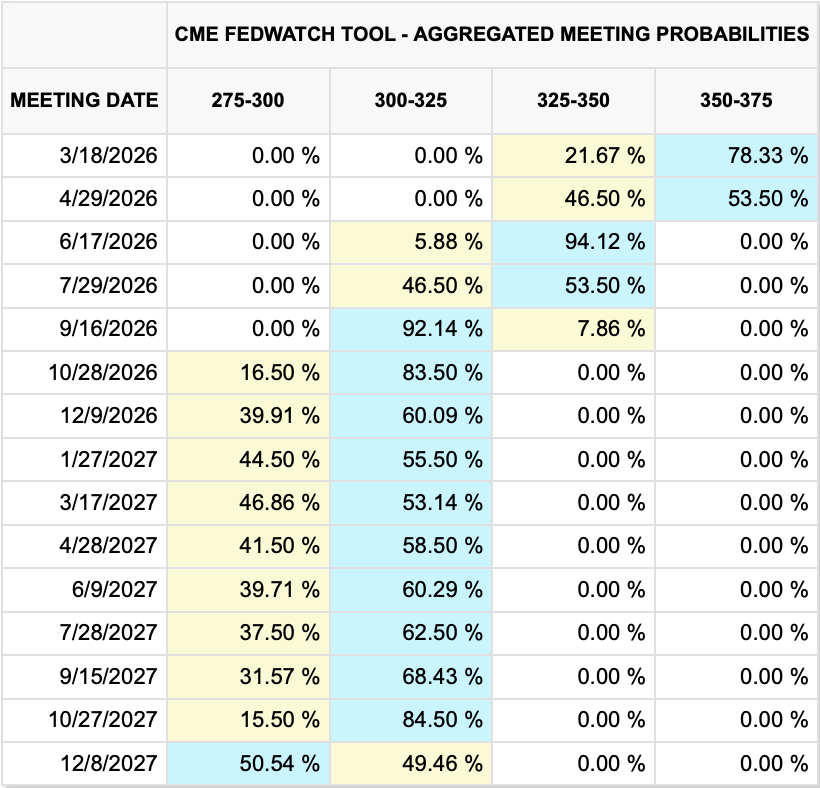

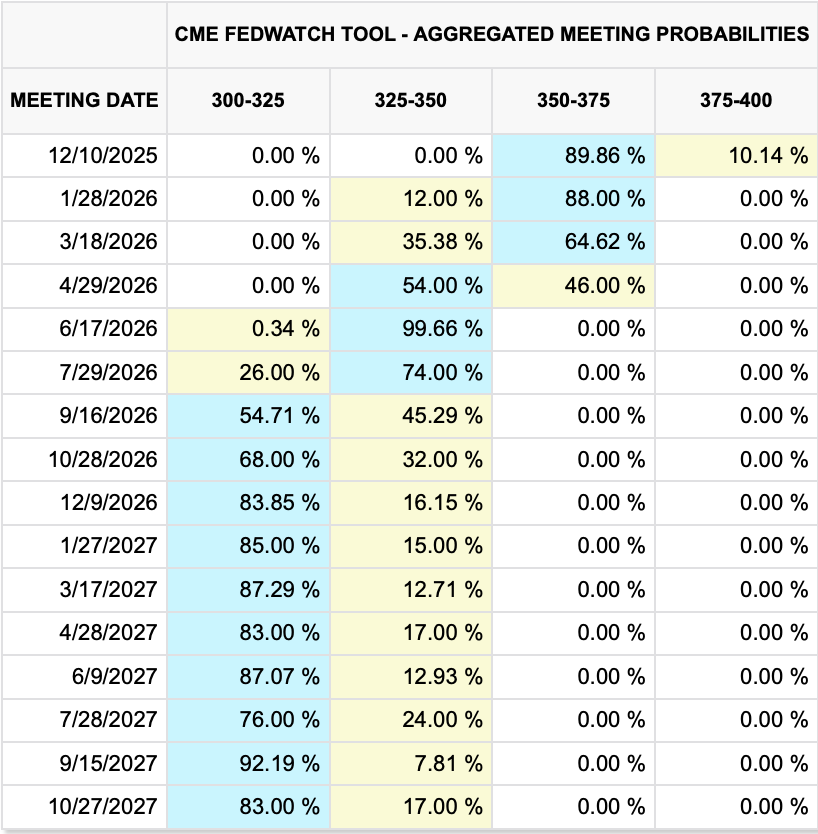

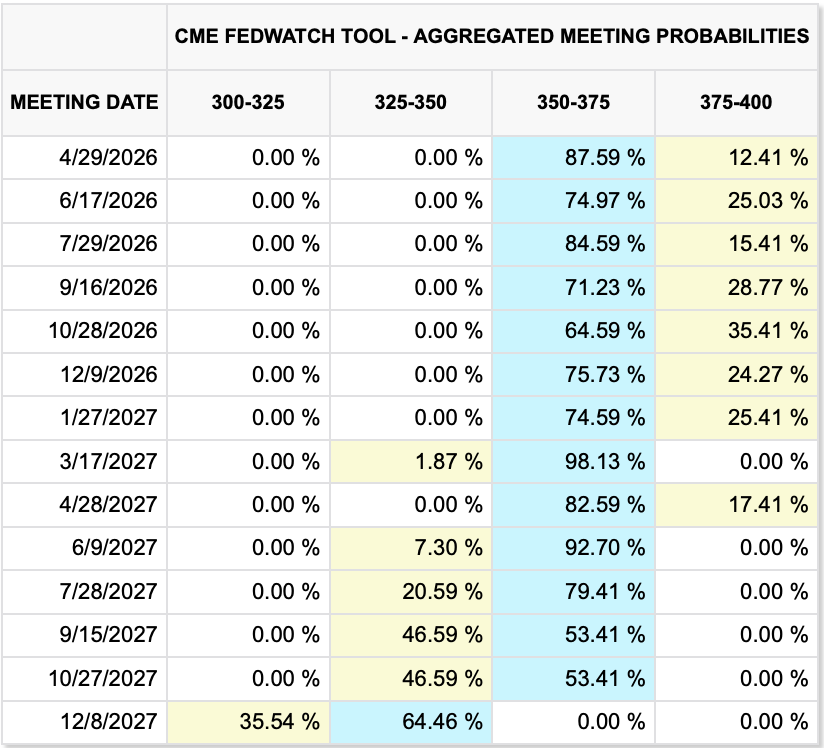

Recapping the end of last week quickly, all the central banks left policy on hold, as was expected with all showing a more hawkish lean given the dramatic rise in energy prices, so far, and fears that food will follow shortly. The BOE was the most obvious as rather than a 5/4 vote with 4 votes for a cut, it was 9/0 for no movement. Adding the Thursday decisions to the previous ones from the week, and looking at the Fed funds futures market, the two tables below from cmegroup.com show the change over the past month from modest expectations of a cut at the next meeting to modest expectations of a hike, first:

Then, if we look at the aggregated probabilities, you can see that the market has priced out any cuts for 2026 at this stage, with nothing, really, until the end of 2027.

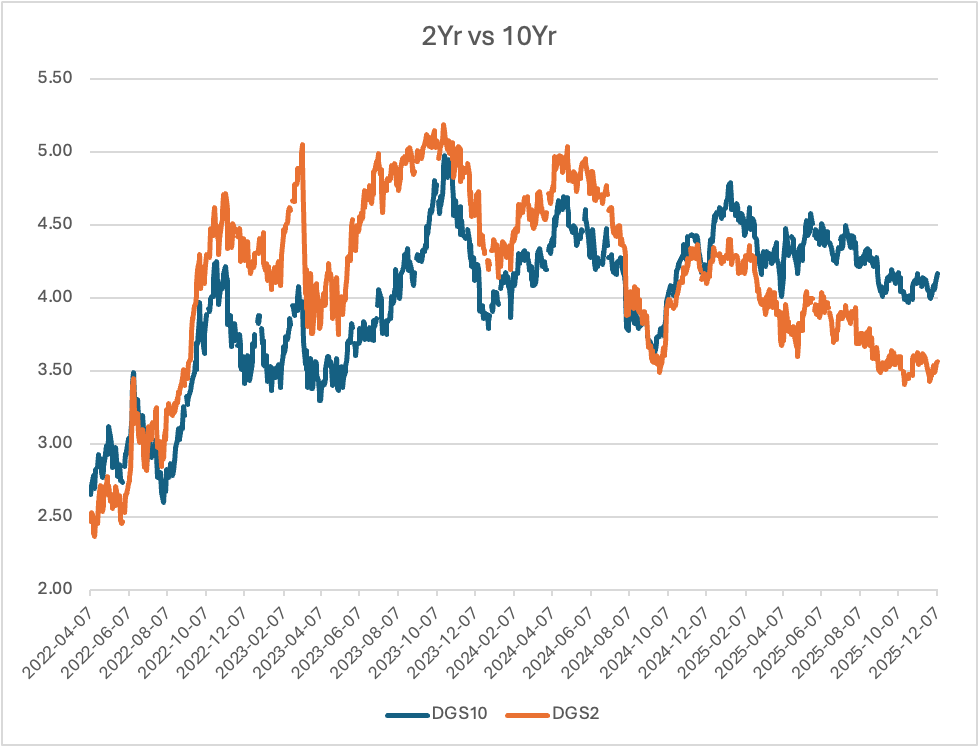

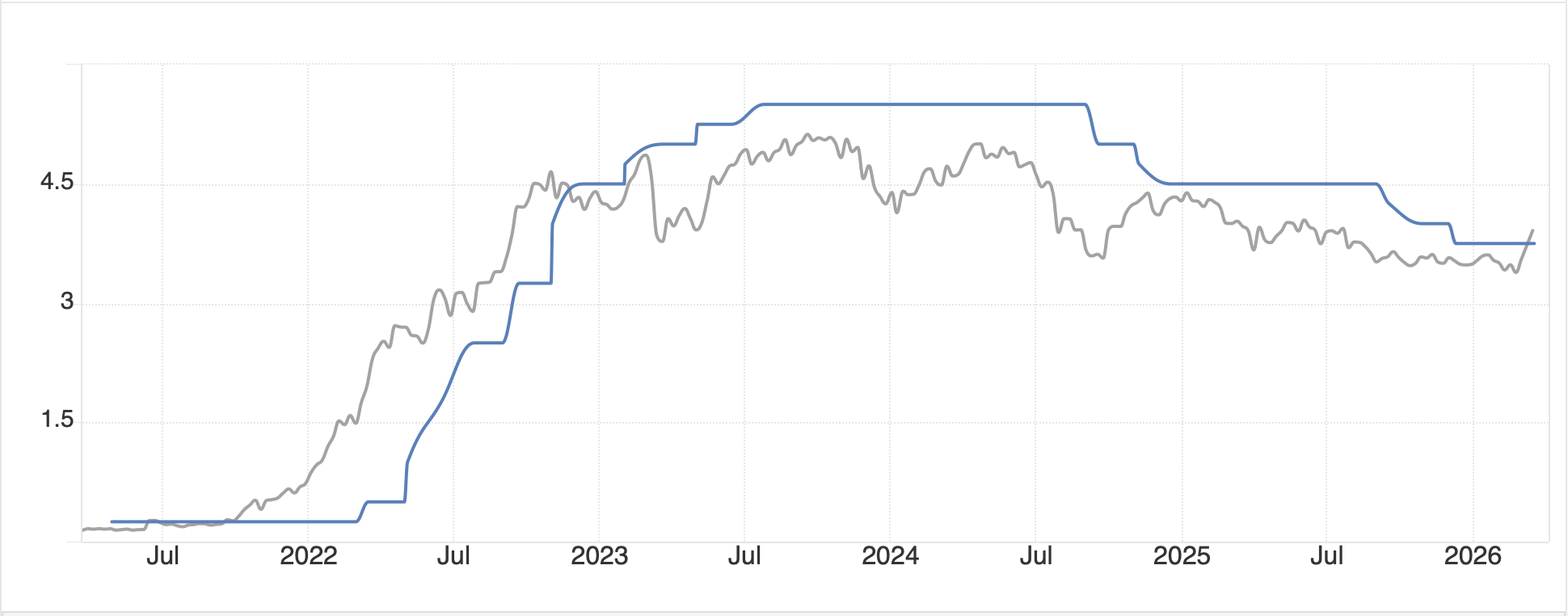

Now, here’s the thing about this pricing. It is a current estimation based on the Fed funds futures curve and certainly is subject to massive change going forward. However, other markets that rely on interest rate cues see this and respond accordingly.

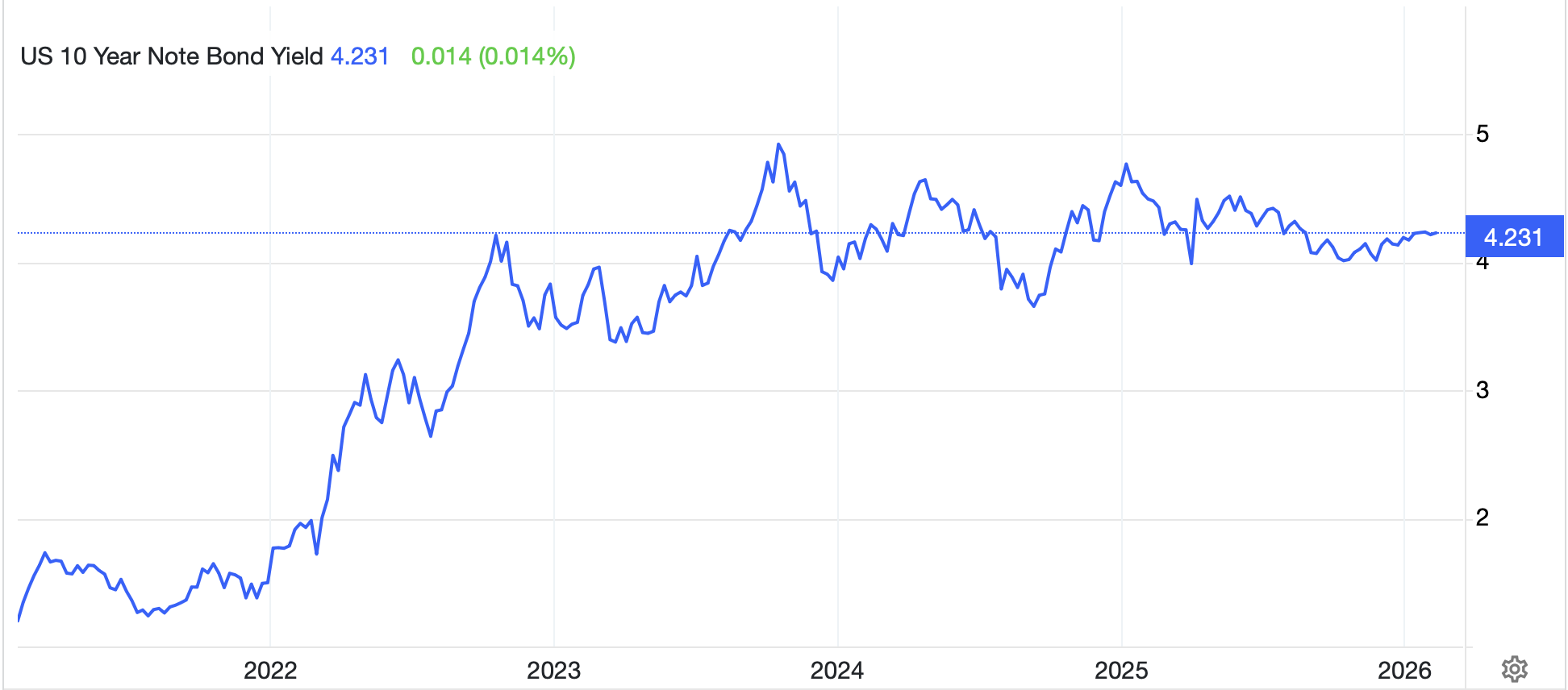

For instance, the 2-yr Treasury note (gray line) also has seen a major yield rally as you can see in the chart below and now sits above Fed funds effective (blue line) for the first time since late 2022 when the Fed finally caught up in its race against the raging inflation of the time.

Source: tradingeconomics.com

So, inflation is once again a major worry of the markets, and investors have come to believe that central banks are not going to be coming to the rescue for their risk assets as their hands will be tied by higher energy prices driving headline inflation higher. Of course, we all know that central banks raising rates will not adjust short term price inelasticity for energy products, although it could well cause a deep recession which would likely have an inflation impact. But my take is, that is not their goal either.

And that is why everyone is so unsettled. The idea that the central banks are going to come to the rescue of risk assets has been killed and now the pricing of those assets needs to rely on their own fundamentals, a much tougher task historically.

This is especially so given the data from Thursday showed PPI much hotter than expected, which adds to the narrative that the Fed, and other central banks, are on hold, at best, if not getting itchy to hike rates.

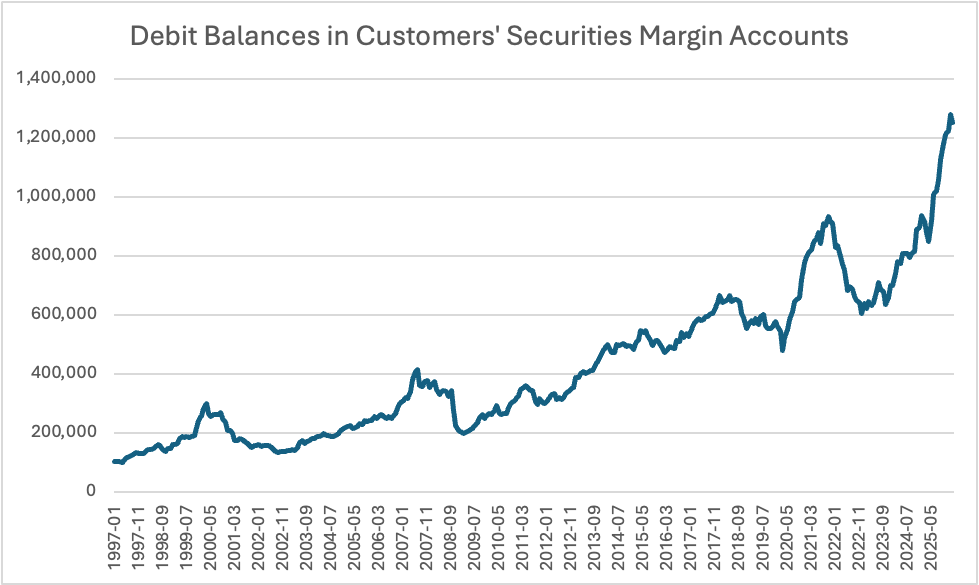

With this in mind, we cannot be surprised that equity markets suffered greatly on Friday, as did bond markets and precious metals. However, I believe the drivers of equities are different than those of the traditional havens of bonds and gold. In the case of equities, high valuations, which have existed for a long time, and significant leverage, with margin debt at record highs, although as you can see from the chart below, I created from FINRA data, it turned down ever so slightly in February have started to take their toll.

And in fact, that toll on margin debt is being played out in both bonds and gold as both are clearly feeling the effects of massive deleveraging as hedge funds and CTAs all scramble to make their margin calls. In this case, they sell what they can that is liquid, not what they want to sell, so bonds and gold fit the bill. My take is if the war continues very much longer, we will see the margin selling diminish and soon, both gold and bonds are going to seem like pretty good places to hide. (Now, if you want to keep up with inflation, USDi, the fully-backed inflation tracking crypto currency available at www.usdicoin.com) is going to do so far better than short-term interest rates which are almost certainly going to lag inflation for a while going forward! Ask me about this and I am happy to discuss.)

And that’s all I have this evening. There is a great deal of back and forth with threats from both sides in the war, and whether or not the Iranian electricity infrastructure is hit, or if their nuclear power plant at Bushwehr is hit and if so, how they retaliate remains unknown and fodder for the narrative writers. I have no opinion other than I hope none of that happens.

In the meantime, risk reduction is likely to continue as equities suffer while the dollar maintains its value and oil is the real risk, as any indication that the military action is ending is likely to see a major downdraft there. Unless you are a professional trader, with real capital behind you and a great market and news feed, this is not a time to play in my view. However, if I look at things and where they currently sit as Sunday night opens, gold seems to be too cheap. For millennia it has served as the last recourse of safety, and I do not believe this war will be any different than any of the countless wars in the past. This doesn’t mean it cannot go lower, just that it probably is approaching a place of ‘value’ especially as you can be sure that at some point later this year, every central bank will be printing as fast as they can if economies start to stutter. One poet’s thought.

Let’s see what happens overnight and I will be back again tomorrow.

Good luck

Adf